- What Is "Borrowing Ships to Go Global"?— Definition and Estimation Logic of Indirect Steel Exports

"Indirect steel trade" refers to steel that is not exported in the form of raw materials, but rather embedded as parts or structural materials in finished products such as machinery equipment, automobiles, and home appliances, achieving implicit exports through the cross-border trade of these goods.

SMM Indirect Steel Export Model: Based on the volume of finished steel consumed per mt/unit/set of specific finished products, approximately 43 categories of steel-containing products covering a total of 497 tariff codes are classified in detail according to the Harmonized Commodity Description and Coding System (HS codes, up to 8 digits). SMM categorises indirect export data into six major industry segments: machinery, home appliances, motorcycles & bicycles, automobiles, containers, and steel products.

- The "Steel Torrent" Hidden in Manufacturing— Scale and Landscape of Indirect Steel Exports

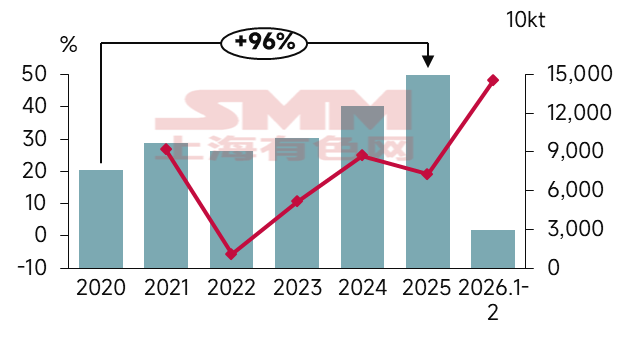

Steel Indirect Export Data, 2020-2026

Data source: SMM; General Administration of Customs

From 2020 to 2021, China, benefiting from supply chain integrity and efforts to ensure supply and stabilise prices, maintained rapid growth in indirect exports even during the pandemic;

In 2022, as the severity of the pandemic eased and major central banks such as the US Fed aggressively raised interest rates to curb high inflation, global manufacturing sentiment pulled back. Coupled with the very high base in 2021, when the "stay-at-home economy" and supply chain congestion drove a surge in global demand for Chinese-manufactured goods, 2022 represented a natural cooling as the dividend faded;

In 2023, China's indirect steel exports reversed course, with the YoY growth rate turning from negative to positive, and maintained rapid growth for three consecutive years;

By 2025, China's total indirect steel exports grew approximately 96% compared to 2020. In the first two months of 2026, cumulative indirect steel exports totalled 29.43 million mt, with a YoY growth rate of 48.07%.

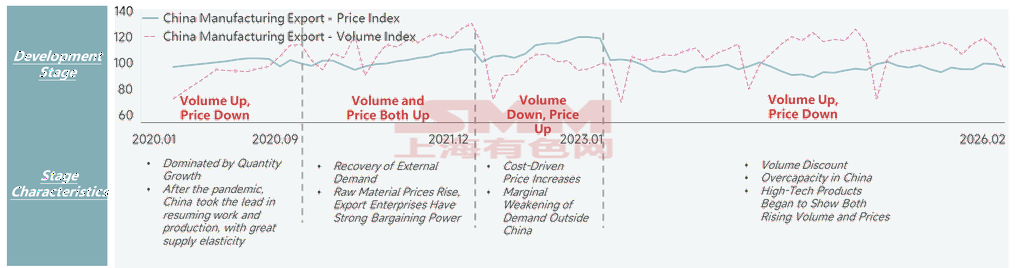

Analysis of China's Manufacturing Export Price & Volume Index (MoM) Curves

Data source: General Administration of Customs

Contrary to the increase in indirect exports, China's manufacturing export price index declined. In 2021, China's manufacturing export price and volume indices exhibited a rare phenomenon of "simultaneous price and volume increases," driven by the gradual recovery of the global economy — particularly the sustained production recovery in Europe and the US — which boosted China's exports of production-related products. The price increases were primarily cost-driven, as upstream raw material prices (non-ferrous metals, steel, etc.) surged sharply, compounded by global supply chain shortages and soaring ocean freight rates. Over the subsequent four years, prices and volumes exhibited clearly opposite trends. As of February 2026, China's manufacturing export price index stood at 97.4, down 8.2 from its historical same-period high, while China's manufacturing export volume index stood at 95.9, up 20.9 from its historical same-period high. This indicates that China's manufacturing exports remain in a relatively fragile stage of "volume discount."

- Who Is Driving This "Invisible Giant Ship"?— The "Twin Engines" Behind High GrowthHigh Growth in Indirect Steel Exports Driven by Recovery of Manufacturing Outside China

China's Indirect Steel Exports by Product Category

Data source: SMM; General Administration of Customs

Global Major Regions Manufacturing PMI Index, 2021-2026

Data source: China Federation of Logistics & Purchasing

According to the SMM indirect steel export model, from January to December 2025, total indirect steel exports reached 149.64 million mt, +19.10% YoY. The reasons behind this were inseparable from the strong boost of downstream manufacturing exports and the diversification of export markets. Specifically, machinery, steel products, and automobiles remained the main drivers of indirect steel exports, with machinery +21.38% YoY, steel products +19.30% YoY, and automobiles +28.66% YoY, contributing 48.05%, 28.91%, and 16.90% to total export growth, respectively. The growth in ex-China demand was also inseparable from the recovery of manufacturing outside China. Since 2023, PMI readings in major regions have been on a rebound trend from the bottom, but due to the overall slow pace of recovery, some regions remained below the 50 mark, resulting in strong dependence outside China on price-competitive finished steel products exported from China.

Indirect Steel Exports Accelerating Shift Toward Emerging Markets

On the other hand, to cope with increasing trade barriers in some developed markets, export markets accelerated their shift toward emerging markets along the Belt and Road Initiative (ASEAN, West Asia, Africa, etc.). For example, the share of indirect exports to regions such as ASEAN and the BRICS Ten increased notably. See the charts below for specific data.

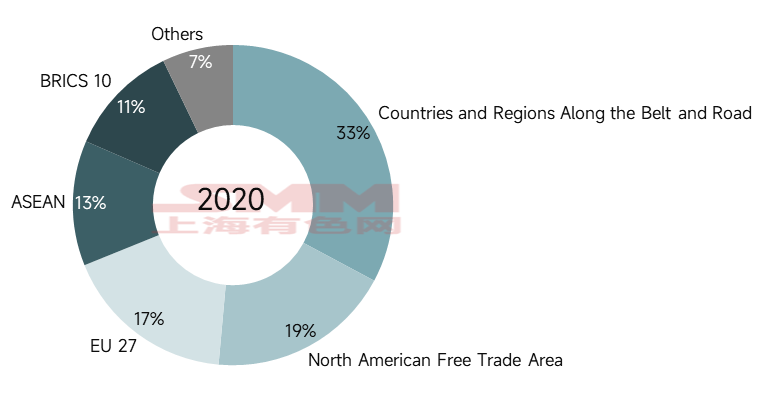

China's Indirect Steel Exports by Economic Zone (2020)

Data source: SMM

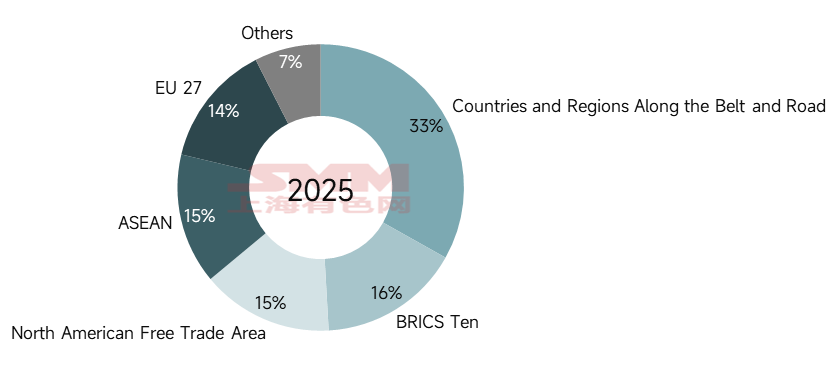

China's Indirect Steel Exports by Economic Zone (2025)

Data source: SMM

According to the SMM indirect export model, in 2025, China's total steel consumption for indirect steel exports to countries and regions along the Belt and Road Initiative reached 49.5966 million mt, accounting for 33% of China's total indirect steel exports, a share largely unchanged from 2020. The economic zones with more notable changes were mainly NAFTA, EU-27, ASEAN, and the BRICS Ten. Among them, NAFTA and EU-27 showed a declining trend, with shares dropping by 4% and 3%, respectively; ASEAN and the BRICS Ten showed an upward trend, with shares rising by 2% and 5%, respectively. The incremental volumes from these regions effectively offset the gap left by declining exports to Europe and the US. As of 2025, the share of China's indirect steel exports to the US dropped by 4% compared to 2020, the share to Japan fell by 2%, and the share to Germany fell by 2%, with some European countries even removed from the top 15 export destinations (the Netherlands). ASEAN countries saw increasingly robust demand for NEVs, PV, and smart devices. The signing of the China-ASEAN Free Trade Area 3.0 added chapters on the digital economy and green economy, removing institutional barriers for such product exports. BRICS countries had robust demand in infrastructure and agriculture, directly boosting China's exports of related equipment. On the other hand, many ASEAN countries imported core parts and intermediate products from China, assembled them locally, and then re-exported globally, forming an industry chain division-of-labor network of "R&D in China, production in neighboring countries, markets worldwide."

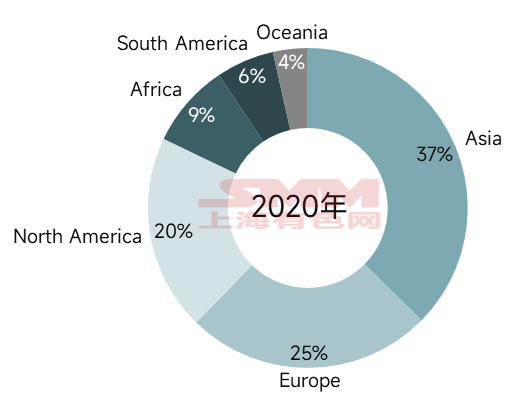

China's Indirect Steel Exports by Continent (2020)

Data source: SMM

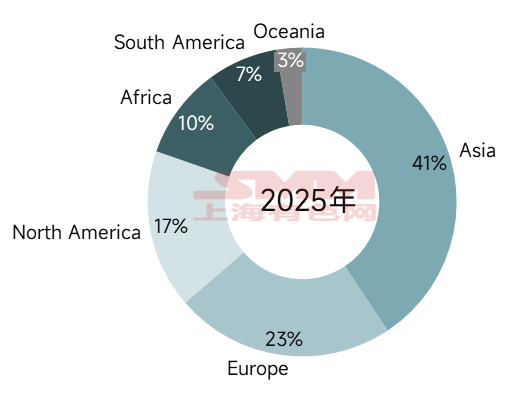

China's Indirect Steel Exports by Continent (2025)

Data source: SMM

By continent, Asia remained the primary destination for China's indirect steel exports. As of 2025, China's indirect steel exports to Asia totaled 60.8719 million mt, accounting for 41% of China's total indirect steel exports. The share of North America declined, while the shares of Africa and South America rose accordingly.

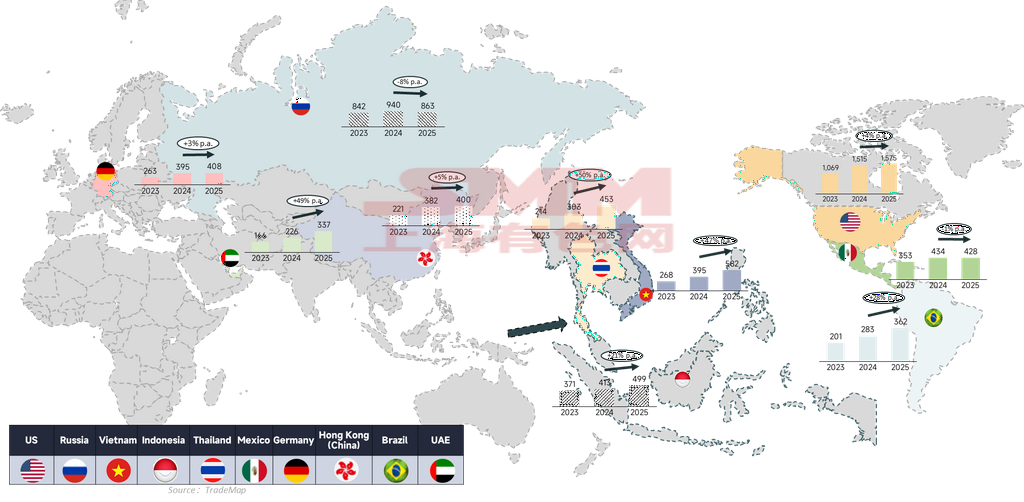

Top 10 Destination Markets for China's Indirect Steel Exports

Data source: SMM

Based on the historical changes in the top 10 destinations for China's indirect steel exports, the compound growth rate of the original major destination markets — European and American countries — has been narrowing, while destination markets led by Southeast Asia and the Middle East have been climbing rapidly at a compound growth rate exceeding 20%. The US share of China's indirect steel exports has also been declining from 15% in 2020 to 10% in 2025. Meanwhile, the shares of major Southeast Asian countries and the UAE rose from 8% and 1.2% to 10.3% and 2.3%, respectively.

- The "Cost" of Growth— When "Steel Going Global" Meets the "Pain of Backlash"First, Strong Exports Led to Excessive External Dependence

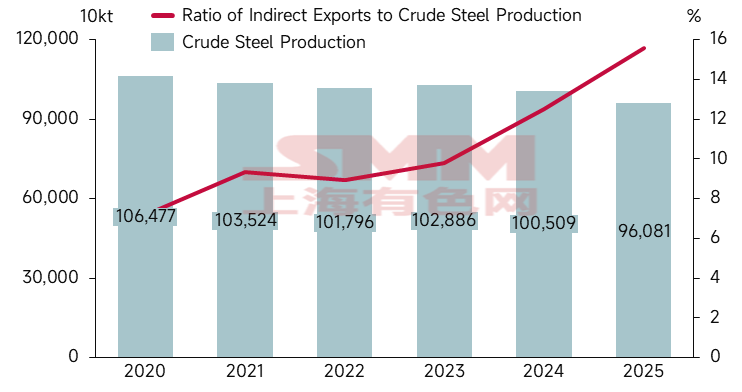

Trends in China's Indirect Steel Exports & Crude Steel Production

Data source: SMM; General Administration of Customs;

According to data from the National Bureau of Statistics, cumulative crude steel production in 2025 totaled 960.81 million mt, while indirect exports reached 149.64 million mt, accounting for as high as 15.57%, up 8.42% from the 2020 ratio. If direct steel exports were also factored in, the ratio would be as high as 29%, meaning that nearly one-third of China's crude steel supply relied on ex-China consumption for absorption. The deep adjustment in China's real estate sector caused domestic steel consumption to decline for the fifth consecutive year, and the difficulty in reducing crude steel production and the slow pace of transformation made exports an inevitable "flood discharge channel."

Looking at the external dependence of some major industries, the external dependence of containers exceeded 100% in 2025, mainly because export data reflected not only current-period production but also the drawdown of prior inventory. In 2024, due to the "Red Sea crisis," the industry entered a "frantic stockpiling" mode, and in 2025, as the impact of the crisis waned, it switched to a "rational destocking" mode. Refrigerators ranked second in external dependence. The structural adjustment of global refrigerator capacity featuring "rising in the East and declining in the West" provided a historic opportunity for China's refrigerator exports. Following closely were motorcycles and bicycles, for which the shrinking Chinese market left no choice but to seek the "blue ocean of demand" in Latin American countries.

Data source: SMM

Second, Strong Exports Led to Escalating Trade Disputes

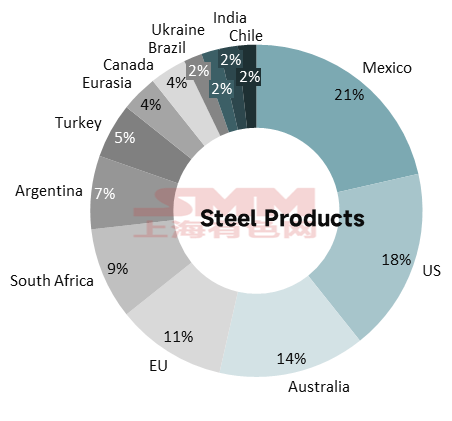

Anti-dumping Cases Against Chinese Steel Products Since 2020

Data source: SMM; China Trade Remedies Information

However, this model of "insufficient domestic demand supplemented by exports" was encountering increasingly severe external challenges. Since 2020, industries related to China's indirect steel exports faced 143 overseas anti-dumping investigations (tallied based on the timing of their latest developments). As steel products were involved in the most cases, they are presented in a pie chart, which shows that Mexico, the US, and Australia initiated the most anti-dumping actions against Chinese steel products, together accounting for over 50%.

Anti-dumping Cases Against Chinese Home Appliances,Automobiles, Machinery, etc. Since 2020

Data source: SMM; China Trade Remedies Information

In the home appliance industry, Turkey and Argentina, through continuous "sunset reviews," extended anti-dumping duties on Chinese air conditioners for nearly twenty years, forming DAS solar and stable trade barrier. In the washing machine industry, the sector was facing a three-dimensional siege of complete units plus parts, anti-dumping plus carbon tariffs, and traditional markets plus emerging markets. Water heaters were involved in a relatively large number of cases, but among them, Uruguay's anti-dumping measures expired in 2025, while Ukraine was still in the investigation phase. Refrigerators and microwave ovens encountered fewer anti-dumping investigations.

In the automobile industry, overseas anti-dumping investigations against China-related automotive products showed a trend of a continuously increasing number of cases, with products involved expanding from parts to complete vehicles, and emerging markets becoming new battlegrounds. There were only 4 anti-dumping cases against complete vehicles, among which Tunisia and the Philippines had no updated developments for the time being, while the EU and US anti-dumping measures against Chinese automobiles remained in their enforcement period.

Compared with the automobile and home appliance industries, although the motorcycle and bicycle industry faced a relatively small number of direct anti-dumping cases, two notable characteristics emerged: first, extremely long duration — some cases had been extended for over 30 years through sunset reviews; second, sharp recent increases in duty rates — Mexico's anti-dumping duty on Chinese children's bicycles surged from $13.12/unit to $57.19/unit (preliminary ruling), an increase of over three times.

The machinery industry faced anti-dumping actions involving the widest range of countries, and the trend was escalating from traditional anti-dumping to Section 337 investigations — the US was increasingly launching investigations against Chinese machinery products on the grounds of intellectual property infringement, a trade restriction measure more severe and costlier to defend against than anti-dumping. Since 2024, the US launched Section 337 investigations into Chinese construction machinery, industrial machinery, and sports equipment, among others.

Beyond anti-dumping measures targeting specific industries, China's manufacturing sector also faced a category of comprehensive trade barriers, as detailed in the table below.

Data source: SMM

- What Lies Ahead?— The Path from "Indirect" to "Value"The Growth Trend of Indirect Steel Exports Remains Unchanged

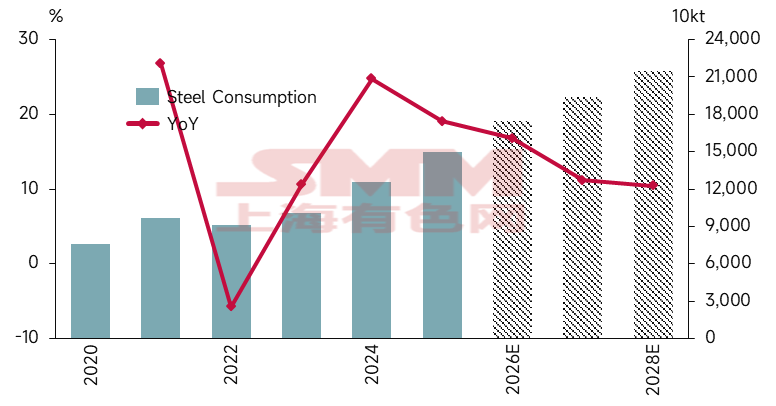

Total Indirect Steel Exports

Data source: SMM; General Administration of Customs

Overall, SMM forecasts that indirect steel exports will grow by approximately 17% in 2026. Going forward, indirect steel exports will maintain a solid growth trend, but the growth rate will gradually slow down. In the long term, the iron element export model relying on manufacturing remains reliable, primarily driven by the mutual reinforcement between China's manufacturing scale and supply capabilities and the industrialization and urbanization demand in emerging markets.

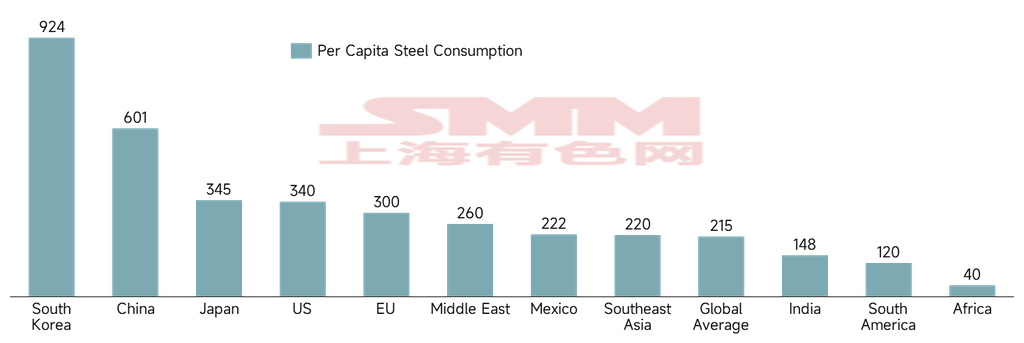

Per Capita Steel Consumption by Major Countries and Regions

Data source: World Steel Association

Per capita steel consumption in Southeast Asia, India, the Middle East, South America, and Africa remains relatively low. According to worldsteel, per capita steel consumption in 2024 for these five regions was 220, 215, 260, 120, and 40 kg, respectively, with South America and Africa significantly below the global average. It can be said that the export competitiveness of China's manufacturing sector has met the requirements of emerging markets for scale and efficiency during urbanization/industrialization, lowering the development threshold to a certain extent. The relatively broad demand space ex-China has also matched the release of China's manufacturing capacity.

Specific industries: Machinery sector, with the global economy undergoing a mild recovery, global end-user growth in the construction machinery industry will drive export demand. Currently, overseas gross margins for construction machinery are generally 5–10% higher than in China, and there is still significant room for expansion in market share and product categories. Therefore, machinery exports are expected to further increase in 2026. Automobile sector, as the marginal effects of "trade-in" and "retirement subsidy" policies diminish, coupled with the halving of purchase tax reduction and exemption policies, growth in the Chinese market will slow down, and "going global" will become an inevitable path for automakers. Currently, NEV penetration rates in Europe, Southeast Asia, Latin America, and other markets remain low, and acceptance of Chinese brands continues to rise. Exports are still expected to increase in 2026, but as China's market share grows, trade barrier risks should be watched closely. Home appliance sector, home appliance exports in 2026 are expected to achieve mild growth on the basis of 2025, with emerging markets becoming the primary growth engine. Container sector, with the "super replacement cycle" ending and concentrated delivery of container ships causing capacity surplus, there is still a possibility of negative YoY growth.

In the long term, China's manufacturing sector has demonstrated strong competitiveness in the global market, and total exports of related industries are expected to maintain rapid growth over the next five years. Breaking Through: An Imperative Path Forward

As China's indirect steel exports have surged rapidly, the country is currently facing multiple challenges: intensifying external barriers, rising internal costs, low-end lock-in within the value chain, and the restructuring of global division of labor. To break through, the core lies in shifting from price competition to value competition, and from scale expansion to quality- and innovation-driven growth.

1 Strategic Upgrade: From "Products Going Global" to "Manufacturing Taking Root"

Deploy a "China+N" capacity layout, circumventing tariff barriers through a "China + Southeast Asia/Mexico/Middle East" capacity configuration; build "micro-factories" by establishing highly automated assembly plants in Europe and other regions to achieve localized production and delivery.

2 Market Expansion: Diversified Layout and Deep Cultivation of the "Global South"

Develop emerging markets by redirecting export growth drivers toward the "Global south" markets in Asia, Africa, and Latin America, reducing dependence on any single market; deepen channel penetration by leveraging cross-border e-commerce, overseas warehouses, and other new business models to build omni-channel sales networks covering major markets.

3 Value Reshaping: Technology-Driven and Brand Elevation

Define standards through technological iteration—in fields such as robotic lawn mowers and new energy, establish generational advantages through RTK vision, AI algorithms, and other technologies, shifting from "selling products" to "setting standards"; build local brands by moving beyond the pure toll processing model, and through sponsoring communities, embracing ESG standards, and hiring localized teams, create brands with emotional resonance.

4 Policy and Systemic Support: Optimizing the Ecosystem and Ensuring Compliance

Strengthen financial support by establishing manufacturing overseas development funds, improving overseas investment insurance systems, and utilizing cross-border financial service solutions to manage exchange rate risks; build comprehensive overseas service systems by leveraging national-level overseas comprehensive service platforms to provide one-stop services for hundreds of thousands of foreign trade entities, while strengthening legal and compliance guidance; regulate overseas competition by leveraging the role of industry associations, implementing coordinated "united front" coopetition strategies, prohibiting low-price dumping, and fundamentally resolving the problem of "exporting involution."

5 Mechanism and Pathway Reshaping: Governing Vicious Competition and Safeguarding Value Exports

The ongoing anti-involution campaign in China has formed a synergistic relationship with indirect steel exports, driving a shift from "scale competition" to "value upgrading." By governing disorderly competition within China and guiding steel to be exported in higher value-added forms (such as automobiles and machinery), industrial upgrading can be achieved, transforming steel exports from the form of "raw materials" to exports of "parts" or "finished products" embedded in global supply chains. Data Source Disclaimer: Data other than publicly available information is derived by SMM based on public information, market communication, and SMM's internal database models, and is for reference only and does not constitute decision-making advice.

Note: This article is an original article of this official account. For any needs regarding reprinting, whitelisting, or cooperation, please contact us. Without permission, the above content shall not be reprinted, modified, used, sold, transferred, displayed, translated, compiled, disseminated, or disclosed to any third party in any other form, nor shall any third party be licensed to use it. Otherwise, once discovered, SMM will pursue legal action for infringement liability, including but not limited to claiming contractual breach liability, return of unjust enrichment, and compensation for direct and indirect economic losses.

![[SMM Steel] Hoa Phat posts over VND 9 trillion Q1 profit, expects stronger performance ahead](https://imgqn.smm.cn/usercenter/wSpkX20251217171718.png)

![[SMM Steel] Turkey targets $17bn steel exports in 2026, maintains 20 Mt shipment outlook](https://imgqn.smm.cn/usercenter/aPBtI20251217171717.jpg)

![[SMM Steel] Japan steel consumption rises 1.8% YoY in Jan–Feb 2026, driven by autos](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)