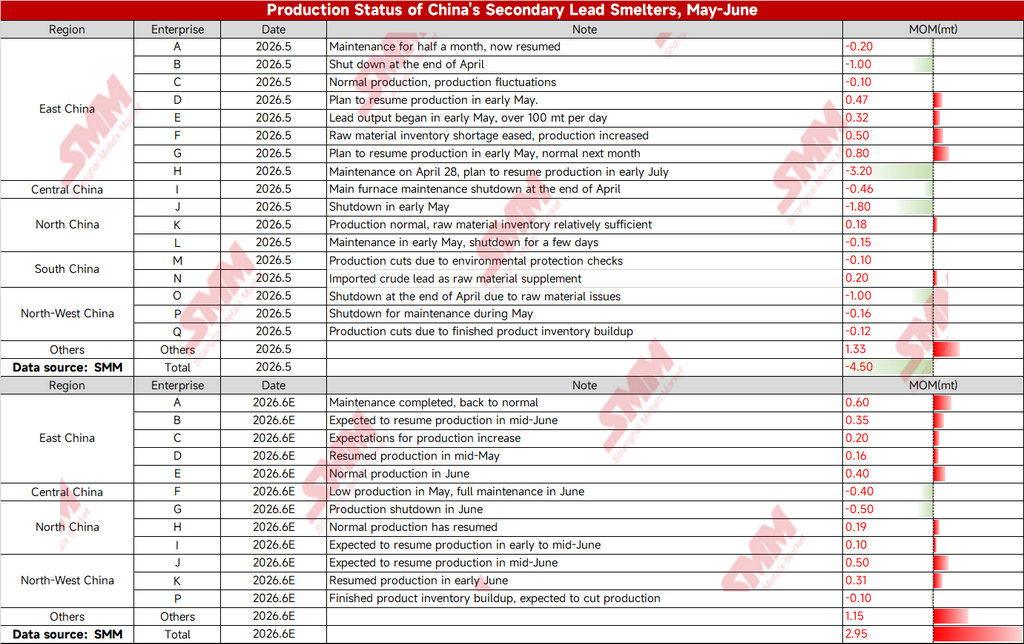

Os dados da SMM mostram que, em maio, o impacto mensal no chumbo refinado proveniente das empresas de chumbo secundário na China totalizou -45.000 toneladas métricas, com a contração da oferta se ampliando ainda mais. As fundições do leste, centro e norte da China, afetadas por paradas de produção, manutenção, escassez de matérias-primas e inspeções de proteção ambiental, tiveram os cortes de produção se espalhando.

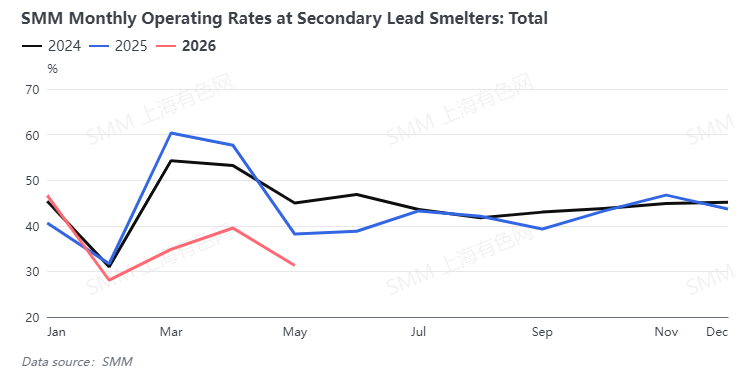

A taxa de operação das empresas caiu significativamente na comparação anual, atingindo um nível baixo observado nos últimos anos.

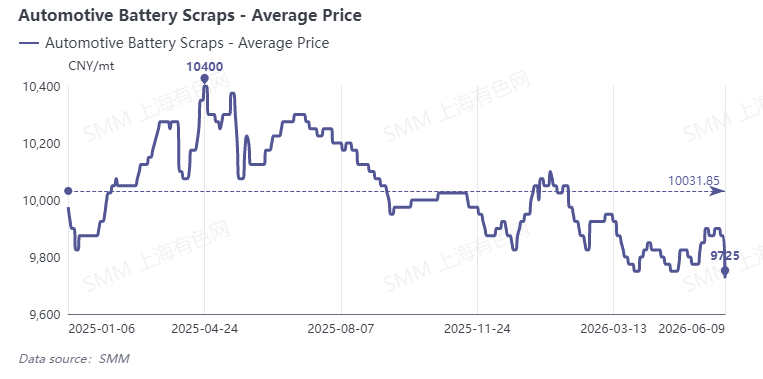

Do lado das matérias-primas, embora o preço médio da sucata de baterias de veículos elétricos tenha recuado das máximas, permaneceu em um nível relativamente elevado de 9.725 yuans/tonelada métrica.

Os custos elevados de aquisição continuaram a comprimir as margens das fundições e, juntamente com o acúmulo de estoques de produtos acabados em algumas empresas, a disposição para cortes passivos de produção se fortaleceu ainda mais.

Embora os cronogramas de produção de junho indiquem que a oferta deve se recuperar na variação mensal, com o impacto mensal total no chumbo refinado em +29.500 toneladas métricas e expectativas claras de retomadas e aumentos de produção entre as fundições do leste e noroeste da China, o ritmo de recuperação permanece altamente dependente da chegada de matérias-primas. O padrão de oferta restrita no setor de reciclagem de baterias usadas persiste, limitando a elasticidade da oferta.

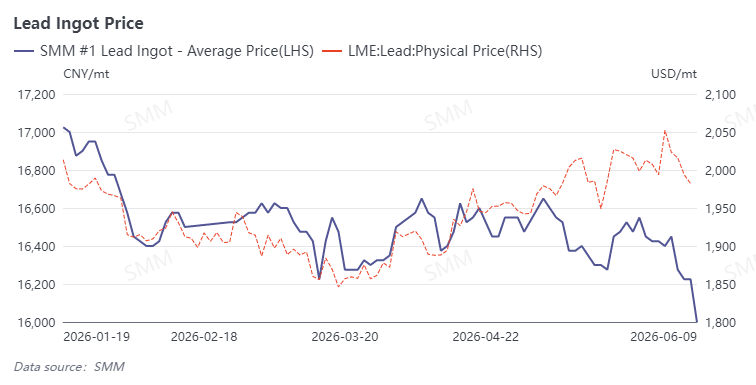

Do lado do consumo, o mercado a jusante de baterias de chumbo-ácido está na entressafra tradicional, com demanda final lenta. Os preços à vista do chumbo na China continuaram a flutuar em baixa, com o preço médio do lingote de chumbo #1 da SMM caindo abaixo de 16.200 yuans/tonelada métrica. Os preços do chumbo na LME também estavam em marasmo, com ambos os mercados doméstico e externo carecendo de claro momento de alta.

No geral, o mercado de chumbo secundário permanecerá em um padrão de "suporte de custo fraco e forte supressão do consumo" no curto prazo. As retomadas de produção das fundições em junho terão dificuldade em compensar integralmente os cortes anteriores, com o lado da oferta mostrando melhora marginal, mas permanecendo restrito. Os preços do chumbo continuarão a oscilar fracamente. No futuro, deve-se prestar muita atenção às melhorias na chegada de matérias-primas e à recuperação do consumo final, pois ambos determinarão conjuntamente o ritmo da recuperação da oferta de chumbo secundário e a trajetória dos preços do chumbo.

![Demanda do mercado de baterias de chumbo-ácido está fraca, algumas empresas do setor interrompem a produção para recesso de altas temperaturas [SMM – Comentário Semanal da Taxa de Operação de Baterias de Chumbo-Ácido]](https://imgqn.smm.cn/usercenter/guTSZ20251217171722.jpg)

![Fornecedores Ampliaram Descontos para Desovar Mercadorias no Fim do Mês, Transações no Mercado à Vista Lentas [Revisão Semanal do Mercado à Vista de Chumbo Refinado SMM]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)

![Taxa Semanal de Operação das Fundições de Chumbo Primário SMM (17 de julho a 23 de julho de 2026) [Revisão Semanal de Fundição de Chumbo Primário SMM]](https://imgqn.smm.cn/usercenter/mfCMp20251217171721.jpeg)