Q1: Geopolitical and Macro Tug-of-War, Destocking and Stockpiling Consolidate at Lows

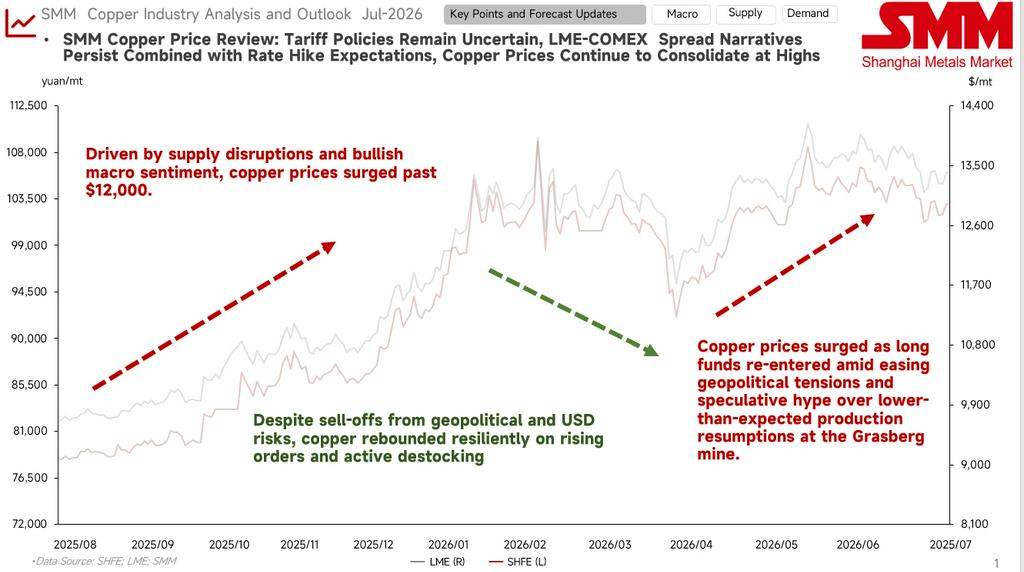

Macro shocks and retreat after rapid rise: At the start of the year, capital inflows drove futures to briefly break through the 110,000 yuan/mt mark. Warsh was subsequently nominated as Fed Chairman, and expectations for a strong US dollar quickly pushed copper prices to retreat under pressure.

Fundamentals provided support and stabilization at lows: At quarter-end, the US dollar index weakened from highs, and with the launch of China’s stockpiling spree and social inventory of copper cathode entering a rapid destocking phase, spot buying effectively supported prices.

Q2: Supply Disruptions Drive Upward, Tariff Expectations Set the Tone for Consolidation at Highs

Ore supply tightness and momentum-driven breakthrough: In April, destocking logic persisted and futures held steadily above the 100,000 yuan/mt mark. In May, production resumptions at the Grasberg mine fell short of expectations, reigniting the narrative of ore supply contraction and driving a rapid rise in copper prices.

LC arbitrage and long-short stalemate: In June, with US copper tariff policy still up in the air, market pricing in advance caused the LC spread (COMEX-LME) to widen significantly. Cross-market arbitrage funds and expectations for restocking in the US market provided downside support for futures. However, as expectations for US Fed interest rate hikes later in the year heated up, coupled with China entering the traditional consumption off-season, sharp upward resistance emerged, and prices settled at 103,000 yuan/mt.

The current tug-of-war between longs and shorts in the copper market is intense, with an overall pattern of "support from below, resistance from above."

Bullish factors: Cooling US nonfarm payrolls has marginally eased macro pressure; doubts about mine production resumptions and early restocking triggered by tariff uncertainty have built a solid bottom for copper prices.

Bearish factors: Sticky inflation causes expectations for rate hikes to recur; as July enters the consumption off-season, high prices severely dampen downstream demand in traditional sectors, limiting upside momentum.

Based on fundamental data, are H2 copper prices "more likely to rise than fall"?

Ore supply disruptions are more likely than new additions.

↓

Global copper cathode production continues to increase, with high expansion demand in China.

↓

Copper demand growth in emerging sectors provides support, and traditional consumption takes over when copper prices are low.

↓

Copper scrap remains overall influenced by policies, with selling sentiment depending on copper prices.

Mine disruptions are frequent, and currently TC/RCs continue to weaken, repeatedly hitting new historical lows; year-end negotiations without a fixed Benchmark have left the market unable to maintain an optimistic outlook on the ore supply situation.

In 2025, global copper cathode production distribution continued to concentrate in China. Smelting capacity further concentrated in a few regions, increasing industry concentration. Comparing annual averages, the dispersion in 2026 is already lower than the three-year average for 2022–2025. In terms of production changes, China's new production release in 2026 is expected to contribute 704 kt of growth, far exceeding other countries; while Japan, South Korea, Chile, and others show negative growth, partly due to technological transformation of aging facilities or raw material supply constraints. The DRC region maintains a relatively high growth rate, with an expected incremental production of 221 kt. Looking ahead, copper smelting profit in Q3 will maintain a hedging pattern of “strong sulphuric acid support, deeply negative TC,” with overall smelting profit remaining positive but already in the top range of this cycle. If high sulphuric acid prices persist into the peak season, the profit window may be extended longer than expected; however, once supply recovers and demand turns weak, the copper smelting loss pressure previously masked by high acid prices will re-emerge, and the risk of industry chain transmission warrants high vigilance.

Supply side, the main contradiction still lies on the ore side. Demand side, global demand continues to be driven by growth in emerging sectors; copper still has momentum to move higher amid the AI and other technology narratives, but this needs to be accompanied by macro sentiment.

Looking ahead to H2, macro attention should be on the US Fed’s subsequent interest rate hike moves and the pending results of the Section 232 tariff survey. The subsequent trend of high COMEX inventory and the year-end global annual long-term contract negotiations for ore and copper cathode will also be a focus. Fundamentals side, currently downstream acceptance at 103,000 yuan/mt is moderate, but when approaching the 100,000 level, end-user ordering sentiment is high, and the 100,000 level shows strong resistance to declines.