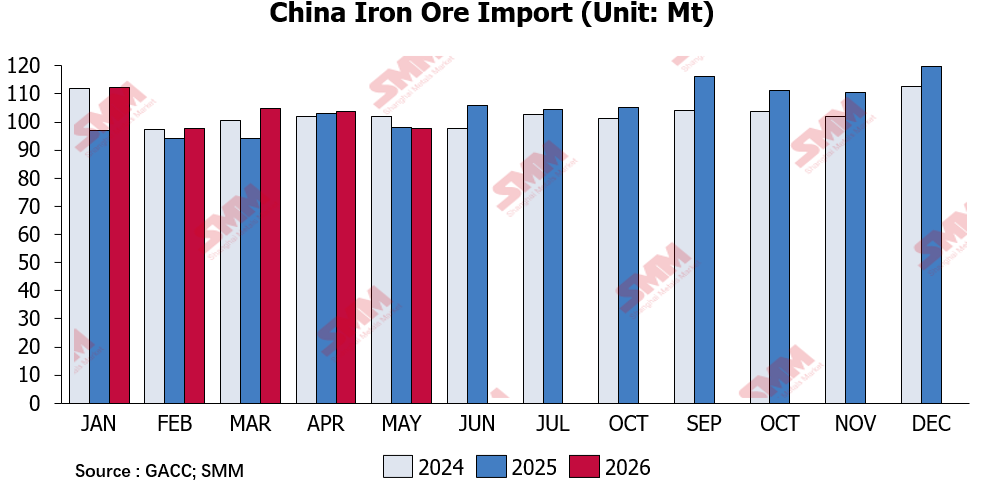

According to the latest data from the GACC. China has imported 97.711 Mt of iron ore and concentrates in May, down 6.143 Mt MoM, a decline of 5.9%. Cumulative imports in January-May reached 516.258 Mt, increased 6.3% YoY.

In May, the operating rate of China's steel industry remained high, with strong downstream demand supporting high pig iron production at steel mills. Given wider profit margins, mills' appetite for iron ore remained solid. That said, elevated port inventories and a persistent decline in ore prices in late May squeezed import margins and partly curbed buying interest. In addition, iron ore prices in May were affected by adjustments to the statistical cycle and the Labour Day holiday, resulting in fewer statistical days compared with April. Some enterprises also made customs declarations ahead of schedule, leading to a notable MoM decline in iron ore imports in May.

June iron ore imports are expected to grow. On one hand, June, as the final month of Q2, will prompt some mines to accelerate production and shipping paces to meet shipment targets. On the other, although the market is starting to enter the traditional off-season for steel, ex-China steel demand is still able to drive Chinese steel exports, leaving mills sufficient surplus to maintain blast furnace operating rates. Hot metal output in June is also projected to stay elevated, providing rigid demand support for iron ore. Supply-demand synergy is expected to lift iron ore imports in June.

![[SMM Lecong HRC Inventory] Lecong HRC inventory continued to accumulate this week.](https://imgqn.smm.cn/usercenter/LMnqz20251217171717.jpg)