SMM, July 10:

In H1 2026, the secondary copper rod market completely detached from the traditional “copper price–supply-demand” pricing framework, primarily impacted by the dual policy shocks of the transition of reverse invoicing from transitional audits to full implementation and the clearance of illegal local fiscal award and subsidy programs (Document No. 770), coupled with the wide fluctuations of the most-traded SHFE copper contract, which retreated from the historical high of 113,800 yuan/mt at the beginning of the year and persistently held the 100,000 yuan/mt mark in mid-year. The entire industry was mired in a deep stalemate characterized by “policies defining structure, invoices locking in transactions, and copper prices setting the pace.” Operating rates plummeted YoY, and enterprises generally walked a tightrope between compliance pressures and weak demand.

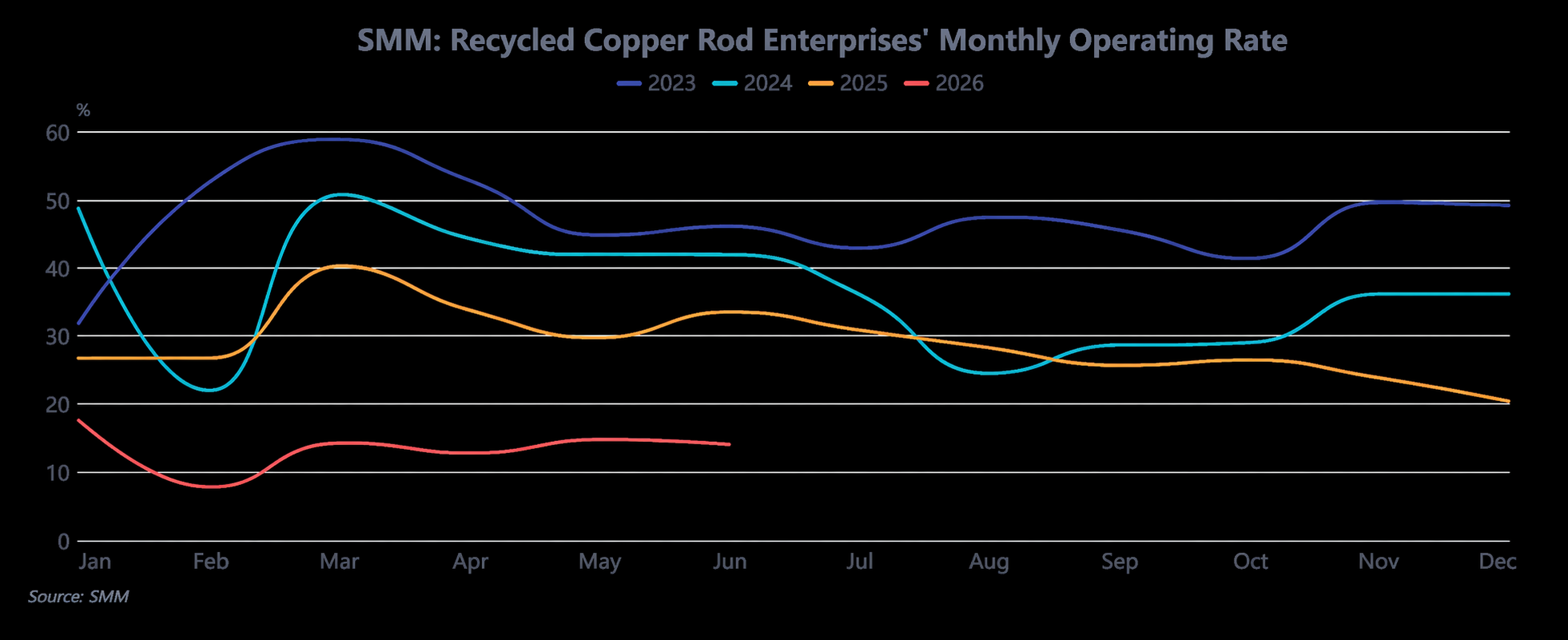

The core contradiction on the supply side was never a shortage in the total volume of copper scrap, but a scarcity of compliant supply that could be properly invoiced and guaranteed stable collection—this was the fundamental variable that suppressed supply in H1. At the beginning of the year, when reverse invoicing was first implemented, local tax audits tightened, forcing enterprises to abandon previously non-compliant low-price sources and fully shift to purchasing domestically produced tax-included or imported copper scrap with higher invoice tax rates. The invoice tax rate surged from 9.1%-9.3% at the start of the year to above 10.5% in March, leading to a rigid increase in the cost of tax-inclusive raw materials and even causing cost inversions where “tax-included copper scrap price > spot copper cathode price.” This directly set a hard floor on the cost of secondary copper rod, meaning that even when copper prices pulled back, raw material prices did not decline in tandem. In Q2, regions in south China such as Jiangxi, Hubei, and Shuyang in Jiangsu successively advanced compliance inspections for reverse invoicing and imposed limits on invoicing quotas, resulting in a large number of small and medium-sized rod producers halting production due to insufficient invoices, further tightening compliant supply. Regional divergence became pronounced: in south China, due to slower capital turnover and higher compliance costs, purchase prices for bare bright copper were 400-600 yuan/mt lower than in north China. The unusual structure of different prices for the same material essentially reflected regional differences in compliance costs, rather than supply-demand disparities. Meanwhile, the payment collection cycle was extended from the original 3-5 days to over two weeks, tying up traders' capital severely, making them unwilling to stockpile and bet on price rises, and widely switching to a strategy of “quick turnover to preserve cash flow.” Some even adopted a model of “raw material consignment plus installment settlement” with rod producers, further driving up the actual circulation cost of raw materials. Constrained by these factors, the average operating rate of secondary copper rod producers in H1 was only about 13.8%, down 18 percentage points from the same period of 2025. After the Chinese New Year, the weekly operating rate dropped to as low as 2.15%, and even in March, traditionally a peak season, it only rebounded to 14.25%. Capacity remained constrained and could not be released. Some enterprises, finding their long-term copper anode contracts stable and at a discount to futures, chose to maintain anode production capacity, further compressing the supply elasticity of secondary copper rod.

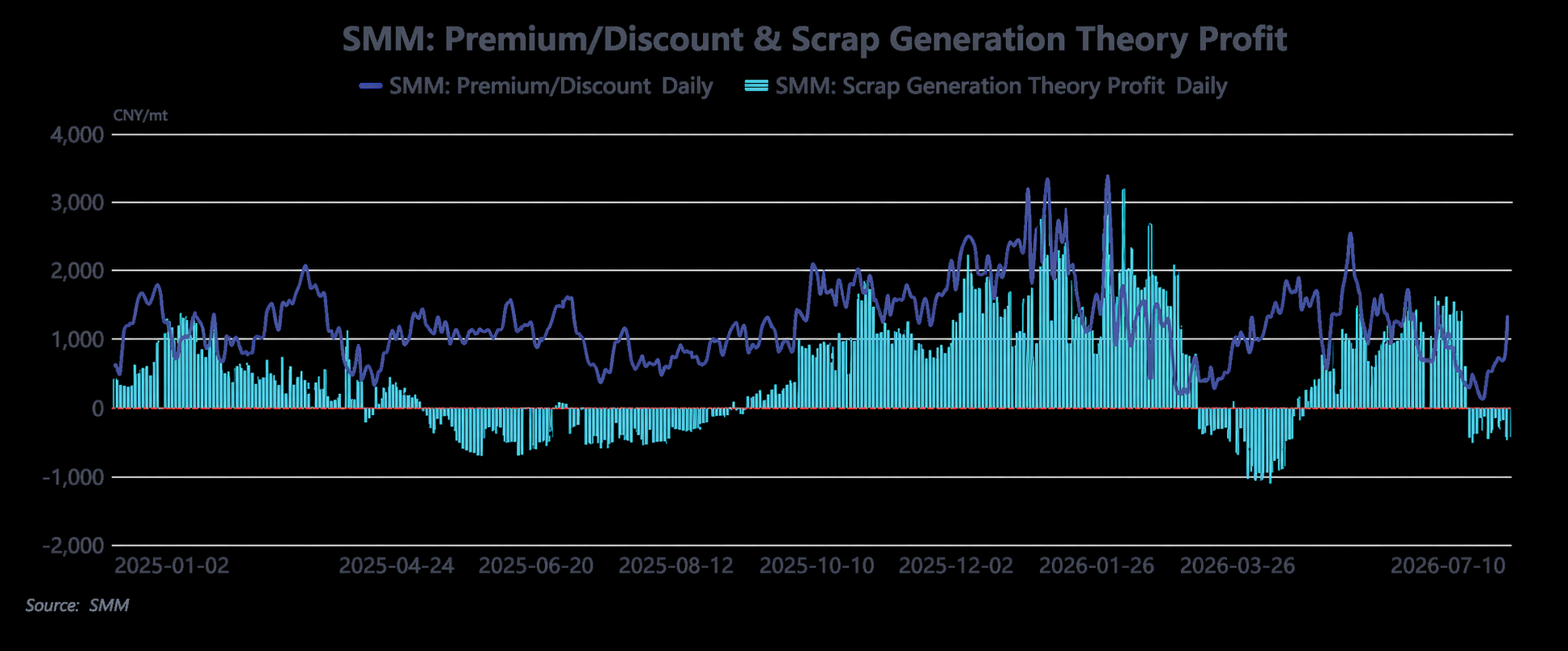

On the demand side, the market was shackled by triple constraints of “high copper prices suppression + unstable price spreads + reverse invoicing constraints,” and remained devoid of endogenous growth momentum. In H1, absolute copper prices persistently stayed above the high level of 100,000 yuan/mt. Orders from end-user sectors such as wire and cable, real estate, and infrastructure were already weak, and businesses widely adopted a "demand postponement" strategy, waiting for copper prices to correct. Particularly in Q2, as copper prices repeatedly tested the 100,000 yuan/mt level, end-users formed a consensus expectation of "procure only after it breaks below 100,000," with purchasing limited to rigid pulse demand. Traditional stockpiling for Chinese New Year and the Dragon Boat Festival completely failed to materialize. The price difference between copper cathode rod and secondary copper rod fluctuated wildly in H1, collapsing from a historical high of 6,000 yuan/mt in January to negative territory in March. In Q2, it mostly fluctuated within a range of 300–1,500 yuan/mt, consistently failing to stay above the 1,500 yuan/mt threshold of economic viability for secondary copper rod. Moreover, due to rigid raw material costs, secondary copper rod frequently commanded a premium to copper futures, leading end-users to prefer purchasing copper cathode rod or shaft furnace rod, further squeezing the demand space for secondary copper rod. Meanwhile, the demand side was also constrained by invoice issues: downstream procurement required matching compliant input invoices. Even if secondary copper rod prices were lower, transactions were difficult to conclude if suppliers could not issue invoices, further reducing effective demand. Throughout H1, secondary copper rod transactions were largely triggered by copper price fluctuations, with no sustained volume. Enterprise gross profit remained around 1,000 yuan/mt with spread fluctuations, but stability was extremely poor. Most of the time, companies relied on drawing down prior inventory or spread arbitrage to sustain operations, leaving them with very weak risk resilience.

Overall, the core logic of the secondary copper rod market in H1 has shifted from the traditional "price versus supply-demand" game to a structural game of "compliance costs – invoice settlement – end-user orders." The essence of the "copper shortage" is a "shortage of copper that can be settled in compliance." Looking ahead to H2, the key to breaking the market impasse lies in two variables: First, whether the implementation details of reverse invoicing can be further clarified. If invoicing quotas are relaxed and procedures simplified, the tightness in compliant cargo availability may ease. Second, whether copper prices can break below the 100,000 yuan/mt level, unleashing pent-up end-user demand, coupled with a substantive recovery in orders from power grid and infrastructure sectors. If the economic viability of secondary copper rod stabilizes and recovers, transactions are expected to improve marginally. If neither variable sees positive progress, the stalemate of weak supply and demand will persist, and the industry may continue to operate within the triangle of "production needs – invoice constraints – payment term control."