7.16

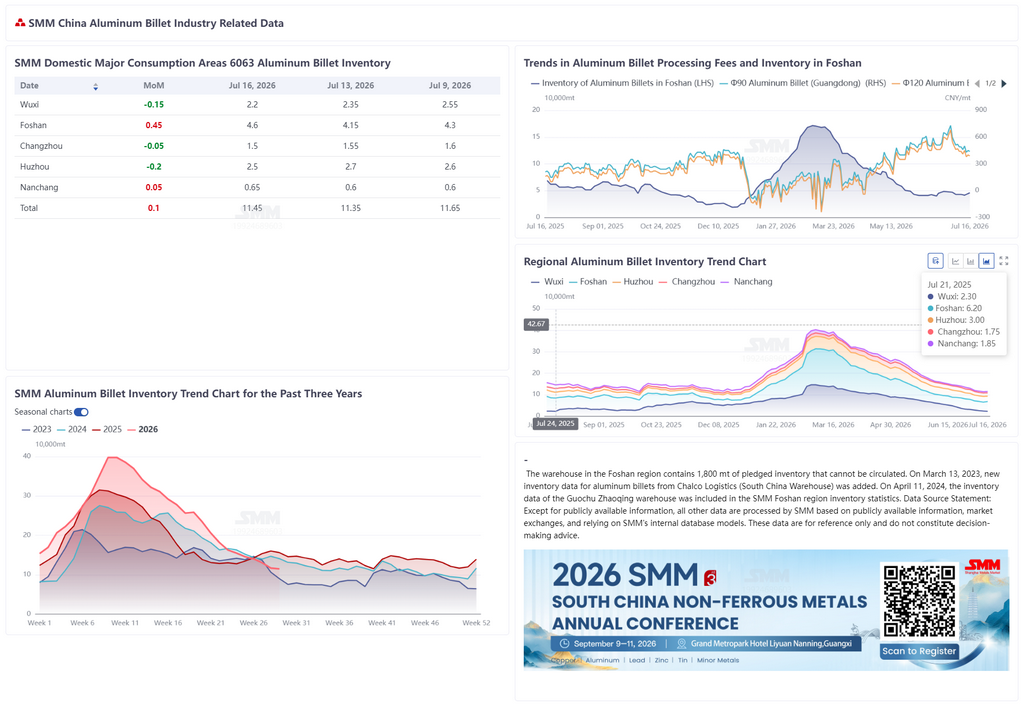

According to SMM data, on July 16, aluminum billet inventory in major Chinese consumption areas stood at 114,500 mt, a slight WoW build of 1,000 mt from last Monday but a decrease of 2,000 mt from last Thursday. This marks the first WoW inventory buildup this year, though the increase was relatively small. Compared to the same period in previous years, inventory was 41,500 mt lower than in 2025, 26,200 mt lower than in 2024, but 24,800 mt higher than in 2023. Total inventory remained at relatively low levels for this time of year over the past four years. Regarding warehouse withdrawals, aluminum billet withdrawals during July 7–13 reached 42,100 mt, down 6,400 mt WoW. Withdrawal volumes stayed high but pulled back somewhat. Currently, aluminum billet inventory showed regional divergence: Foshan saw an inventory buildup of 4,500 mt, the main driver of the overall inventory rebound, mainly due to concentrated arrivals after previously low arrivals; Wuxi, Changzhou, and Huzhou regions continued destocking, with Wuxi destocking 1,500 mt and Huzhou destocking 2,000 mt, pushing inventories even lower; Nanchang recorded a slight inventory buildup of 500 mt. Overall, inventory has fallen to historically low levels for this period, leaving limited room for further destocking. Next week, aluminum billet inventory is expected to consolidate around 110,000 mt in a narrow range. Future attention should be paid to Foshan's absorption of arrivals and changes in material flows across regions.

Aluminum price center continued to shift higher this week. The SMM A00 spot aluminum price rose from 22,950 yuan/mt last Thursday to 23,170 yuan/mt, a cumulative increase of about 220 yuan/mt. Against the backdrop of rising aluminum prices, processing fees diverged by region, and Wuxi showed a price-firming trend. By region, in Foshan, processing fees for φ90 aluminum billet were quoted at 440 yuan/mt and φ120 at 390 yuan/mt, each down 50 yuan/mt from last Thursday. In Wuxi, φ90 and φ120 billet processing fees were 620 yuan/mt and 520 yuan/mt, respectively, up 80 yuan/mt from last Thursday, with clear price-firming sentiment. In Nanchang, φ90 and φ120 fees stood at 460 yuan/mt and 410 yuan/mt, each down 140 yuan/mt from last Thursday. Wuxi’s processing fees bucked the trend to rise this week, mainly due to tight supply in circulation. Some aluminum billet producers reported that active shipments in the market were relatively tight, and some producers diverted supply to Guangdong, resulting in low arrivals in Wuxi, which fueled significant price-firming sentiment. In Foshan, processing fees pulled back under pressure from increased arrivals recently, while Nanchang followed the broader decline. Next week, processing fees are expected to remain divergent across regions. Supported by tight supply, Wuxi’s fees are likely to stay high, while Foshan and Nanchang still have room to ease under arrival pressure. Attention should be paid to the pace of material flows between regions and the transmission of aluminum price trends to processing fees.

![[SMM Analysis] The Southeast Asian secondary aluminum market remains in the doldrums, while the import window has improved but transactions are yet to recover.](https://imgqn.smm.cn/usercenter/iCOMR20251217171653.jpg)