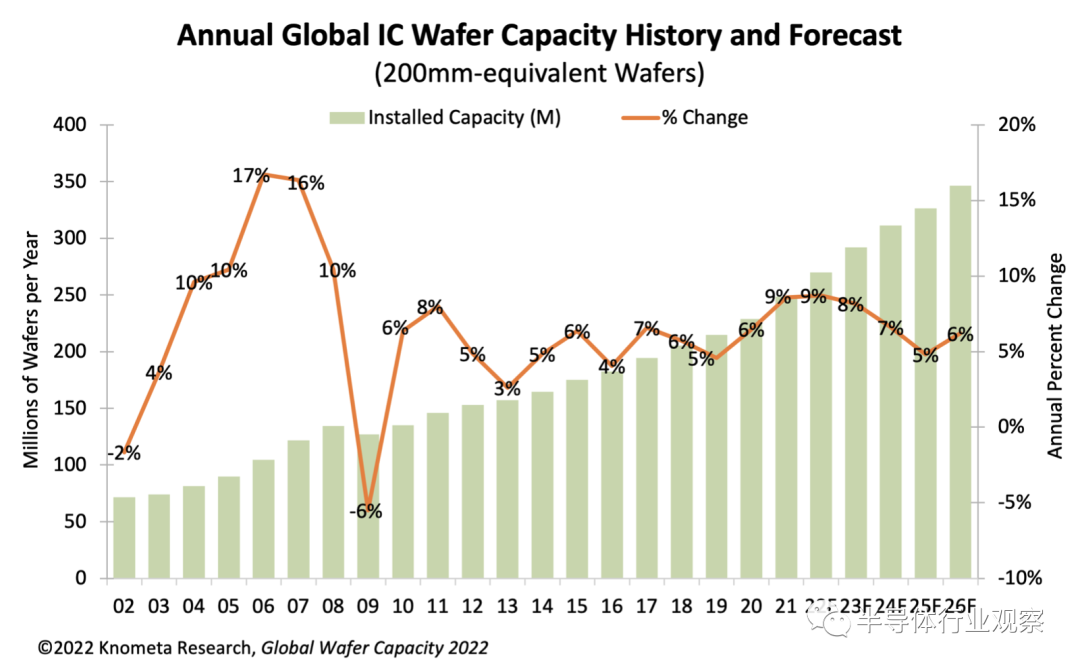

IC manufacturers responded to widespread shortages by adding 8.6 per cent of capacity in 2021, the highest level since 8.0 per cent in 2011 or 10.4 per cent in 2008, according to analyst firm Knometa Research.

Capacity is expected to grow by 8.7 per cent by 2022 and then by 8.2 per cent in 2023.

In 2021, capital expenditure on wafer factories and equipment accounted for 25 per cent of semiconductor revenue, the highest level since the ratio was 26 per cent in 2001. In the past, very high expenditure-to-sales ratios usually indicated that capacity had increased too much and that market adjustment was just around the corner.

In 2001, capacity utilization fell sharply from the collapse in chip demand in 2000. However, compared with 2001, unit shipments in 2021 were very strong, resulting in an overall utilization rate of nearly 94%.

The ratio of capital expenditure to sales is expected to remain high in 2022 as chipmakers continue to increase wafer production to address persistent shortages. Due to the depth and duration of the shortage, global interest in building fabs has been restored.

Over the past decade, governments in countries that no longer emphasize chip manufacturing have renewed their interest in providing incentives for companies to set up wafer factories in their own countries.

Of course, the current upsurge in fab construction activity and the emergence of new fab construction plans have raised concerns that too much capacity will be added in the coming years, which could lead to downward pressure on prices that supply exceeds demand.

However, Knometa Research partner IC Insights predicts that IC unit demand will grow well in 2022 and 2023, followed by low but still positive growth in 2024.

IC Insights predicts that the average selling price of IC will fall by 5% in 2024, and the decline in ASP is a sign that supply exceeds demand. However, unit shipments are still expected to grow by 4 per cent that year, causing the market to contract by only 2 per cent. In addition, IC Insights expects growth to resume in 2025 and 2026.

Given the continued healthy demand for integrated circuits and the fact that manufacturers are still struggling to address huge shortages, the industry's current capacity expansion plans do not seem excessive.

Semiconductor capital expenditure hit an all-time high in IC insights:2021

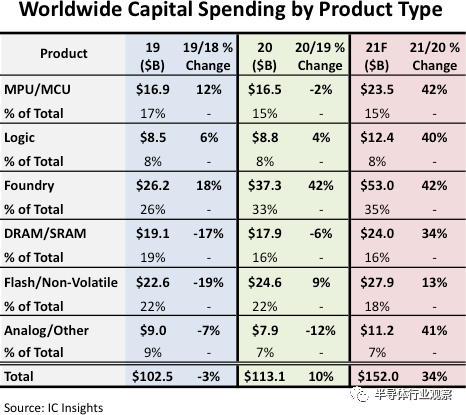

Global semiconductor capital spending is expected to soar 34 per cent in 2021, the biggest percentage increase since 41 per cent growth in 2017, according to IC Insights. Spending this year, at $152 billion, will hit a record annual high, surpassing the record of $113.1 billion set last year. Figure 1 shows semiconductor capital expenditure by major product segment from 2019 to 2021.

As shown in the chart, the contract manufacturing sector is expected to account for 35% of all semiconductor capital expenditure by 2021, which could easily become the largest portion of capital expenditure in major product / sector categories. Foundry has accounted for the largest share of semiconductor capital expenditure every year since 2014, with two exceptions-capital spending on DRAM and flash memory surged in 2017 and 2018. As the industry's demand for IC made using advanced process technology nodes continues to rise, the cost of foundry becomes very important (and necessary).

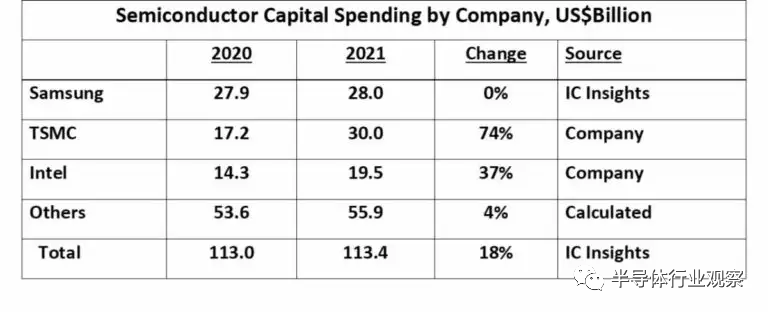

TSM.US, the world's largest contract manufacturer, is expected to account for 57 per cent of the $53 billion spent on contract manufacturing this year. Samsung has also invested heavily in its contract manufacturing business. Samsung has been able to match TSMC's technology roadmap and continues to strive to attract more leading wafer-free logic suppliers away from its pure foundry competitors.

On the other hand, the Chinese government is counting on SMIC to supply more semiconductors to the Chinese market. But SMIC's ability to implement these plans has been seriously undermined by SMIC's (00981) blacklist in the United States. SMIC's capital expenditure is expected to fall 25 per cent to $4.3 billion this year, accounting for just 8 per cent of total contract manufacturing spending in 2021.

By 2021, capital expenditure in all product sectors is expected to show strong double-digit growth, with OEM and MPU/MCU having the largest year-on-year growth of 42 per cent, followed by analog / other (41 per cent) and logic (40 per cent).

Contrary view: beware of overcapacity

Semiconductor manufacturers are expanding capital spending in 2021 and beyond to help ease shortages. In addition, many governments around the world are proposing to finance their home-grown semiconductor manufacturing.

The U.S. Senate approved a bill this month, including $52 billion to fund research, design and manufacturing of semiconductors. The bill is supported by the U.S. House of Representatives and President Joe Biden.

Japan's Ministry of economy, Trade and Industry announced a "national project" earlier this month to support Japan's semiconductor manufacturing.

South Korea announced a plan in May to spend $450 billion on non-memory semiconductor manufacturing over the next decade, to be paid for by private companies and government tax credits.

The European Union announced in May that it was prepared to invest "a lot" of money to expand semiconductor manufacturing in Europe.

These government measures will help support investment by semiconductor manufacturers. SEMI's latest fab forecast predicts that the industry will build 19 and 10 mass semiconductor fabs in 2021 and 2022, respectively. These fabs should spend more than $140 billion on equipment. China and Taiwan will each have eight new fabs, including six in the Americas, three in Europe and the Middle East, and two in Japan and South Korea.

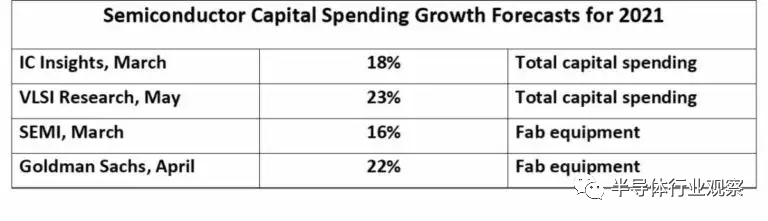

According to IC Insights, the total (CapEx) of capital expenditure in the semiconductor industry was $113 billion in 2020. The forecast for growth in 2021 is between 16% and 23%.

Three companies accounted for more than 50% of semiconductor capital expenditure in 2020. Samsung, the biggest spender in 2020, is expected to spend $27.9 billion and is expected to be flat in 2021. TSMC has seen the biggest increase, rising by $12.8 billion from 2020 to $30 billion, with a growth rate of 74 per cent in 2021. TSMC will account for more than 60 per cent of the industry's total expenditure growth of $20.4 billion. INTC.US has said it will increase its spending from $14.3 billion in 2020 to $19.5 billion in 2021, an increase of 37 per cent. The 2021 forecast is mainly made in April after the release of first-quarter earnings. Many of these figures are likely to be revised upwards during 2021.

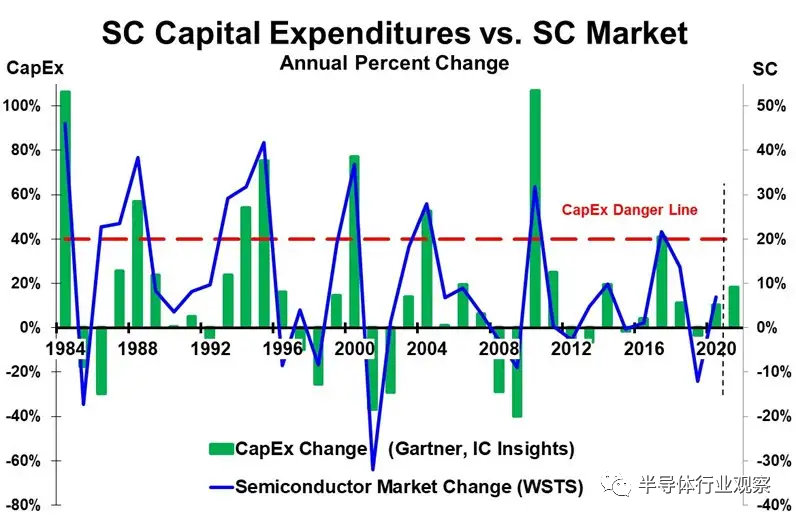

The semiconductor industry has traditionally experienced boom-bust cycles. A large amount of investment was made to expand production capacity in a period of high demand. When demand growth slows or falls, overcapacity leads to lower incomes. This trend is shown in the following figure. The annual change in semiconductor capital expenditure is indicated by a green bar chart on the left-axis scale. The annual change in the semiconductor market is shown by the blue line on the right-axis scale. The red line marked "capital expenditure danger line" indicates that more than 40% growth in capital expenditure will cause the semiconductor market to get into trouble.

After a sharp increase in semiconductor capital expenditure, the semiconductor market will decline (or a significant slowdown in growth) within a year or two. When the semiconductor market grew by 46% in 1984, capital expenditure increased by 106%. This was followed by a 17% decline in the semiconductor market in 1985. In 1988, the semiconductor market grew by 38%, and capital expenditure increased by 57%. Since then, the semiconductor market slowed by 30% to 8% in 1989. The next big growth period was from 1993 to 1995, when it peaked in 1995, with market growth of 42 per cent and capital expenditure growth of 75 per cent. The following year, the market fell 9%. The 8% decline in the market in 1998 was due to the Asian financial crisis.

In 2000, at the peak of the Internet boom, the semiconductor market grew by 37%. At the same time, capital expenditure increased by 77 per cent. In 2001, the market suffered its biggest decline in history, at 32%. In 2004, the market grew by 28%, and capital expenditure grew by 52%. In 2005, it grew by 21 percentage points to 7%. The decline in the semiconductor market in 2008 and 2009 was caused by the global financial crisis. Strong growth resumed in 2010, with the market growing by 32 per cent and capital expenditure by 107 per cent. The market slowed by more than 30 percent in 2011, almost zero growth, and then fell by 3% in 2012. In 2017, the market grew by 22% and capital expenditure by 41%. Compared with the previous peak growth rate, growth in 2017 was relatively modest. Two years later, however, the market fell by 12 per cent in 2019.

There are many factors affecting the growth rate of the semiconductor market, including the overall economy and the demand for key electronic products. However, when demand slows, a sharp increase in capacity always leads to overcapacity. Overcapacity has led to lower prices for semiconductors, especially for commodities such as memory. Inventories held by electronics manufacturers and distributors have been cut. This overcapacity tends to occur after capital spending increases by more than 40 per cent. This is indicated by the red capital expenditure danger line in the chart.

Capital expenditure is expected to grow between 16 per cent and 23 per cent in 2021, and the industry is far from close to the "danger line" of more than 40 per cent growth. Even if capital expenditure growth accelerates in the second half of 2021, it is unlikely to exceed 30 per cent. TMSC is satisfied with the 74 per cent increase in capital expenditure because many of its contract manufacturing customers have asked for more capacity. Two other contract manufacturers, UMC and GlobalFoundries, both plan to at least double capital expenditure in 2021 compared with 2020. SMIC, a Chinese contract manufacturer, plans to cut capital spending by 25% in 2021, mainly because of trade problems. After the memory market fell 33 per cent in 2019 two years ago, memory companies such as Samsung were cautious about capital spending.

Although the current situation does not indicate semiconductor overcapacity in the near future, it is worth paying attention to in the coming years. It remains to be seen to what extent the current shortage of semiconductors is due to short-term disruptions caused by a pandemic and to increased demand for electronic equipment and increased content of semiconductors.