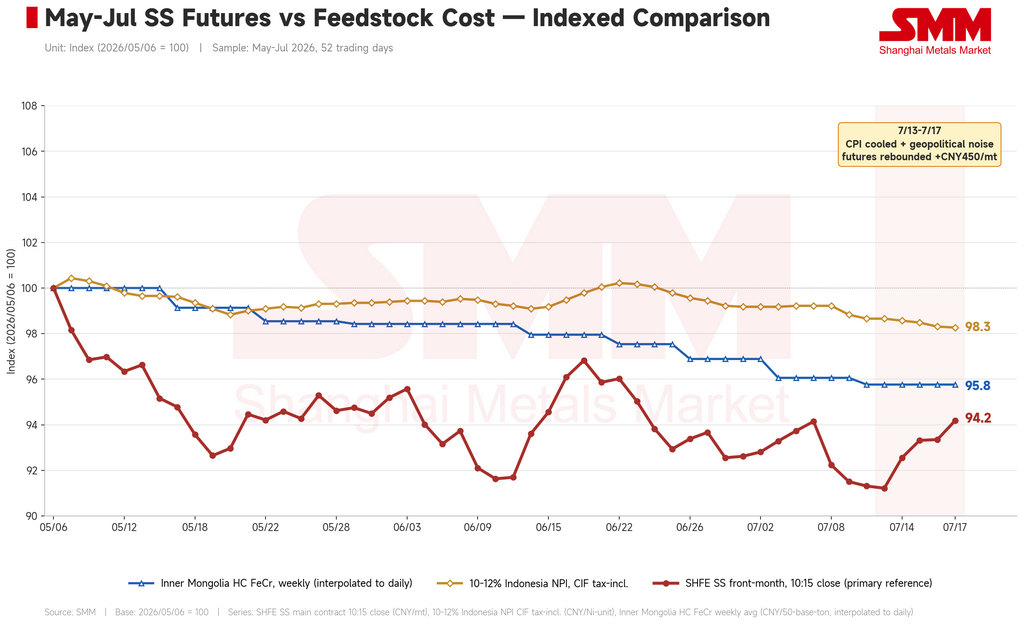

This week (July 13–17), China's stainless steel futures rebounded from their decline, driven by a dual tailwind: US June CPI data came in softer than expected, cooling inflation expectations and lifting market risk appetite, while limited growth in Indonesian nickel ore supply kept a raw-material shortage in place, supporting the cost side. The benchmark contract closed Friday, July 17 at RMB 14,795/mt (approx. $2,185/mt), up RMB 450/mt — around 3.1% — from RMB 14,345/mt (approx. $2,119/mt) the previous Friday. The week's defining feature remained the gap between futures and spot: futures rallied sharply on the back of improved macro sentiment, while spot prices, though also firmer, rose far less than the futures contract.

On the macro and news front, sentiment both at home and abroad broadly improved, though geopolitical disruption remained a wildcard. Overseas, US June CPI slowed to 3.5% year-on-year and fell 0.4% month-on-month — the first such monthly decline in six years — while PPI dropped 0.3% month-on-month, its first decline since last year, and core PPI slowed to 4.7% year-on-year. The across-the-board cooling in inflation data revived rate-cut expectations and lifted risk appetite. Fed officials, however, remained cautious in their public remarks: Governors Kevin Warsh and Lisa Cook, along with New York Fed President John Williams, all stressed the need to bring inflation sustainably back to the 2% target, offering no clear signal of imminent easing. At the same time, Middle East tensions repeatedly disrupted market sentiment — Iran briefly announced the closure of the Strait of Hormuz, the US responded by blockading Iranian ports and proposing a 20% transit fee, and tensions then eased again — creating a tug-of-war over oil prices and broader commodity cost expectations. Domestically, China's economy showed resilience even as growth cooled: GDP grew 4.3% year-on-year in the second quarter and 4.7% for the first half, while nationwide power demand repeatedly hit record highs, providing some support to overall sentiment.

On fundamentals, destocking continued and spot demand showed some resilience. SMM-tracked 300-series stainless steel social inventory stood at 591,000 mt this week, down 18,000 mt from 609,000 mt the previous week — a meaningful drawdown even in the traditional off-season, easing near-term pressure from inventory buildup. Spot prices held up for three main reasons: first, limited supply arrivals — mills held firm on pricing, and this week's typhoon disrupted logistics, slowing the pace at which fresh material reached the market; second, improved trading sentiment — the futures rally spurred buy-the-dip behavior, and end users released some restocking demand, visibly improving the trading atmosphere from recent weeks; third, persistent end-user caution — the market remains in the traditional seasonal lull, underlying demand is generally weak, and buyers showed limited appetite for higher-priced material after the rally, with a wait-and-see mood still constraining spot's upside relative to futures.

On costs and supply, raw material prices continued to soften, further improving mill profitability. Indonesian nickel pig iron (10–12% grade — a low-grade ferro-nickel alloy used in stainless steel production) priced at RMB 1,132.5 per nickel point (approx. $167/point) this week, down slightly from RMB 1,137 (approx. $168/point), as mills continued pressing for lower purchase prices. High-carbon ferrochrome from Inner Mongolia was quoted at RMB 8,100 per 50-mt basis ton (approx. $1,197) in its latest reading, down RMB 25 from the prior RMB 8,125 (approx. $1,200), with the cost base for raw materials steadily trending lower. Finished-product prices, by contrast, trended higher on mill price support and improving transactions, widening the spread between finished goods and raw materials. That directly boosted stainless steel smelting margins, further strengthening industry-wide profitability, easing pressure on production-side earnings, and providing some support for current output schedules — with no signs yet of supply contracting.

Overall, China's stainless steel futures stabilized and rebounded this week on the combined strength of improved macro sentiment and spot destocking, but the futures-spot divergence has not narrowed — futures gains clearly outpaced spot, with spot restrained by weak end-user acceptance during the off-season. Looking ahead, Middle East geopolitics remains the key uncertainty; further escalation could disrupt the futures market through cost-side effects and shifts in risk appetite. On the industry side, the key questions are whether off-season destocking can continue, and whether mills' willingness to hold prices firm is sustainable against a backdrop of weak demand. SMM expects the benchmark contract to hold a moderately firm, range-bound tone in the near term, with the futures-spot divergence persisting. Industry clients are advised to view macro-driven futures volatility with a level head, closely track the actual durability of off-season spot destocking and shifts in end-user buying appetite, and maintain a steady, risk-managed approach to operations.