In April 2026, domestic lead prices overall moved sideways, with spot cargo and futures trends remaining relatively stable. According to SMM data, the average spot price of SMM #1 lead ingot in April was 16,525 yuan/mt, with prices operating steadily within the range during the month, rising first then declining. Futures market, SHFE lead contract prices were generally higher than spot prices, the spread between futures and spot prices remained within a reasonable range, and overall market fluctuations were limited. Against the backdrop of stable price movements, China's lead product import and export markets showed significantly divergent trends — refined lead imports surged sharply while exports contracted significantly, lead alloy imports pulled back slightly, and the industry's supply-demand pattern underwent a phased reshaping.

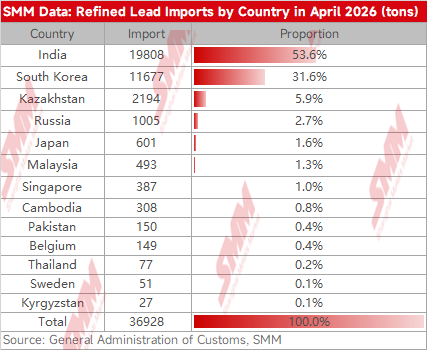

Import and export data showed that China's refined lead imports performed strongly in April, reaching a total of 36,928 mt, up 48.7% MoM from March, hitting a phased high.

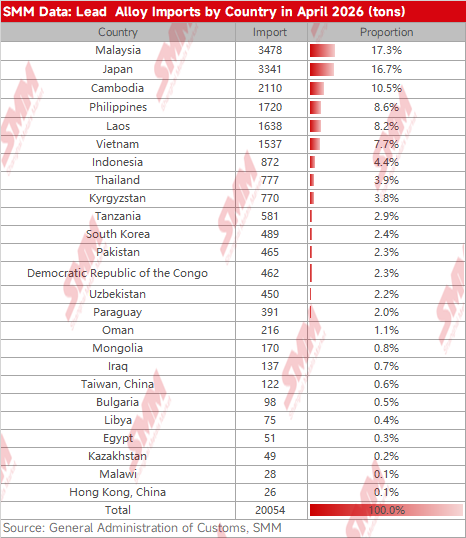

By country, April refined lead imports mainly came from India, South Korea, and Kazakhstan; lead alloy imports primarily originated from multiple Southeast Asian countries and Japan.

The sharp increase in imports was primarily driven by the persistently open import profit window. Lead ingot imports remained profitable throughout April, with average monthly import profit reaching 359.86 yuan/mt, greatly stimulating traders' enthusiasm for import arbitrage.

Meanwhile, large volumes of import orders signed during the period of widening domestic-to-overseas price spread in March arrived at ports in a concentrated manner in April, forming a lagged increment. Additionally, overseas LME lead inventory remained at elevated levels above 260,000 mt for an extended period, with ample ex-China supply providing solid support for increased refined lead imports into China.

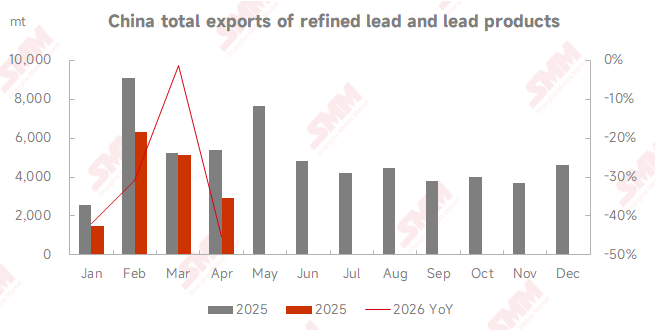

In contrast to the strong import trend, refined lead exports came under significant pressure in April, with monthly exports of only 927 mt, down 70.9% MoM. The core reason for weak exports was the severe inversion of export profitability, with the export window essentially closed and enterprises' willingness to export falling to low levels. Meanwhile, domestic lead market supply and demand remained relatively balanced, and combined with maintenance at some smelting facilities reducing domestic supply, domestic lead prices remained firm, with enterprises prioritizing domestic sales markets, further squeezing export space. In addition, lead alloy imports in April totaled 20,054 mt, pulling back slightly by 18.4% MoM, mainly because the downstream lead-acid battery market entered the traditional off-season, with end-users purchasing primarily based on rigid demand and alloy import demand contracting moderately.

Raw material side, lead concentrates imports remained stable, effectively ensuring domestic primary lead smelting production. Entering May, the fundamentals of China's lead market underwent a notable shift, with the market landscape gradually adjusting. Price side, prices pulled back slightly. As of May 25, the SMM #1 lead ingot average price edged down MoM from April, showing an overall trend of initial decline followed by fluctuations. Supply-demand side, bullish and bearish factors were intertwined. Supply side, primary lead operating rates remained stable, while secondary lead operating rates briefly pulled back at the beginning of the month, forming temporary supply support. However, demand side, weakness persisted, with the off-season effect for batteries becoming prominent, overall downstream operating rates remaining low, and market demand staying sluggish. Inventory side, continuous inventory buildup was observed, with social inventory across five domestic regions climbing significantly from the beginning of the month, exerting notable downward pressure on lead prices.

Import-export dynamics underwent a fundamental reversal in May. The import profit landscape completely reversed, with the monthly average import profit margin turning negative to -216.2 yuan/mt, and losses continued to widen. Import arbitrage opportunities completely disappeared, and newly signed import orders decreased sharply. Meanwhile, concentrated arrivals in April front-loaded earlier import demand. Combined with tight supply of high-grade lead ingots from Southeast Asia and elevated domestic inventory, multiple factors jointly suppressed import increments. Overall, refined lead imports in May are expected to pull back 30%-50% MoM, falling to the range of 15,000-25,000 mt. Lead alloy imports, underpinned by long-term contract commitments, are expected to see relatively limited fluctuations and maintain a slight pullback trend. Export side, weakness persisted, with the export loss pattern unchanged, and exports will continue to remain at low levels.

In summary, the April lead market was dominated by import arbitrage logic, with refined lead imports surging significantly and driving incremental domestic supply. Entering May, with the import window closing, end-use demand remaining in the off-season, and social inventory continuing to accumulate, the market's dominant logic shifted from external import increments to a domestic tug-of-war between sellers and buyers. Lead prices overall will continue a fluctuating trend, and the import-export market will also return to a relatively weak trajectory.

![SHFE Lead Under Pressure Pulling Back After Hitting Highs, Closing Slightly Higher Intraday [SHFE Lead Brief Comment]](https://imgqn.smm.cn/usercenter/TmYox20251217171721.jpeg)