Price Trends

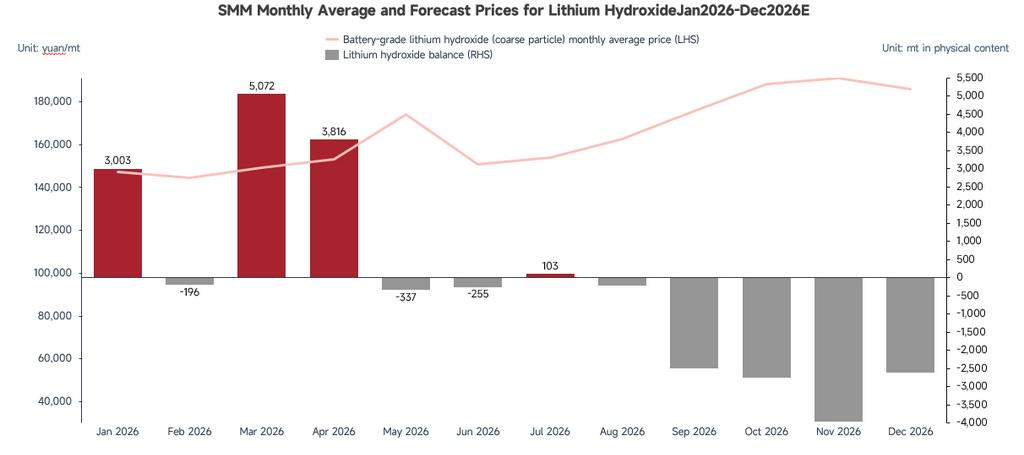

In the first half of 2026, domestic lithium hydroxide prices followed a trajectory of "surge – high-level volatility – softening decline," with the price center first rising and then falling amid the interplay of multiple factors.

January: Prices surged sharply. Concentrated maintenance shutdowns at major lithium salt producers tightened spot supply. Combined with persistently rising costs of lithium carbonate and lithium ore, lithium salt producers held firm on pricing, pushing the monthly average price up by 65% month-on-month. Although ternary material manufacturers maintained just-in-time procurement and remained cautious on spot orders, and some import flows returned due to domestic-international price spreads, the phase of supply shortages and cost support still drove prices to a high level.

February: Prices fluctuated at high levels with thinning trading. Macro sentiment drove overall lithium prices downward, but producers' firm pricing stance persisted. Downstream ternary manufacturers, having ample inventories and some entering maintenance, saw eased raw material shortages, with procurement mostly based on monthly average prices. During the Chinese New Year holiday, transportation of lithium hydroxide, classified as hazardous chemicals, stalled, leading to a seasonal quiet period; post-holiday restocking demand was tepid, limiting upside momentum, and prices oscillated widely throughout the month.

March: Gains narrowed notably. Cell manufacturers' offtake fell short of expectations, and new orders for ternary materials were limited. Additionally, increased customer-supplied materials in mid-month sharply reduced spot demand, leading to subdued trading and an upward price channel that stalled. The monthly average price rose only 3.4% month-on-month.

April: First down then up. In the first half, limited new ternary orders and scarce spot demand put mild pressure on prices; in the second half, pre-holiday stocking and new orders drove increased inquiries from ternary producers, while sharp rises in lithium carbonate and ore prices pulled lithium hydroxide higher. The monthly average price rose 2.73% month-on-month.

May: Rose then fell. In the first half, positive demand expectations and supply-side disruptions lifted lithium carbonate and ore prices, pulling lithium hydroxide higher in tandem; in the second half, sentiment turned weaker, with more trades settled via negotiation between traders and material mills. As ternary demand trends became clearer, upstream producers softened their price support, prompting a modest pullback. The monthly average price reached RMB 174,000/ton, up 13.6% month-on-month.

June: Prices fell notably, with range-bound volatility intensifying. Frequent supply disruptions on the lithium resource side amplified market volatility significantly, prompting holders to adopt a cautious stance and quote prices in line with market conditions. Upstream producers adjusted prices flexibly, while traders maintained a high discount (over RMB 15,000/ton against the lithium carbonate futures main contract). On the demand side, total ternary material demand remained weak month-on-month, but within the RMB 135,000–145,000/ton range, downstream buyers showed strong willingness to stockpile on dips, providing some bottom support and exacerbating range-bound fluctuations. The monthly average price fell 11.52% month-on-month.

Looking at the price trends, the correlation between lithium hydroxide prices and lithium carbonate futures prices has strengthened over the past six months. This is partly because upstream producers use a "lithium carbonate price × discount factor" formula as a floor price in their pricing. On the other hand, traders capitalize on the price spreads between domestic and overseas lithium hydroxide and between hydroxide and carbonate, by importing lithium hydroxide and pricing their sales with reference to lithium carbonate futures, further reinforcing this price linkage.

Production

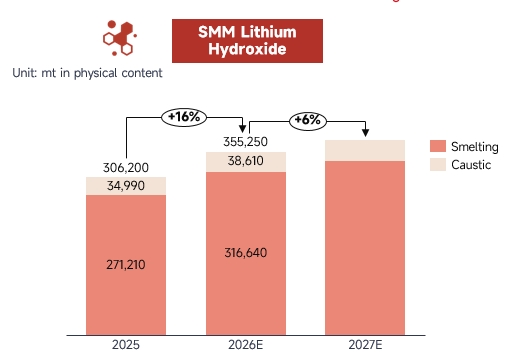

In the first half of 2026, domestic total lithium hydroxide output reached 172,000 tons, up 21% year-on-year, driven by relatively robust downstream demand, with notable incremental growth. By output structure, the refining segment contributed the most, accounting for about 88%. Within this, the gradual ramp-up of new production lines at leading companies added some volume, while other enterprises maintained steady output backed by downstream orders, resulting in an 18% year-on-year increase for the overall refining segment. For the causticization segment, most active producers sustained stable operations, and the industry CR5 reached 72% in the first half, indicating a persistently high market concentration.

From the capacity utilization perspective, although some capacity has been switched to lithium carbonate production, the operating rate for the lithium hydroxide industry has consistently lingered below 50% over the past six months, reflecting an ongoing overcapacity trend.

Costs and margins: For the refining segment, lithium ore feedstock remained relatively tight in the first half of 2026, with ore prices staying elevated and closely correlated with lithium carbonate prices, providing strong cost support for lithium hydroxide. As a result, non‑integrated producers faced notable pressure on the sales side, and their product discount prices did not decline further, which in turn provided marginal support for profit margins at current price levels. For the causticization segment, the supply of salt‑lake‑based lithium salts has increased over the past six months, making causticization feedstock relatively ample. The linkage between actual procurement costs and industrial‑grade carbonate quotes has weakened, which has alleviated cost pressures for enterprises that purchase lithium carbonate externally, leading to actual profitability in the causticization segment being better than theoretical estimates.

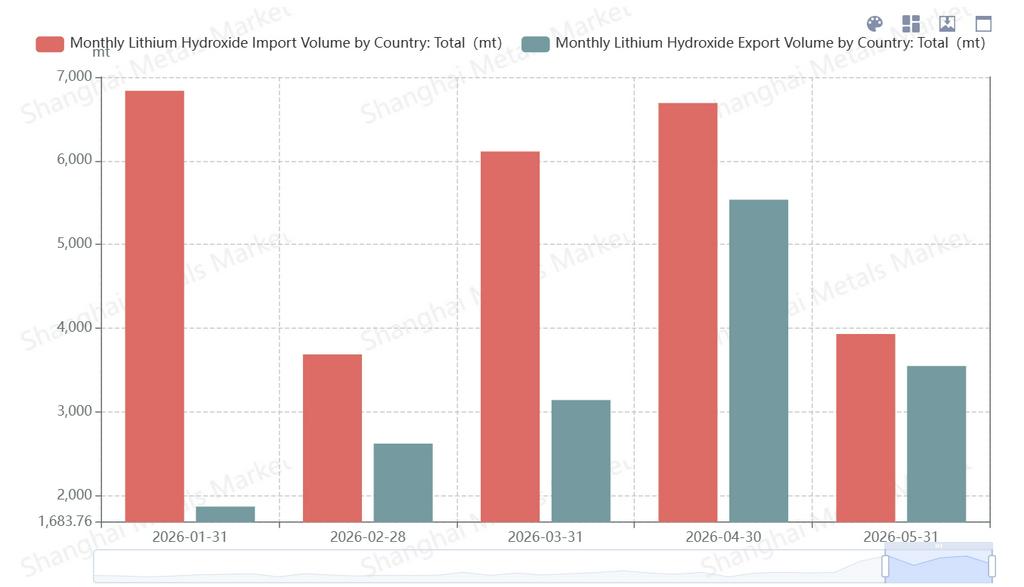

Import and Export

The import‑export landscape has seen a notable reversal. On the export front, since the second half of 2025, some overseas ternary material producers have shifted to entrusting domestic tolling processors, resulting in products that would have been exported being delivered domestically instead, effectively suppressing export volumes. At the same time, overseas demand for ternary materials has remained persistently weak, reducing foreign buyers' appetite for Chinese lithium hydroxide. This, combined with the gradual ramp‑up of overseas local production lines, has collectively kept export volumes at low levels over the past six months. On the import side, weak overseas demand, high accumulated inventories, and arbitrage opportunities have driven import volumes to remain relatively elevated, further reinforcing the net import trend.

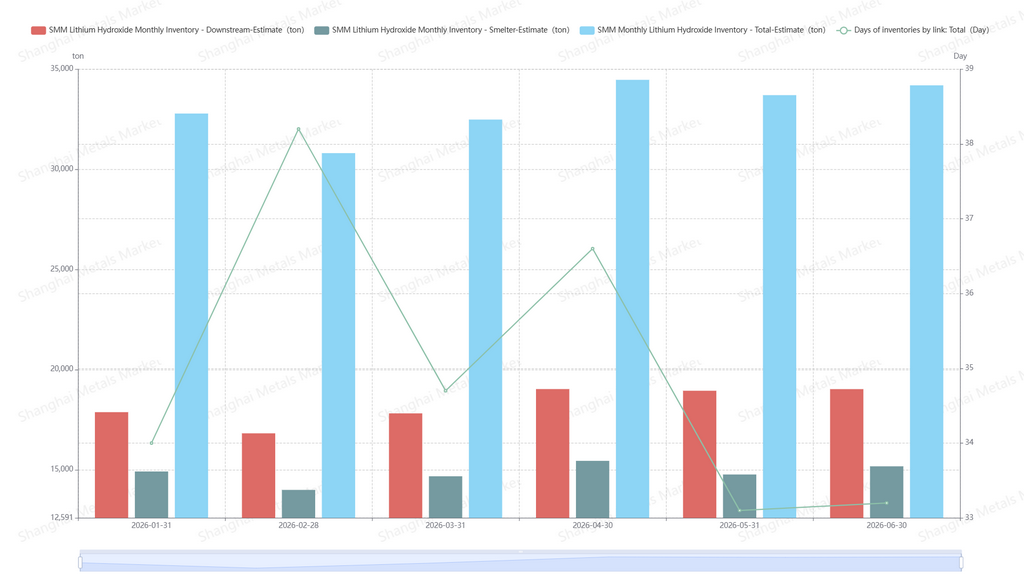

Supply‑Demand Balance and Inventory

The surge in import data made most months in the first half of the year oversupplied. However, from the perspective of directly usable lithium hydroxide products, the market as a whole remained in a relatively tight balance, providing effective support for upstream price control.

As for inventory, current lithium hydroxide stock levels have improved significantly compared with the same period last year. This is mainly attributable to two factors: first, part of the inventory has been absorbed into the market by being converted into lithium carbonate; second, active producers have flexibly adjusted their output pace, keeping current inventory days at around one month.

Future Outlook

Looking ahead, although the LFP route continues to squeeze the ternary route, ternary materials currently have no rival in the high‑nickel segment. In addition, the cost advantages of 6‑series materials offer more possibilities for the ternary route. Based on end‑user production schedules, ternary power demand in the second half of 2026 is expected to maintain a sound performance, growing by approximately 36% compared with the first half. This will drive a roughly 7% sequential increase in ternary material output in the second half. As ternary materials continue to move toward higher nickel content, this brings an incremental demand trend for lithium hydroxide. Meanwhile, considering that most lithium hydroxide production lines have flexible switching or carbonation purification capabilities, lithium hydroxide output is projected to grow by about 6% sequentially. Coupled with a modest recovery in overseas ternary demand, the supply‑demand balance for lithium hydroxide is expected to remain tight through 2026–2027.

In terms of price, under a market structure with highly concentrated supply, lithium hydroxide prices are primarily determined by the supply‑demand dynamics of its own industrial chain and closely track lithium ore and lithium salt price trends. Prices are currently oscillating in a range above RMB 150,000/ton.

Futures Developments

As for lithium hydroxide futures, there has been a flurry of related developments in the second quarter.

The Guangzhou Futures Exchange (GFEX) and the Lithium Branch of the China Nonferrous Metals Industry Association have both explicitly stated that they will continue to strengthen cooperation and jointly advance the listing of lithium hydroxide and other lithium‑chain futures products. The征求意见稿 of Guangzhou's "15th Five‑Year Plan" for finance also clearly supports GFEX in listing new‑energy futures such as lithium hydroxide.

On the industrial side, companies have moved swiftly to follow up. In June, Yahua Group, Shengxin Lithium Energy, and Tianqi Lithium all announced their intention to apply to GFEX for designated delivery factory warehouse status for lithium hydroxide. In addition, Milkyway's shareholders' meeting approved a proposal for its subsidiary to apply to become a designated delivery warehouse for battery‑grade lithium hydroxide at GFEX. According to media reports, lithium salt producers (Ganfeng Lithium, Tianqi Lithium, Yahua Group, etc.) have already positioned themselves in the factory‑warehouse system. However, due to the high‑risk storage requirements of lithium hydroxide—such as strong corrosiveness, exothermic reaction with water, and the need for inert gas protection—no logistics‑focused player had previously entered this category.

On the market front, some traders have already made early arrangements in anticipation of futures listing, and the number of merchants participating in lithium hydroxide import trade has noticeably increased.

In summary, preparations for the listing of lithium hydroxide futures are progressing in an orderly manner, with positive official signals and accelerating industrial infrastructure development.

![H1 Refined Cobalt Price Surged over 97% YoY; Demand Remains the Current Focus; What Can the Market Expect Going Forward? [Weekly Observation]](https://imgqn.smm.cn/usercenter/oVqJl20251217171730.jpg)

![[SMM Analysis] Riding the Winds In and Outside China, Breaking the Iron Law of Old Cycles: 2026 Energy Storage Battery Cell Semi-Annual Review and Outlook](https://imgqn.smm.cn/usercenter/WBREf20251217171728.png)