Survey Data on Operating Rates of Secondary Aluminum Alloy Enterprises by Region and Scale in June 2026:

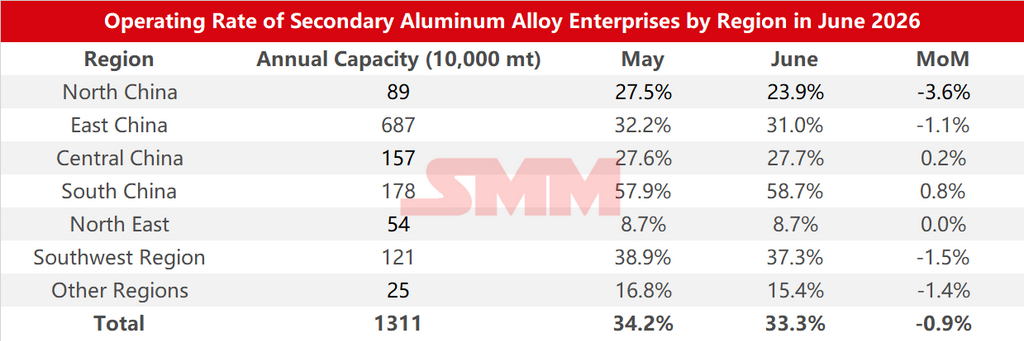

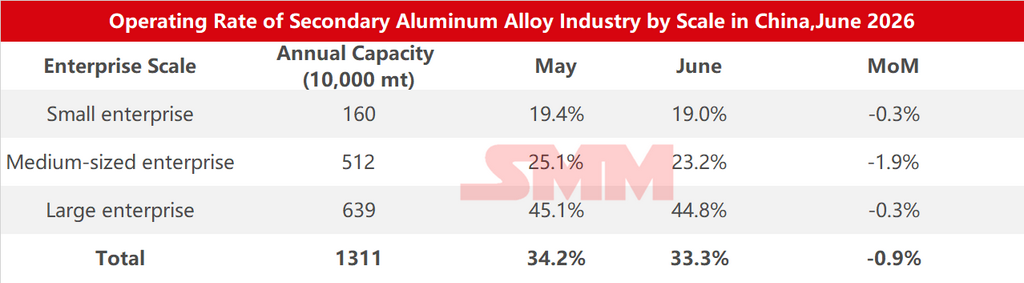

According to an SMM survey, the operating rate of the secondary aluminum industry in June 2026 fell 0.9 percentage points MoM from May to 33.3%, a decline of 7.6 percentage points YoY.

The industry operating rate continued its downward trend in June, dropping to the lowest level of the year excluding the impact of Chinese New Year, weighed down by both tight raw material supply and weak end-use demand.

Raw material side, since the start of June, regulatory oversight of the "ticket economy" has not eased, with coverage continuing to expand. Many regions suspended reverse invoicing, further intensifying input invoice shortages and significantly pushing up corporate tax and compliance costs, adding to operational pressures. Meanwhile, SHFE aluminum prices accelerated their decline in late June. Although this drove marginal softening in aluminum scrap prices, scrap prices overall remained resistant to decline, with limited price adjustments, squeezing suppliers' profit margins further and increasing their sentiment to hold back from selling. Against the backdrop of simultaneous invoice and material shortages, raw material procurement remained difficult, continuing to constrain production release.

Demand side, the traditional consumption off-season became more pronounced in June. Automotive production and sales slowed down, weighing on order performance at die-casting enterprises, and secondary aluminum demand remained under pressure. Demand in sectors such as motorcycles was relatively stable, and some export orders saw slight growth thanks to an improved price spread between Chinese and overseas markets, but the increment was limited. Overall orders remained in contraction, with enterprises lacking momentum for new production, and operating rates continued to be under pressure.

However, as production had already contracted significantly in May, the room for further production cuts in June was limited, so the MoM decline in the operating rate narrowed compared with the previous month. On a YoY basis, the decline widened notably, mainly because in the same period last year, the listing of cast aluminum alloy futures prompted trading firms engaging in both spot and futures markets to actively participate in procurement, concentrating restocking during the off-season, which boosted production enthusiasm among secondary aluminum producers and created a high base for the comparison period.

Looking ahead to July, the industry is still expected to face constraints such as the continuation of the demand off-season and tighter invoice regulation, but after two consecutive months of production cuts, the room for further output compression is already quite limited. At the same time, the price spread between A00 primary aluminum and ADC12 has continued to widen recently, and some enterprises have started to increase primary aluminum procurement to alleviate difficulties in scrap aluminum procurement and invoice shortages, ensuring normal production. Although the overall scale of substituting primary aluminum for scrap is expected to remain limited, it is likely to improve the raw material supply situation to some extent, providing marginal support for industry operating rates. The secondary aluminum industry operating rate may see a slight rebound in July.

![In June, the operating rate of secondary aluminum producers saw a narrowing MoM decline and a deep YoY pullback, with attention to production elasticity driven by price spreads [SMM Analysis]](https://imgqn.smm.cn/usercenter/risnW20251217171650.jpg)