According to the latest SMM data, the secondary lead industry faced worsening difficulties of high costs and losses, with the price spread between raw materials and finished products continuing to narrow, enterprise losses widening, and operating rates declining accordingly.

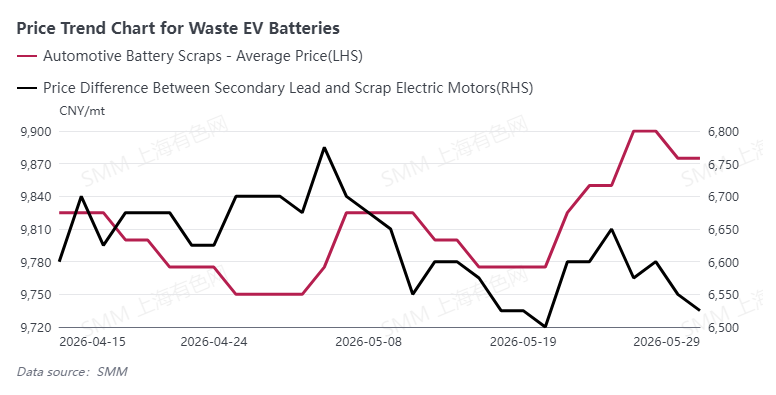

Cost side, waste EV battery prices stayed high, with the recent average price fluctuating at highs near 9,870 yuan/mt, pushing up secondary lead smelting costs. The price spread between secondary lead and waste battery raw materials continued to narrow, with the current spread having pulled back to approximately 6,500 yuan/mt, significantly narrower than the previous high, as raw material cost pressure continued to transmit to the smelting side, severely squeezing processing profit margins.

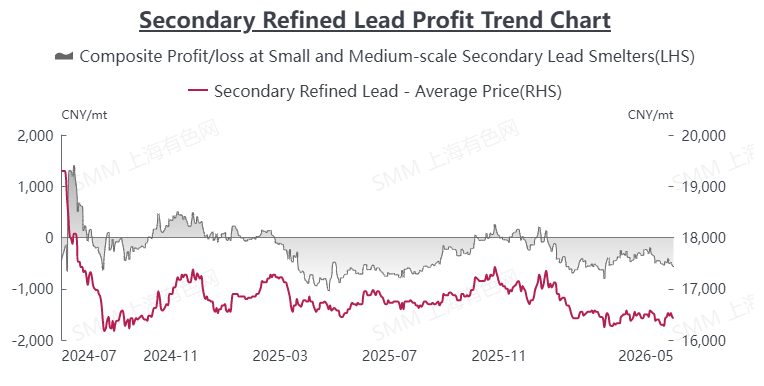

Affected by this, industry losses intensified: comprehensive losses of small and medium-sized secondary lead enterprises widened to approximately -550 yuan/mt, while large enterprises also generally fell into loss territory, with profitability deteriorating notably compared to the previous period. High costs combined with weak finished product prices left smelters struggling to recover profitability, with the industry as a whole clearly under pressure.

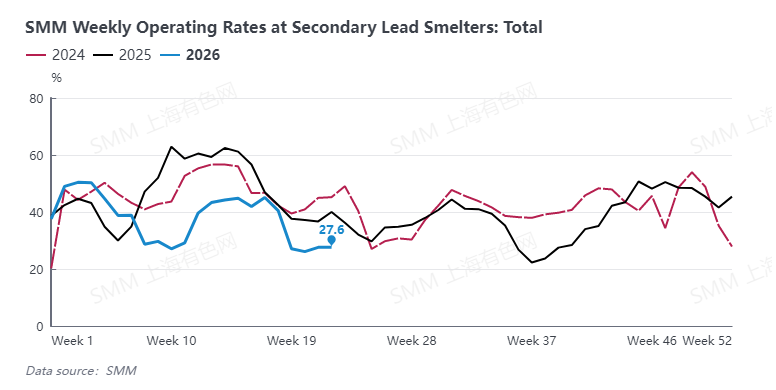

Under profitability pressure, enterprises' willingness to produce continued to weaken, and industry operating rates continued to decline. As of Week 23 of 2026, the national comprehensive operating rate of secondary lead dropped to 27.6%, at a low level for the year. Some small and medium-sized enterprises were forced to cut production or halt operations due to sustained losses, with a notable contraction on the market supply side.

Overall, the secondary lead industry is currently facing multiple pressures of high raw material costs, losses, and declining operating rates. In the short term, the tight raw material supply pattern is unlikely to change, cost support will stay high, and the industry as a whole may continue in the doldrums with losses and low operating rates.

![Bullish and Bearish Factors Coexisted in and outside China, SHFE Lead Replicated Previous Day's Trend [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/XMxKT20251217171720.jpeg)

![Supply Recovery VS Tight Raw Material, Lead Prices May Continue to Consolidate [SMM Lead Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)