2.28

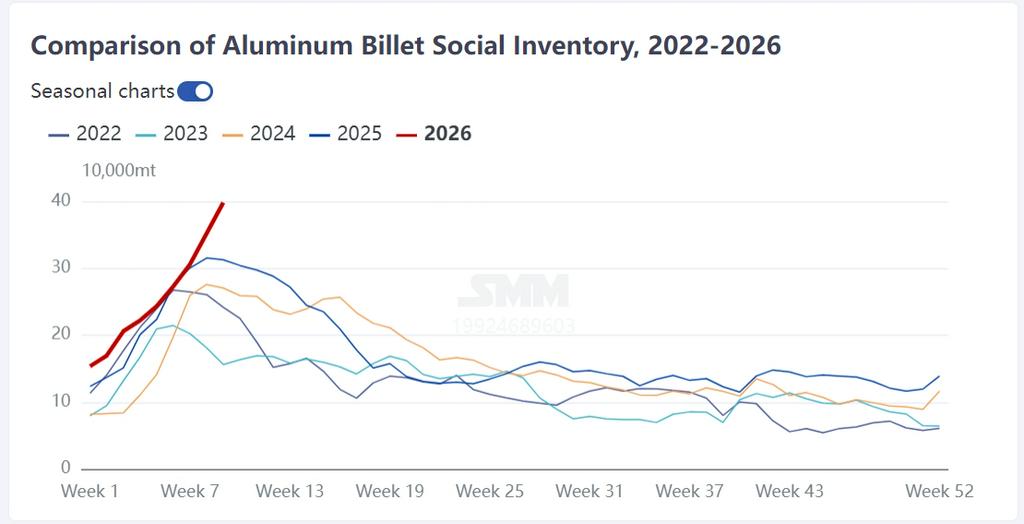

According to SMM survey, as of February 26, social inventory of aluminum billets in mainstream domestic consumption areas reached 398,000 mt, approaching the 400,000 mt mark. The absolute inventory level hit a new high in nearly five years, and the inventory buildup trend has not eased, with the inventory inflection point yet to emerge. In terms of the accumulation magnitude, aluminum billet inventory accumulated a total of 93,000 mt after the Chinese New Year holiday in 2026, higher than the average annual accumulation of 70,500 mt over the past four years, significantly exceeding market expectations.

Why does aluminum billet inventory continue to accumulate at a high speed without showing a peak, even though it is already at a historically high level?

Supply side, despite negative factors such as weakening downstream demand and sluggish market purchasing during the Chinese New Year holiday, aluminum billet producers, as the main consumer in the aluminum industry, mostly maintained normal production pace. Moreover, the contract breach costs between billet producers and aluminum smelters are significant, further limiting production cuts during the holiday. According to SMM survey statistics, expected aluminum billet production in February is 1.13 million mt. After adjusting for the number of days in the month, the expected operating rate for February is 45.7%, down 3.85 percentage points MoM from January, indicating a relatively limited decline. Therefore, the limited supply reduction during the holiday laid the groundwork for post-holiday inventory breaking historical highs.

Demand side, January and February typically enter the off-season each year. Additionally, the sharp rise in aluminum prices in January directly led to downstream extrusion plants choosing early holidays with slightly extended breaks. Furthermore, as aluminum prices remained at historically high levels, manufacturers opted to reduce raw material stockpiling to minimize capital occupation and price fluctuation risks. Thus, under the triple impact of seasonal off-season, extended holidays, and reduced stockpiling, trading sentiment in the aluminum billet market remained sluggish. With slow downstream resumption progress, the pace of aluminum billet inventory buildup has not eased.

How will social inventory of aluminum billets evolve going forward?

Currently, in industrial extrusions, new energy-related orders such as PV and batteries perform well. Adjustments to export tax rebate policies for PV and batteries are about to trigger a rush to export, and the resumption progress at industrial extrusion plants is optimistic. In contrast, building extrusion plants, whose latest resumption period is concentrated around the Lantern Festival, have shown slow progress after resumption, lacking strong order support for production. Therefore, the inflection point for aluminum billet inventory depends closely on downstream resumption progress. Entering March, aluminum billet producers will gradually resume production due to contract obligations, adding further pressure to the supply side. The industry's supply-demand pattern has not yet entered a virtuous cycle. In the short term, aluminum billet inventory is expected to fluctuate between 400,000-450,000 mt in early to mid-March. Whether an inventory inflection point can be achieved depends not only on the resumption of extrusion plants but also on the sustainability of production at aluminum billet manufacturers.