SMM April 30:

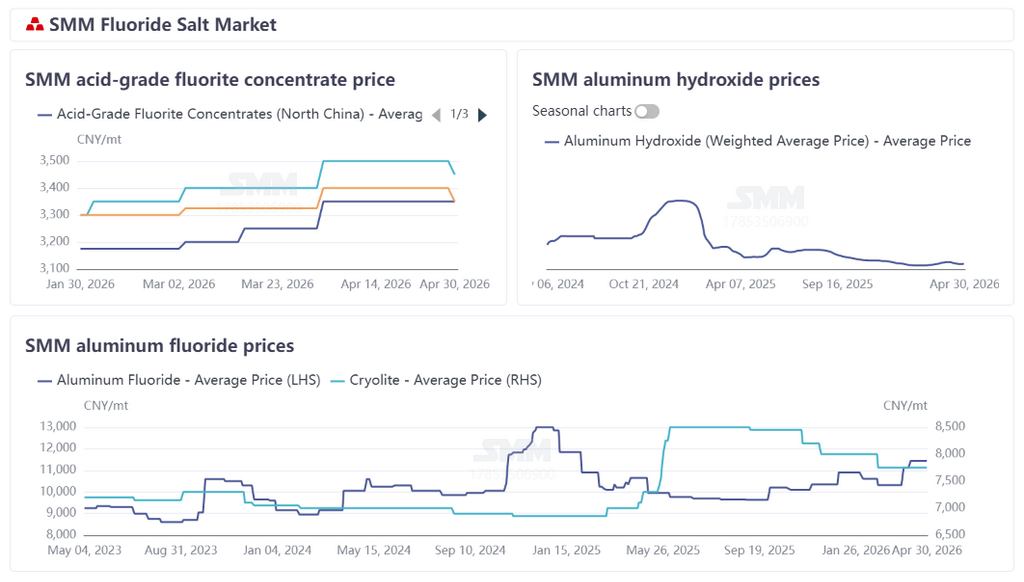

In April, aluminum fluoride prices shifted to a wide upward trend due to supply tightening and strong cost support. As of month-end, SMM aluminum fluoride prices closed at 10,980-11,900 yuan/mt. The cryolite market performed steadily overall, with SMM cryolite prices at 7,000-8,500 yuan/mt.

Raw material side: Supply disruptions lifted fluorite price center; policy ignited sulphuric acid market to retreat after rapid rise

In April, China's fluorite market prices fluctuated upward in early month then stabilized, with a slight pullback at month-end, and the overall price center edged up slightly. Supply side, affected by safety accidents in major producing areas, industry safety and environmental protection inspections continued to tighten, expanded in coverage, and strengthened in enforcement. Operating rates at mines and beneficiation plants in south China's core producing areas declined notably, supply volumes contracted sharply, forming a rigid contraction pattern. Enterprises generally held back from selling and held prices firm, with spot cargo circulation remaining tight. Combined with downstream hydrofluoric acid enterprises fully resuming production after the holiday, just-in-time procurement steadily recovered, and increased purchasing enthusiasm provided strong support for fluorite prices, with prices rising approximately 100 yuan/mt in early month. The market then operated steadily. At month-end, as operating rates in northern producing areas steadily rebounded and Mongolian imported supplies continued to supplement, the overall fluorite market supply trended toward looseness, and high-priced cargo transactions were clearly under pressure. Some traders' bearish sentiment intensified, actively cutting prices for shipments to recover funds. Combined with the approaching holiday, wait-and-see sentiment was strong in the market, in-market quotations became cautious, new orders were sluggish, and the focus was on digesting earlier orders. Although the sharp rise in downstream hydrofluoric acid prices at month-end boosted fluorite price-holding willingness to some extent, and delayed production resumptions at Zhejiang mining areas due to safety accidents and periodically low inventory also formed localized support, offsetting some downward pressure, these factors could not offset the bearish pressure from loose supply and sluggish trading, and fluorite prices showed a slight downward trend overall. As of April 30, SMM 97% fluorite powder average delivery-to-factory price reached 3,383 yuan/mt, up 1.74% from March 31. As another core raw material for aluminum fluoride, the aluminum hydroxide market was under pressure from alumina prices fluctuating downward, with aluminum hydroxide prices under pressure. As of April 30, SMM's average ex-factory price for aluminum hydroxide was 1,660 yuan/mt, down 3.09% from March 31. Additionally, in the sulphuric acid market, China's sulphuric acid market prices in April continued March's upward momentum overall, fluctuating at highs and retreating after rapid rise, with the monthly price center rising further MoM, but the MoM increase narrowing marginally. Shandong 98% sulphuric acid prices surged to 2,000-2,050 yuan/mt within the month, then gradually pulled back due to weak downstream purchasing at high levels and increased profit-taking shipments, falling to 1,600-1,700 yuan/mt at month-end. After the export control policy was officially announced on April 10, market sentiment was ignited in early-to-mid month with prices surging, then pulled back in late month as demand slowed down and profit-taking occurred. Near month-end as the ban approached implementation, market participants' wait-and-see sentiment intensified, trading turned sluggish, and the market shifted from high-level rises to cautious consolidation. Overall, the rise in fluorite and sulphuric acid prices in April provided strong cost support for aluminum fluoride prices.

Supply and Demand: Losses Suppress Aluminum Fluoride Operating Rates, May Supply-Demand Pattern Generally Stable with Slight Fall

In terms of supply, a negative cycle of rigid cost increases — deeply pressured profitability — low willingness to operate has emerged. In April, the price centers of fluorite and sulphuric acid continued to rise, but aluminum hydroxide prices pulled back. Overall, aluminum fluoride production costs remained high. The industry was deeply mired in losses and cost inversion, enterprise production enthusiasm remained weak, and the overall industry operating rate stayed at a low level around 40%. Even though spot prices recovered slightly, they could hardly fully cover incremental raw material costs. Enterprise profitability saw no substantial improvement, and low-load production and active production cuts became the industry norm. Demand side, downstream operating aluminum capacity stayed high and stable, forming sustained rigid floor demand for aluminum fluoride. In April, downstream aluminum enterprises overall maintained a pace of restocking based on rigid demand and purchasing as needed, with no concentrated large-scale stockpiling behavior. Demand was released steadily overall, with no significant increase or decrease. Looking ahead to May, the high raw material support pattern is difficult to break, aluminum fluoride cost pressure is expected to continue, industry losses are hard to reverse, and the trend of low operating rates and low inventory at enterprises may further solidify. Downstream operating aluminum capacity remains robust, rigid demand support stays strong, and the demand side continues to be dominated by purchasing as needed and steady consumption. The supply-demand pattern continues to feature weak supply and stable demand.

Overall, in early April, downstream benchmark aluminum enterprises raised tender prices significantly, up 770-800 yuan/mt MoM, ultimately settling in the range of 10,980-11,050 yuan/mt. By mid-month, as sulphuric acid prices continued to surge, aluminum enterprises' procurement tender prices rose to around 11,500-11,800 yuan/mt under cost support, driving market prices further up. Currently, although raw material markets showed divergent changes, the overall high comprehensive cost pattern remained unchanged, still providing price support for next month. In terms of supply, due to high production costs, enterprise operating enthusiasm was poor, and market supply is still expected to shrink. Demand side, the aluminum industry was dominated by rigid demand, lacking obvious positive factors to boost consumption. Overall, cost support remains strong, supply is tightening while demand is stable, and prices are expected to rise further next month. Close attention should be paid to dynamic changes in raw material costs and adjustments in downstream procurement pace going forward.