Esta semana (20–26 de março de 2026), os preços dos materiais para baterias de estado sólido apresentaram divergência estrutural: os preços do LPSC da rota de sulfetos e do sulfeto de lítio caíram, enquanto os óxidos permaneceram estáveis. No lado industrial, a bateria semissólida para veículos de duas rodas da Taiblue–Yadea alcançou lançamento comercial; os pedidos de eletrólitos sólidos da BTR dispararam; e o projeto de 2 bilhões de yuans da WELION New Energy foi instalado em Huadu, Guangzhou. Os cortes de preços a montante repercutiram na implementação a jusante, acelerando o processo de comercialização.

Recentemente, houve muitas conferências do setor na área de baterias de estado sólido, dentro e fora da China, e as empresas participaram ativamente ou realizaram eventos de lançamento de produtos. Fora da China, a MG lançou uma bateria semissólida com baixo teor de eletrólito líquido e deve entrar na Europa em 2026; a QuantumScape divulgou sua estratégia de comercialização para baterias de lítio-metal de estado sólido. Na China, os pedidos de eletrólitos sólidos da BTR dispararam, e sua linha de produção de óxidos já havia sido concluída; o projeto de baterias de estado sólido de 2 bilhões de yuans da WELION New Energy foi instalado em Huadu, Guangzhou; e a bateria semissólida para veículos de duas rodas desenvolvida em conjunto pela Taiblue e pela Yadea alcançou lançamento comercial.

I. Rota dos sulfetos: preços dos materiais sob pressão, expectativas de industrialização em alta

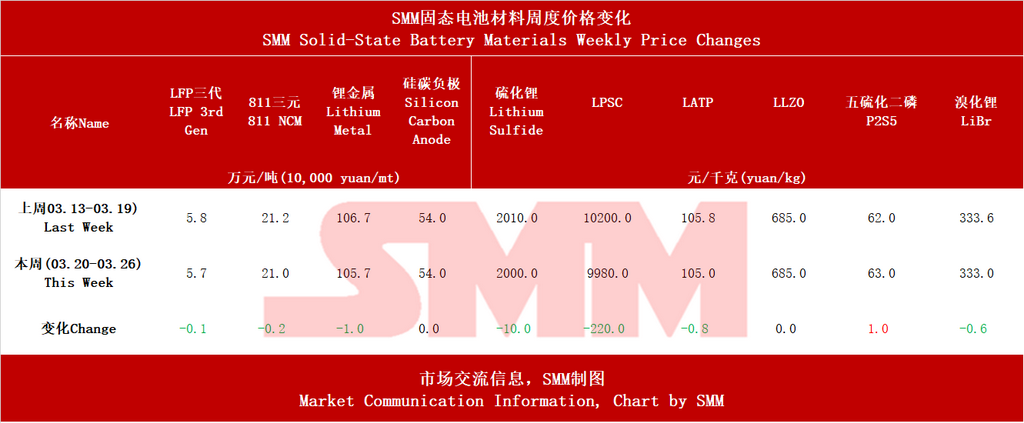

Nesta semana, os preços das principais matérias-primas para eletrólitos sólidos à base de sulfetos registraram queda clara. O preço médio do sulfeto de lítio grau bateria caiu para 2.000 yuans/kg, uma redução semanal de 10 yuans; o LPSC (eletrólito do tipo minério prata-germânio) recuou 220 yuans, para 9.980 yuans/kg, queda de 2,2%. Sustentado pela força dos preços do enxofre, o precursor P₂S₅ subiu levemente 1 yuan, para 63 yuans/kg, na contramão da tendência.

Em 23 de março, a BTR divulgou que seus pedidos de eletrólitos sólidos haviam disparado; sua linha de produção de óxidos na escala de 1.000 toneladas já havia sido concluída; e suas vendas de eletrólitos de óxido superaram 100 toneladas em 2025. Em seguida, a Lishen Battery e a FAW Co., Ltd. anunciaram patentes relacionadas a eletrólitos sólidos à base de sulfetos. A rota dos sulfetos é considerada a direção final das baterias totalmente de estado sólido devido à sua vantagem em condutividade iônica; a queda dos preços no lado dos materiais ajuda a reduzir os custos dos sistemas de bateria e a acelerar a industrialização.

II. Rota de Óxido/Polímero: Primeiros Avanços na Comercialização

O progresso da comercialização nas rotas de óxido e polímero concentrou-se esta semana. A motocicleta elétrica de alta gama equipada com a bateria semissólida co-desenvolvida pela Taiblue New Energy e pela Yadea, a “Guaneng Xingjian II-200L”, entrou em comercialização, marcando o primeiro avanço no cenário de veículos de duas rodas. A Sinopec concluiu, em Suzhou, um projeto de demonstração de microrrede com bateria de estado sólido de polímero; após um mês de operação, adotou um eletrólito sólido polimérico desenvolvido de forma independente pelo Instituto de Pesquisa em Processamento de Petróleo da Sinopec. Os produtos de bateria de estado sólido da DARE Auto fizeram sua estreia no exterior no Tokyo Battery Show e na Exposição Australiana de Armazenamento de Energia.

Em termos de preços, os eletrólitos de óxido LATP e LLZO permaneceram estáveis esta semana em 105 yuans/kg e 685 yuans/kg, respectivamente. Devido à maior maturidade do processo, a rota de óxido já atendia às condições de comercialização em cenários com exigências de densidade energética relativamente moderadas, como veículos de duas rodas e armazenamento de energia.

III. Cátodo e Ânodo: Leves Quedas de Preço, Silício-Carbono Estável

Esta semana, o LFP de 3ª geração caiu 1.000 yuans, para 57.000 yuans/t, e o ternário 811 caiu 2.000 yuans, para 210.000 yuans/t. O lítio metálico recuou 1 yuan, para 105,7 yuans/g. O preço do ânodo de silício-carbono permaneceu estável em 54 yuans/kg.

A queda nos preços dos materiais catódicos foi impulsionada principalmente pelo lado das matérias-primas, como o carbonato de lítio, com correlação relativamente indireta com as baterias de estado sólido. Como material-chave para baterias de alta densidade energética, a estabilidade do preço dos ânodos de silício-carbono refletiu um padrão de oferta e demanda relativamente equilibrado.

IV. Tendências do Setor

A rota de sulfeto entrou em uma fase de otimização de custos: com a queda dos preços de LPSC e sulfeto de lítio avançando em paralelo com a expansão da capacidade (BTR) e a implantação de patentes (Lishen, FAW), o setor estava passando da validação técnica para a viabilidade econômica.

A implementação comercial mostrou “duas frentes avançando juntas”: Taiblue–Yadea (veículos de duas rodas), a microrrede da Sinopec (armazenamento de energia) e MG SolidCore (automotivo) alcançaram avanços em diferentes cenários de aplicação, esclarecendo a trajetória de comercialização “progressiva” das baterias de estado sólido.

Os avanços no exterior reforçaram as expectativas de longo prazo: a QuantumScape divulgou sua estratégia de comercialização para baterias de lítio-metal em estado sólido; e uma parceria tripartite entre a sul-coreana Kumho Petrochemical, a POSCO e a BEI desenvolvia uma bateria de lítio-metal sem ânodo, enquanto gigantes internacionais aceleravam sua expansão em tecnologias de próxima geração.

Segundo as previsões da SMM, os embarques de baterias totalmente em estado sólido alcançarão 13,5 GWh até 2028, enquanto os de baterias semissólidas chegarão a 160 GWh. A demanda global por baterias de íons de lítio deve atingir aproximadamente 2.800 GWh até 2030, com a demanda do setor de veículos elétricos apresentando uma CAGR de cerca de 11% entre 2024 e 2030, a demanda de baterias de íons de lítio para armazenamento de energia (ESS) com CAGR de cerca de 27%, e a demanda de baterias de lítio para eletrônicos de consumo com CAGR de aproximadamente 10%. A penetração global das baterias de estado sólido é estimada em cerca de 0,1% em 2025, com a penetração das baterias totalmente em estado sólido devendo alcançar cerca de 4% até 2030, e a penetração global das baterias de estado sólido podendo se aproximar de 10% até 2035.

**Nota:** Para mais detalhes ou consultas sobre o desenvolvimento de baterias de estado sólido, entre em contato com:

Telefone: 021-20707860 (ou WeChat: 13585549799)

Contato: Chaoxing Yang. Obrigado!

![[Bateria de Lítio: Produtos da Tianli Lithium Energy Compatíveis com Rotas de Estado Sólido Alcançam Remessas em Massa]](https://imgqn.smm.cn/usercenter/MbKXH20251217171730.jpg)