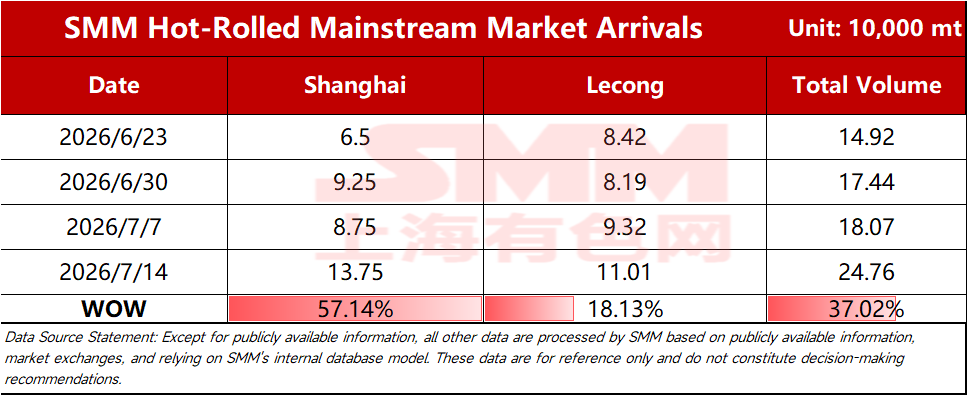

SMM Steel, July 14 – According to SMM statistics, this week, total estimated shipments of mainstream market resources reached 247,600 mt, up 37.02% WoW. By market:

Table 1: Arrivals Comparison by Mainstream Market

Data source: SMM Steel

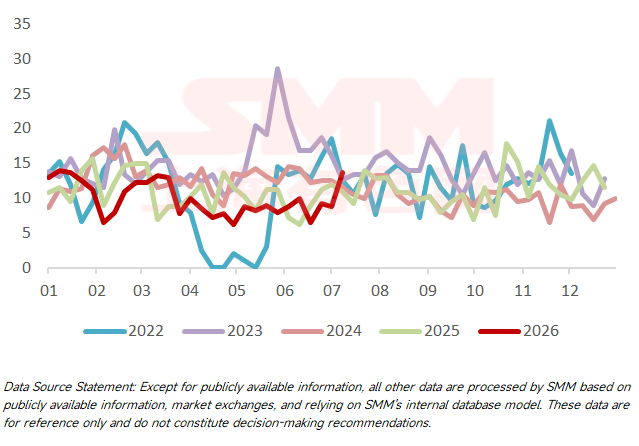

Shanghai Market: This week, HRC shipments in the Shanghai market increased from last week. Specifically, shipment volumes from the Northeast market declined, possibly affected to some extent by recent typhoon weather; shipment levels from the South China market were low earlier, but rose markedly this week. Under the combined influence, HRC shipments rebounded WoW. Looking ahead, as the impact of the typhoon gradually eases, shipments from some northern markets are expected to increase.

Chart-1: Shanghai Market Arrivals

Data source: SMM Steel

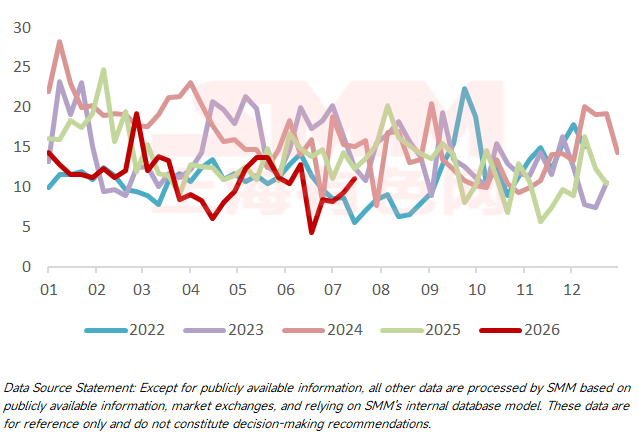

Lecong Market: This week, shipments to Lecong increased. Specifically, North China resources remained stable, while both major mainstream sources posted WoW gains, driving overall arrivals further upward. Looking ahead, as the typhoon impact in South China gradually fades and no new maintenance emerges for the two major mainstream sources, arrivals are expected to continue growing in the short term.

Chart-2: Lecong Market Arrivals

Data source: SMM Steel

SMM releases mainstream market HRC shipment data every Tuesday. For subscriptions or more data, please scan the QR code below.