Indonesia has officially activated one of the most structurally significant commodity trade reforms in its recent history. On May 20, 2026, President Prabowo Subianto signed Government Regulation (PP) No.24/2026 on the Governance of Strategic Natural Resource Commodity Exports (State Gazette No.58, Supplementary State Gazette No.7178), which took effect on June 1, 2026 per Article 10. The regulation designates Danantara Sumberdaya Indonesia (DSI) as the mandatory sole export intermediary for all shipments of coal, palm oil, and ferro alloys. No Indonesian producer in these categories can sell directly to a foreign buyer anymore. Every transaction must legally pass through DSI first.

The constitutional grounding is explicit. The preamble invokes Article 33 of the 1945 Constitution, which establishes that natural resources are controlled by the state and must be used for the greatest possible benefit of the Indonesian people (sebesar-besar kemakmuran rakyat). The regulation's explanatory notes go further, stating that "so long as the state possesses the capital, technology, and management capability to manage Strategic SDA Commodities, the state should undertake direct management," and that doing so ensures "all results and profits will become state revenue bringing more optimal benefits for the welfare and prosperity of the people." This is framed not as a technical trade regulation but as a matter of constitutional duty.

The explanatory notes to Article 7 explicitly name the five digital systems through which DSI will exercise oversight: CEISA (Customs Excise Information System and Automation), SINSW (Indonesia National Single Window), INATRADE (Trade Information System), SiMoDIS (Integrated Foreign Exchange Monitoring System), and MOMS (Minerba Online Monitoring System). Real-time visibility across all five platforms forms the enforcement backbone of the entire reform.

On June 9, Minister of Energy and Mineral Resources Bahlil Lahadalia and DSI COO Dony Oskaria offered three key reassurances at a press conference to calm investor sentiment. Oskaria confirmed that existing B2B contracts and Letters of Credit will continue to be honored during the transition period, provided DSI's monitoring system confirms that pricing is fair and transparent. Bahlil categorically denied market rumors of a "profit-sharing" mechanism in the minerals sector, stating that this concept applies only to oil and gas and that Minerba rules remain unchanged. He also committed to aligning RKAB mining quotas with smelting capacity and promised quota relaxations during periods of highly favorable global prices.

June 8th DPR RI Coordination Hearing: What Bahlil and Dony Oskaria Actually Said

The Indonesian House of Representatives (Dewan Perwakilan Rakyat Republik Indonesia / DPR RI) convened a coordination hearing to align the new natural resource export governance policy between Danantara's Investment Management Agency (BPI Danantara) and the Ministry of Energy and Mineral Resources (Kementerian ESDM). The session featured Minister Bahlil Lahadalia representing ESDM and DSI COO Dony Oskaria representing BPI Danantara.

Oskaria opened by clarifying the precise scope of DSI's mandate in its initial phase. He confirmed that DSI's primary and immediate purpose is to halt under-invoicing and transfer pricing — not to disrupt physical commodity flows. He gave explicit assurance that existing B2B sales contracts and Letters of Credit will continue to be honored and executed normally during the transition period, with one condition: DSI's digital monitoring system must determine that the declared pricing is fair and reflects genuine market values. Any contract where declared prices are flagged as suspiciously below market will be subject to DSI scrutiny, but standard commercially negotiated contracts should proceed without interruption.

Bahlil addressed three distinct concerns that had been circulating in the market. First and most urgently, he categorically denied rumors of a "gross split" profit-sharing mechanism being introduced into the minerals sector. He stated directly that gross split calculations exist only in the oil and gas sector and that there are "absolutely no changes" to the existing rules governing the minerals and coal (Minerba) space. This denial was significant because the rumor alone had been enough to cause investors to reconsider capital commitments to Indonesian smelting projects. Second, Bahlil acknowledged the domestic ore supply squeeze that has been tightening around Indonesian smelters, and committed to aligning RKAB mining quotas with downstream smelter capacity. He promised "measured relaxations" of production limits during periods when global commodity prices are highly favorable, signaling that the government has no interest in strangling the smelting industry it has spent years building. Third, on the broader question of investment security, Bahlil framed DSI as a value-capture mechanism rather than a market interference tool — the government wants more of the revenue that Indonesian commodities generate to stay in Indonesia, not to reduce the volume of those commodities being exported.

What the Regulation Actually Says: Key Articles

Reading PP No.24/2026 directly, several provisions carry commercial implications beyond what the market has fully absorbed.

Article 3(1) establishes the core mandate: strategic commodities may only be exported by the BUMN Ekspor, acting either as owner or as sole intermediary. The word hanya ("only") in the Indonesian text is unconditional. Article 3(2) goes further: the selling price of Strategic SDA Commodities is determined by the BUMN Ekspor. This is not a transparency or monitoring function — DSI holds formal pricing authority over every export transaction. Article 3(4) confirms that DSI may charge a margin at a reasonable level in accordance with prevailing regulations, meaning DSI is legally entitled to a fee for its intermediary role. The combination of state-determined selling price and a state-imposed margin on every nickel and ferro alloy export has not yet been fully digested by the market.

Article 4(2) contains the most important exemption in the regulation. DSI's mandatory intermediary role can be waived for business operators who hold contracts or agreements with the government that include provisions on at minimum: investment, divestment, and domestic processing and/or refining. Exemptions are decided in a coordination meeting chaired by the Coordinating Minister for Economic Affairs. For the nickel sector, this is a critical provision — any smelter with an existing government contract containing these three elements has a legal pathway to apply for exemption from DSI routing entirely.

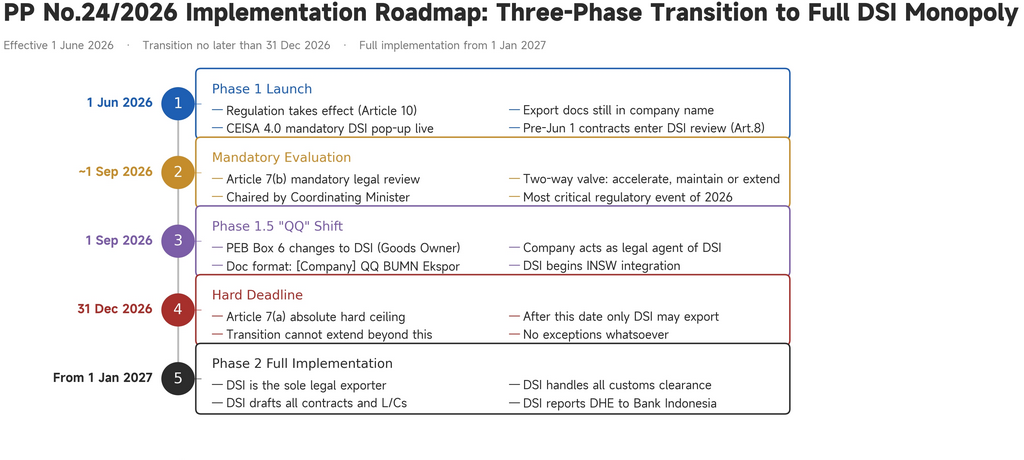

Article 7 governs the full transition timeline. It states that from June 1 through no later than December 31, 2026, exports must go through BUMN Ekspor. Within three months of the effective date — meaning by approximately September 1, 2026 — a formal inter-ministerial evaluation must take place. Based on that evaluation, the Coordinating Minister has the authority to set a new deadline that is either earlier or later than originally planned, provided it remains before December 31. This is a genuine two-way valve: if the transition is going well, implementation can be accelerated; if problems emerge, the government can extend the timeline. Article 7(e) further provides that if the transition completes ahead of any applicable deadline, the full DSI-only rules apply from that earlier date immediately.

Article 8 addresses existing contracts: all sales contracts signed before June 1, 2026 that remain valid are subject to evaluation by the BUMN Ekspor. DSI holds formal authority to assess every pre-existing long-term purchase agreement, including those between Indonesian smelters and their Chinese offtake partners.

Critical Dates and Deadlines: The Full Regulatory Calendar

May 20, 2026 — PP No.24/2026 signed by President Prabowo Subianto.

June 1, 2026 — Regulation takes effect. Phase 1 begins. CEISA 4.0 mandatory DSI reporting pop-up activated. Pre-June 1 sales contracts enter DSI evaluation period under Article 8.

By ~September 1, 2026 — Mandatory inter-ministerial evaluation of the transition (Article 7b). This review is a legal obligation, not optional. Its outcome determines the pace of everything that follows: the Coordinating Minister may accelerate, maintain, or extend the timeline to any date before December 31.

September 1, 2026 — Phase 1.5 begins (unless the evaluation resets the timeline). PEB Box 6 changes to BUMN Ekspor (DSI). QQ document format begins. Companies act as DSI's legal agents.

December 31, 2026 — The hard outer ceiling (Article 7a). After this date, no transitional exceptions remain. Only DSI may export, unconditionally. The Coordinating Minister cannot extend beyond this date.

January 1, 2027 (or earlier if accelerated) — Phase 2 full implementation. DSI is the sole legal exporter. DSI drafts all contracts and L/Cs, handles all customs clearance, and reports DHE directly to Bank Indonesia via SiMoDIS.

The NPI Classification Crisis

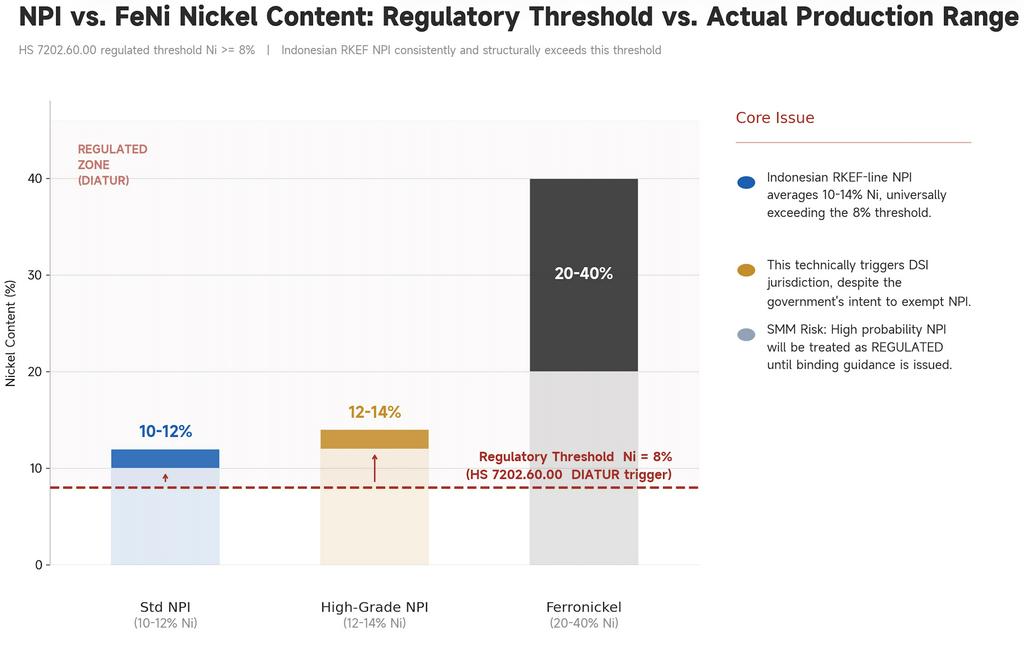

The inclusion of ferro alloys has created the most significant market confusion, centered on a single unresolved technical problem: where Nickel Pig Iron sits relative to the regulated ferro-nickel HS code.

Ferronickel (FeNi) is a mature, refined iron-nickel alloy produced through capital-intensive smelting, typically containing 20–40% nickel. It is a direct feedstock for stainless steel production and commands a meaningful price premium. Nickel Pig Iron (NPI) was developed in China in the mid-2000s as a low-cost alternative, produced via the simpler Rotary Kiln-Electric Furnace (RKEF) process using laterite ore. Indonesian RKEF-line NPI consistently produces at 10–14% Ni — a structural result of the process and the ore body, not a product specification smelters can adjust. NPI trades at a significant discount to FeNi, and any trader or stainless steel mill can distinguish the two products immediately.

The problem is that Indonesia's customs classification framework cannot reliably tell them apart. Both products can fall under HS 7202.60 (ferro-nickel), and Indonesian NPI smelters have historically declared under that code without issue. Under Permendag No.12/2026, HS 7202.60.00 is now DIATUR (Regulated) — triggered when Ni content reaches ≥ 8%. The Ministry of Trade chose this as the demarcation: refined FeNi at 20–40% Ni would clearly exceed it, while NPI was assumed to fall below it and escape the regulation.

That assumption fails entirely. Standard Indonesian RKEF output runs 10–12% Ni; higher-grade lines reach 12–14% Ni. There is no commercially significant NPI stream below 8% Ni under normal operating conditions. The threshold sits below average grade Indonesia actually produces, meaning every Indonesian NPI shipment technically triggers under the regulated classification, capturing precisely the product the government intended to exempt. Internal Rakortek documents confirm the Coordinating Minister directed that NPI should not be captured. The discussion slides acknowledge the collision and propose corrective steps: set a threshold above actual RKEF NPI norms, issue binding technical definitions for NPI, and align classification consistently across HS 7201 (pig iron), 7202.60 (ferro-nickel), and 7502.20 (nickel alloys). None of that supplemental guidance has been published yet.

Strategic Outlook: The September Evaluation Is the Pivot Point

The most important thing to understand about PP No.24/2026's near-term trajectory is that the regulation has deliberately built in a recalibration mechanism — and that mechanism has not been priced into most market participants' planning.

Article 7(b) and 7(c) together create a genuine two-way valve. The September evaluation is a legally mandated inter-ministerial review that gives the Coordinating Minister real authority to reset the timeline in either direction. If the first three months reveal that DSI is not operationally ready, and the Rakortek checklists, which showed nearly every DSI readiness item as incomplete as of May 25, suggest that risk is real — the Coordinating Minister can formally extend the transition and push the QQ phase and beyond to a later date before December 31. Equally, if the reporting data flowing through CEISA, SiMoDIS, and MOMS shows that compliance is working smoothly and DSI is ready, the same evaluation could authorize an accelerated Phase 2 arrival, potentially as early as October or November 2026.

What is not negotiable is the December 31, 2026 ceiling. Articles 7(a) and 7(d) together make clear that this is the absolute outer boundary of the Coordinating Minister's authority. Regardless of what the evaluation finds, the transition cannot be extended beyond December 31. After that date, DSI is the sole legal exporter with no exceptions, and no amount of industry pressure or operational unreadiness changes that.

The Article 4(2) exemption pathway remains the most immediately actionable provision for smelters with qualifying government contracts. Any agreement containing investment, divestment, and domestic processing provisions should be reviewed against that exemption criteria now. Engaging the Coordinating Minister's coordination meeting process before the September evaluation is concluded is far preferable to doing so afterward.

On NPI, the plain text of Permendag No.12/2026 as it stands today classifies Indonesian NPI as regulated. Smelters should not wait for the Ministry of Trade's supplemental guidance before beginning compliance preparation. Seeking an advance product classification ruling, exploring the Article 4(2) exemption if applicable, and building DSI integration workflows in parallel remains the most prudent path. The December 31 deadline, or whatever earlier date the post-evaluation acceleration may set, is not the end of the story. It is the point at which the entire B2B architecture of Indonesian strategic commodity exports permanently and irreversibly changes.

SMM Analysis makes no representations as to the official legal interpretation of any regulation cited. Stakeholders should seek formal legal counsel for all compliance decisions.

![[NPI Daily Review] Consecutive Declines in Futures Drag Down Spot Cargo, NPI Price Center Continues to Move Down](https://imgqn.smm.cn/usercenter/WNjzM20251217171732.jpeg)