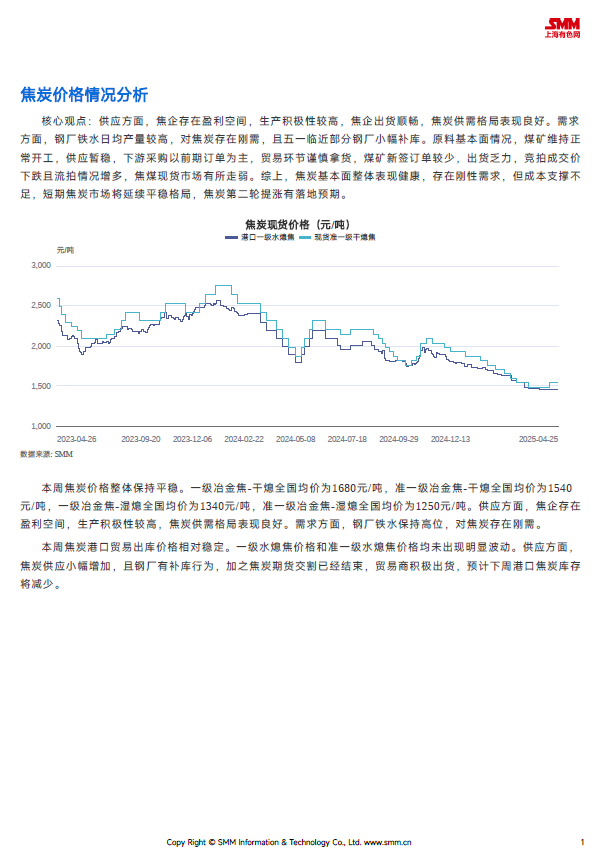

[SMM Coke Market Weekly Report 20250530] Bearish sentiment in the market remains strong; a third round of coke price cuts is expected next week

In terms of supply, the profit and loss situation of most coking enterprises remains within an acceptable range, with production temporarily stable and coke supply fluctuating at highs. In terms of demand, there has been a seasonal decline in steel demand, with pig iron continuing its downward trend. Moreover, as south China enters the rainy season, high temperatures and rainy weather are affecting project commencements, further dampening the enthusiasm of steel mills to purchase coke. Regarding the fundamentals of raw materials, coal mines are maintaining a normal production pace, with supply remaining loose. The wait-and-see sentiment among downstream players remains heavy, and online auction transactions are poor. Coal mines have lowered their starting auction prices, but the signing situation remains unfavorable. In summary, bearish sentiment in the market remains strong, and the coke market is expected to be in the doldrums in the short term, with a third round of price cuts expected next week.

》Subscribe to view historical prices of SMM metal spot cargo

![Short-Term Finished Steel Continues to Move Sideways, Raw Material Trends May Diverge [SMM Steel Industry Chain Weekly]](https://imgqn.smm.cn/usercenter/zDUFJ20251217171748.jpg)

![[SMM Steel Monthly Shipping] In May, departures from 32 Chinese ports edged down 3.43% MoM.](https://imgqn.smm.cn/usercenter/MhPNV20251217171716.jpg)