On May 20, 2026, Indonesian President Prabowo Subianto announced during a plenary session of the National Congress that the government has officially signed a groundbreaking regulation targeting the governance of natural resource exports. This bold policy framework will establish a dedicated state-managed natural resource export agency, executing exports through State-Owned Enterprises (BUMN) acting as government-designated single exporters.

According to local media disclosures and presentation slides shown during the session, this centralized mechanism will initially apply to palm oil, coal, and ferroalloys (paduan besi). Under this system, direct private export transactions will be phased out, forcing overseas buyers and Indonesian producers to route contracts, logistics, and payments entirely through state-appointed BUMN nodes.

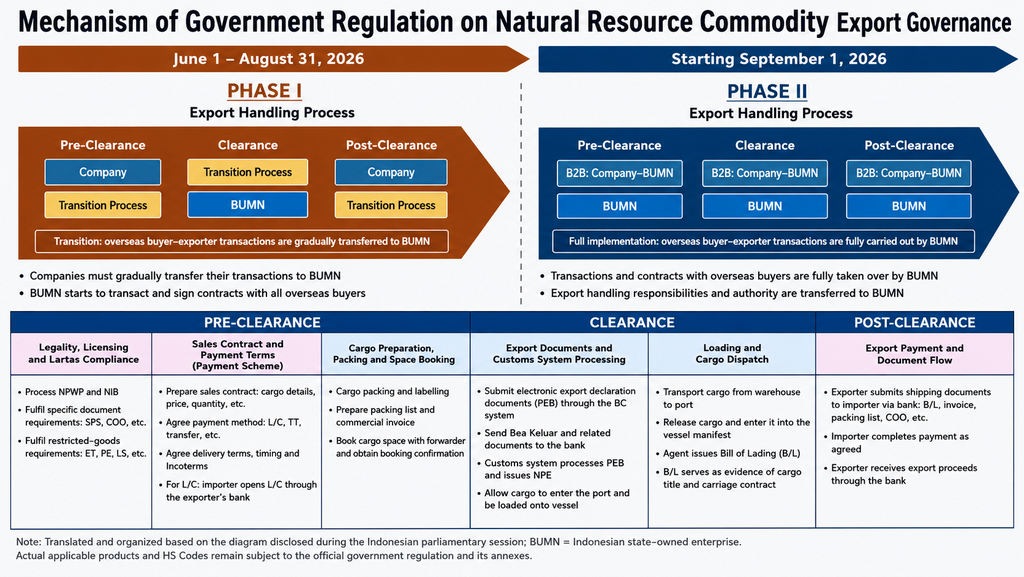

1. The Two-Phase Implementation Timeline

Based on the official policy schematic diagrams disclosed on-site, the transition to a centralized BUMN-led export model will occur in two distinct regulatory phases:

Phase 1 (Transition)

Time : June 1, 2026 - August 31, 2026

Mechanics : Private enterprises continue to manage some internal administrative and logistics steps. However, all existing and new import-export transactions with overseas buyers must begin a step-by-step migration to BUMN entities.

Phase 2 (Full Monopsony)

Time : September 1, 2026, Onward

Mechanics : Complete takeover. All transaction flows, sales contracts, export declarations, customs clearance, shipping arrangements, and the collection of export earnings (DHE) will be fully managed or led by designated BUMN.

2. Deep Structural Intervention: Pre- to Post-Clearance

This regulatory mechanism does not simply install a government "rubber stamp." Instead, it represents a fundamental reallocation of the entire export trade chain, deeply embedding BUMN across three key logistics and financial phases:

[Pre-Clearance] ──> [Clearance] ──> [Post-Clearance]

(Contracts & Docs) (Customs & Loading) (Payment & FX DHE)

-

Pre-Clearance (Contract & Goods Preparation): This covers verifying legality, IUP mining licenses, export restrictions (Lartas) compliance, sales contract drafting, finalizing payment terms, commercial invoicing, and vessel chartering/cabin bookings.

-

Clearance (Customs & Physical Shipment): Includes filing export declarations (PEB), managing customs system approvals, cargo transport from smelter warehouses to port terminals, loading shipments, and issuing Bills of Lading (B/L).

-

Post-Clearance (Documentation & Capital Flow): BUMN will act as the principal intermediary, dispatching trade documents (B/L, Commercial Invoice, Packing List, Certificate of Origin/COO) to the buyer's issuing bank and managing the repatriation of export proceeds (DHE) under strict domestic banking provisions.

3. The Billion-Dollar Question: Will NPI and FeNi be Classified as "Ferroalloys"?

For the global stainless steel and electric vehicle battery supply chains, the immediate focal point is how Indonesia defines the scope of "ferroalloy" (paduan besi). Market consensus strongly suggests that the "ferroalloys" under discussion are highly likely targeting Nickel Pig Iron (NPI), which represents a massive trade flow of approximately 11.5 million tons of Indonesian NPI exports in 2025.

However, because the official, legally binding regulation "signed" by the government has not yet been formally released to the public, further clarification is needed to verify the exact scope of affected materials.

Crucially, the leaked written draft of the regulation does not actually mention "ferroalloys" at all. The term "ferroalloy" (paduan besi) was only verbally highlighted and presented by President Prabowo during the House of Representatives Plenary Session (Rapat Paripurna DPR) on Wednesday (20/5).

According to the leaked draft text, the actual written scope of the law is structured as follows:

CHAPTER II: DETERMINATION OF STRATEGIC NATURAL RESOURCE COMMODITIES

Article 2 (1) Strategic Natural Resource Commodities subject to export governance include:

a. coal;

b. palm oil; and

c. other strategic natural resource commodities.

(2) The Government may amend the Strategic Natural Resource Commodities as referred to in paragraph (1) letters a and b, and establish other Strategic Natural Resource Commodities as referred to in letter c through a coordinated meeting (rapat koordinasi) led by:

a. the minister responsible for synchronization, coordination, and control of ministerial affairs in the field of the economy (Coordinating Minister for Economic Affairs / Menko Perekonomian); or

b. the minister responsible for synchronization, coordination, and control of ministerial affairs in the field of food (Coordinating Minister for Food / Menko Pangan), attended by relevant ministers/heads of non-ministerial agencies.

This clause reveals a crucial legal framework: any expansion of the export control list to designate NPI, FeNi, or related ferronickel alloys under "other strategic commodities" is strictly required to be determined through a formal coordinated meeting (rapat koordinasi) led by either the Coordinating Minister for Economic Affairs or the Coordinating Minister for Food.

Because the written regulation itself is silent on "ferroalloys," the legal scope of the policy has not been fixed yet. Until this high-level inter-ministerial coordination meeting (rapat koordinasi) takes place and issues a definitive annex list with matching HS codes, the practical impact on NPI trade remains pending official confirmation.

Should nickel-iron intermediates formally fall under the BUMN single-exporter mandate after this meeting, SMM foresees four critical structural disruptions:

I. Erosion of Direct Negotiation Flexibility

Currently, Indonesian NPI is sold through a highly flexible ecosystem of steel mills, global trading desks, independent brokers, and back-to-back supply contracts. Forcing these contracts to route through a single state exporter compresses the operational room for direct price discovery, spot volume locking, and rapid high-frequency reselling.

II. Absolute Export Price Transparency

By funneling all sales contracts, shipping invoices, and foreign exchange collection (DHE) through state-owned channels, the Indonesian government will gain real-time, absolute transparency over actual transaction prices. This complements Indonesia's ongoing tightening of domestic mining benchmarks (HPM), the annual RKAB quota system, and the strict requirement for export proceeds to be held in domestic bank accounts.

III. Disintermediation of Traders and Brokers

In-transit or port-stored nickel-iron inventories have historically served as highly liquid financial assets for brokers and traders who leverage transfer orders and back-to-back contracts. Standardizing all contract entities and payment channels under BUMN will squeeze the margins of non-producing traders, rendering physical spot market quotes highly rigid.

IV. Export Execution Delays

Migrating long-term off-take agreements to BUMN templates will trigger significant friction during the Phase 1 transition. SMM expects delays stemming from contract re-signings, banking channel adjustments, letter of credit (L/C) re-issuances, and initial administrative coordination at port customs, temporarily disrupting short-term port-arrival schedules.

4. Market and Price Impact Analysis (If NPI were to be Involved)

Short-Term Sentiment vs. Medium-Term Realities

-

Short-Term (Sentiment-Driven): The direct impact on physical NPI shipping volumes returning to China will remain limited during the initial transition window, as private exporters continue to assist with logistics. However, given tight domestic nickel ore supplies, production cuts at several RKEF plants, and already declining NPI shipments, the market will likely digest this announcement as a fresh supply-side threat, driving up bullish sentiment.

-

Medium-Term (Structural Shifts): If NPI is formally included in the HS code list, Chinese stainless steel mills will face centralized Indonesian state sellers. This will result in stronger payment scrutiny, fewer options for non-standard flexible transactions, and the virtual elimination of low-cost, off-market FOB deals.

Transaction Costs vs. Production Costs

Unlike mining-end disruptions such as rising HPM benchmarks, declining laterite ore grades, or restricted RKAB quotas, this export centralization policy does not directly raise the physical smelting cost of NPI. Instead, it functions as a tax on transaction efficiency, increasing compliance burdens, administrative delays, and state oversight on pricing. SMM concludes that the impact of this policy is an increase in "transaction-side friction" rather than raw production costs, which will ultimately support sellers' intentions to hold prices firm and reinforce the price rigidity of high-nickel pig iron.

5. SMM Outlook

Indonesia’s new export regulation signals that its resource nationalism is successfully extending its reach beyond the mine gate and tax office, directly into the global sales and trading arena.

However, the key takeaway is that nothing is legally set in stone for the nickel industry yet. Because the written regulation currently leaves the door open under "other strategic commodities," and the word "ferroalloy" was only delivered verbally by the President on Wednesday (20/5), the entire framework remains unfixed. The critical indicator for the nickel chain over the coming weeks is whether the upcoming inter-ministerial rapat koordinasi formally adopts the HS codes for NPI and FeNi into the final regulatory annex.

![[SMM Analysis] Can Indonesia import sulfuric acid as a substitute after the sulfur restriction?](https://imgqn.smm.cn/production/admin/votes/imagesDzORb20240320114304.png)

![[SMM Analysis] After Sulphur Restrictions, Can Indonesia Import Sulphuric Acid as a Replace?

Wait, let me reconsider the translation.

[SMM Analysis] After Sulphur Restrictions, Can Indonesia Import Sulphuric Acid to Replace It?](https://imgqn.smm.cn/usercenter/fzwTi20251217171733.jpg)

![[SMM Analysis] Regional price gaps stay high. Why have the high-price and low-price regions of sulfuric acid shifted?](https://imgqn.smm.cn/usercenter/tXxfd20251217171713.jpg)