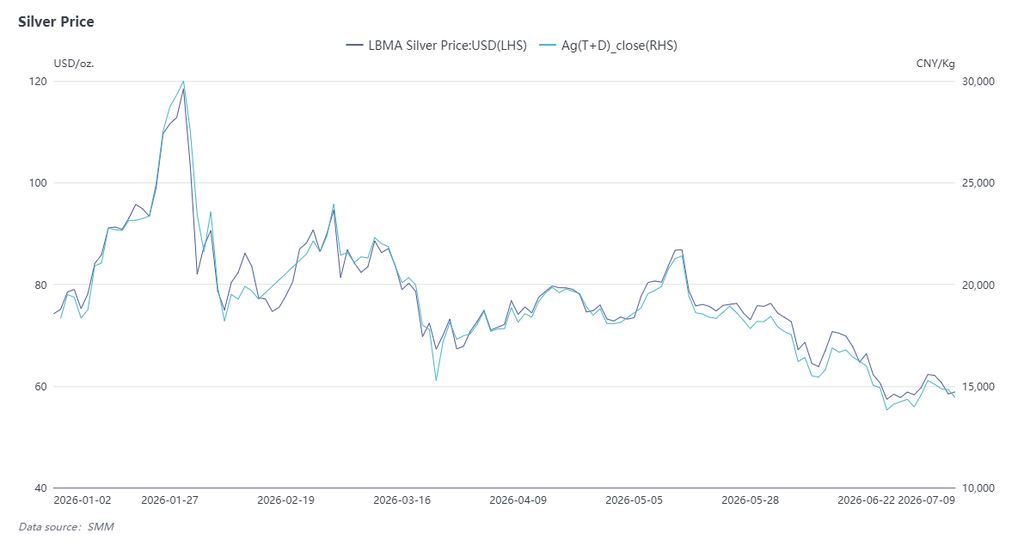

H1 2026 Silver Price Review: An Extreme Surge Followed by a Trend Pullback

In H1 2026, silver experienced extreme price action — a “pointed-top inverted V” followed by a stepwise decline — driven by the interplay of two key themes: a dislocation in spot market fundamentals and a shift in US Federal Reserve monetary policy. Early in the year, a squeeze in the spot market intensified, and accommodative expectations provided valuation support, together pushing silver to an all-time high of 30,900 yuan/kg. Subsequently, rate-cut expectations went from fully priced in to a complete reversal, and persistently above-forecast inflation reinforced tightening expectations, sending silver into a downward trajectory. In June, it hit a half-year low of 13,816 yuan/kg, a pullback of 55% from the peak.

In January and February, squeeze sentiment dominated the spike, with accommodative expectations providing a macro valuation floor. At the start of the year, the market continued to trade on the earlier loose-policy narrative, broadly expecting the Fed to begin cutting interest rates within 2026, while a temporarily weaker US dollar underpinned the precious metals complex. In late January, circulation of SHFE silver in the spot market tightened sharply, creating a rare backwardation structure; squeeze risk escalated rapidly, and the resonance of fundamentals and macro factors drove silver to its historic high. In early February, after a single-day plunge, silver rebounded quickly and consolidated above 25,000 yuan/kg. In mid‑February, the exchange tightened risk-control measures, squeeze sentiment gradually faded, and the extreme spike phase came to a temporary halt.

In March and April, rate-cut expectations continued to cool, and silver entered a trend pullback. In March, US inflation stickiness became increasingly apparent, and market bets on Fed rate cuts shrank persistently. The loose-trading theme unwound rapidly, and silver officially entered a downward trajectory, dipping to above 16,000 yuan/kg during the month. The market then entered a tug-of-war between longs and shorts; amid shifting expectations, silver prices stabilized and rebounded intermittently. April remained largely range-bound, lacking a clear directional breakout, as the market awaited further guidance from inflation and employment data.

In May and June, policy expectations completely reversed. Strong hawkish signals, combined with above-forecast inflation, accelerated the bottoming process. In May, US CPI and PPI data both exceeded expectations, and the labor market was surprisingly strong, shattering any remaining market hopes for rate cuts. Major institutions successively lowered and eventually erased their full-year rate-cut forecasts; the market consensus rapidly shifted from a “rate-cut cycle” to “higher for longer,” and silver prices resumed their decline. In June, the Fed’s meeting formally confirmed the policy pivot, with the dot plot showing no rate cuts for the year. US Treasury yields and the US dollar index rose in tandem, persistently weighing on silver’s financial attributes. Silver prices accelerated downward, eventually touching a half-year low of 13,816 yuan/kg, a decline of 55% from the peak.

H1 2026 Silver Ore Market Review: Peru Incidents Spark Supply Concerns, Import Surge Supports Domestic Raw Material

International Mine Disruptions: Peru Mine Disruptions Spurred Silver Price Surge of 7.3% in a Single Day

On May 11, 2026, the Presidential Palace of Peru issued Emergency Decree No. 003-2026. Affected by the ongoing energy crisis, some small and medium-sized mines with weak risk resilience and high-cost operations faced risks of production cuts or temporary shutdowns. Driven by both the energy crisis in Peru and escalating Middle East tensions, LBMA spot silver prices surged about 7.3% in a single day, reaching $86.1/oz.

According to the SMM survey, Peru holds a dominant position in global mined silver supply, and small and medium-sized mines account for as much as 75% of its domestic projects. Meanwhile, Peru represents half of China’s imports of silver-bearing concentrates. Once a substantial supply shortage materializes, it will cause a significant supply shock to both China and non-China markets. However, this incident remained largely at the sentiment-driven trading stage on news and has not yet been supported by sustained supply data.

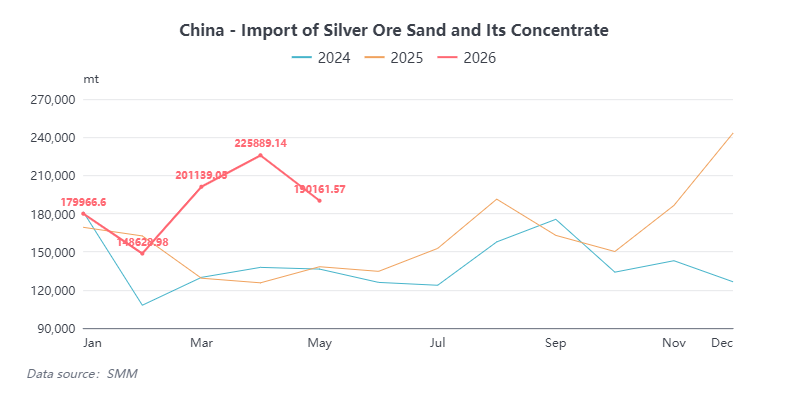

Import Market: H1 Import Surge, Full-Year Growth Expected Above 20%

In May 2026, China’s imports of silver-bearing concentrates were 190,000 mt, down 15.8% MoM; January-May cumulative imports reached 946,000 mt, up 30.4% YoY. Imports continued to surge in H1 this year, mainly due to persistent premium of SGE over LBMA spot silver prices, which attracted overseas miners to increase exports to China. Since May, the premium has narrowed, and imports have pulled back accordingly.

In 2025, China’s imports of silver-bearing ore were 1.94 million mt in physical content, up 16% YoY. Combined with the better-than-expected growth driven by the premium in H1 this year, China’s imports of silver-bearing ore are expected to maintain growth of over 20% for full-year 2026.

H1 2026 Silver Ingot Market Review: Stable Supply Growth, Surge in Imports Then Return to Normal, and Demand Structure Reshaping

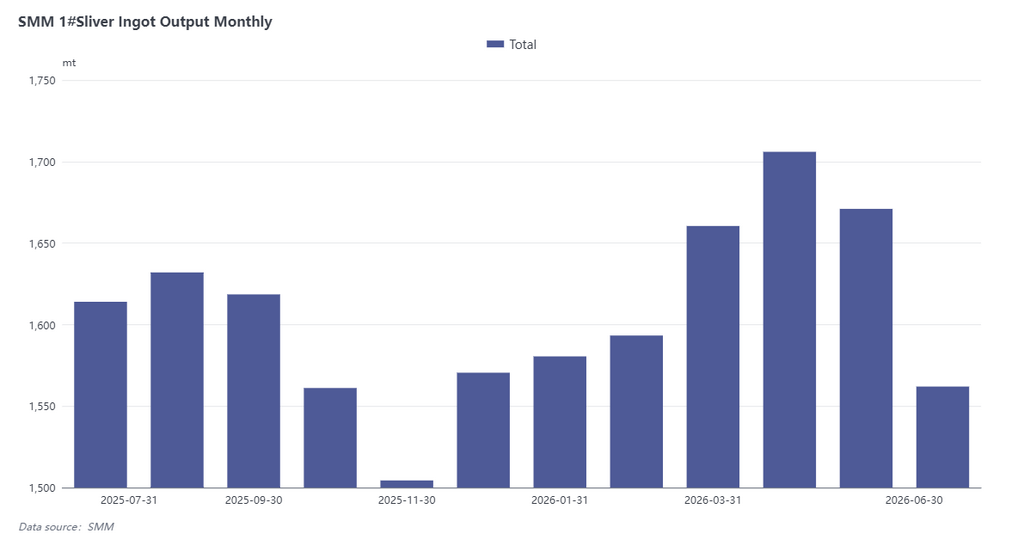

Supply Side: Silver Ingot Production Up 6.9% YoY, Full-Year Expected to Reach 20,000 mt

In H1 2026, China's silver ingot production rose initially then leveled off. According to SMM data, June output was 1,562 mt, down 6.5% MoM, mainly due to concentrated maintenance at copper smelters and temporary shutdowns at some producers. Cumulative production from January to June reached 9,773 mt, up 6.9% YoY, maintaining steady growth overall.

Looking at the full year, domestic mine silver supply remained broadly stable, while imports of silver-containing concentrates continued to grow. Together with higher by-product silver value and improved overall recovery rates, some enterprises plan to start up their precious metals lines in H2. Full-year 2026 silver ingot production is expected to reach around 20,000 mt, up about 7% YoY, accelerating from the 18,600 mt SMM #1 silver output in 2025. May–June is the traditional maintenance season for copper concentrates and lead concentrates, so the recent phased supply contraction is normal seasonal fluctuation; production is expected to gradually recover in July–August. Overall, H1 silver ingot supply fundamentals remained solid, laying a good foundation for H2 market operation.

Imports & Exports: Surge in Imports Then Return to Normal, H2 Focus on India's Tariff Disruption

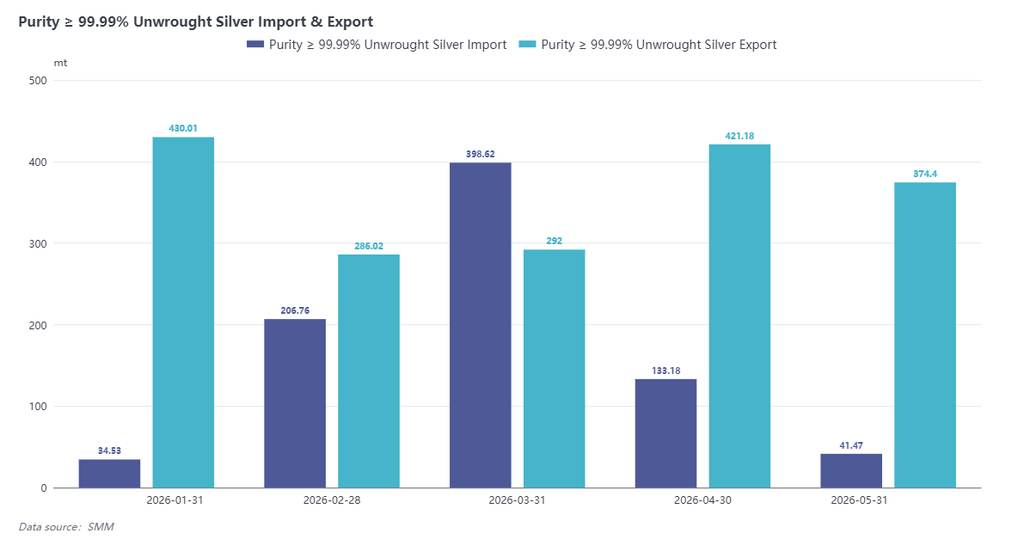

Exports: From January to May 2026, cumulative exports of refined silver totaled 1,803 mt, down 3.38% YoY, with 94.64% under processing trade with imported materials.

Imports: Imports of refined silver reached 815 mt in January–May, compared with net imports of only 16 mt in the same period last year. The sharp increase was mainly driven by a widening price spread between Chinese and overseas markets. With high domestic silver ingot premiums, speculative buying of overseas silver ingots in the Shenzhen area increased noticeably, and in March silver ingot trade briefly shifted to a rare net import mode. Some smelters could still capture sizable profits by exporting through processing trade with imported materials and then importing via ordinary trade. After April, the import window gradually closed, and refined silver trade returned to normal patterns. H2 exports are expected to remain stable, while imports will likely normalize in the absence of large disruptions to the price spread between Chinese and overseas markets.

In May 2026, India raised the basic customs duty on gold and silver imports from 5% to 10%. Indian banks proactively paid duties to resume bullion imports, completing customs clearance for 9 mt of gold and 34 mt of silver in May. India is a key demand market for silver jewelry and electronic components manufacturing globally, and the higher import duty in H2 could weigh on its purchasing demand, potentially having some impact on export markets.

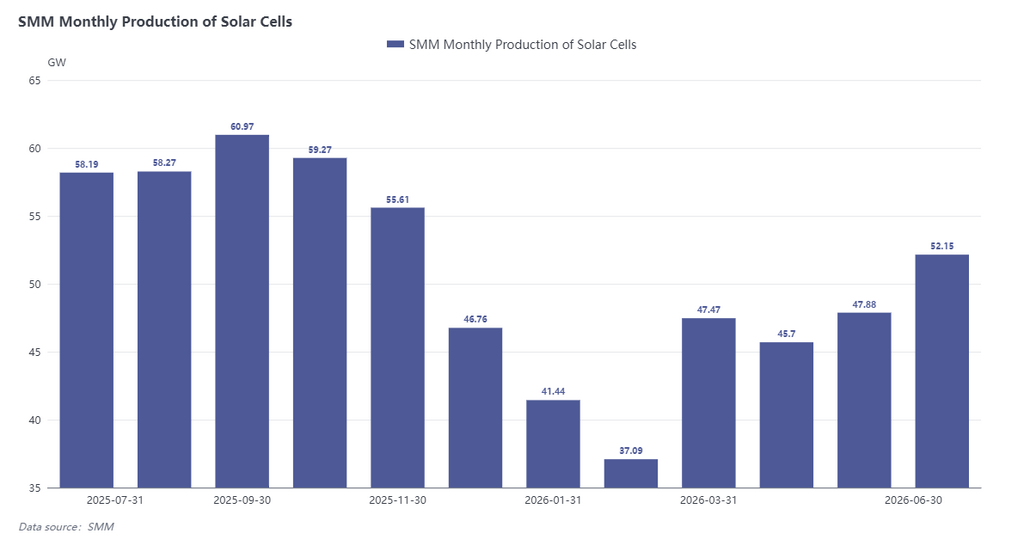

Demand Side: Silver Used in PV Down 21% YoY; Industrial Demand Takes Over as Main Driver from Investment

In H1 2026, solar cell production experienced a notable decline in Q1 followed by a gradual recovery in Q2. Q1 output dropped 22% QoQ, suppressed mainly by high silver prices (silver accounts for roughly 30%–40% of cell costs), the traditional production off-season and expectations that the PV module tax rebate policy would be cancelled in April, which weighed on stockpiling demand. Some enterprises staged a temporary rebound in April driven by an export rush. Entering Q2, ample orders for utility-scale modules, together with India's ALMM policy taking effect on June 1, prompted companies to front-load exports before the policy window closed, steadily lifting production schedules and causing output to edge up month by month.

From the perspective of total silver use in PV, the pace of copper-for-silver substitution has been modest. According to SMM data, average silver consumption per GW for solar cells in 2026 is expected at 9 mt/GW, down 5% YoY, with an annual decline of around 5% maintained through 2030. However, as end-user module output declines, annual cell production forecasts have been revised down, and silver use in PV in 2026 is estimated at about 4,935 mt, down 21% YoY.

Looking at the overall demand structure in 2026, silver use in PV contracted sharply, while investment demand took the lead in Q1. Industrial demand remained rigid, boosted by SiC chips, PCB circuit boards, and the new energy vehicle market. However, Q2 premiums and discounts showed that the market had cooled from earlier overheating in investment demand back to the industrial demand main driver. Combined with reduced demand from the PV sector, overall demand remained feeble. Affected by the traditional off-season in July and August, industrial demand support was insufficient. In H2, industrial demand is expected to gradually recover from September–October onward, and the silver demand narrative driven by AI development is likely to gradually materialize.

Outlook

Overall, silver’s performance in H1 2026 essentially reflected a valuation rebalancing after liquidity expectations faded, with extreme anomalies in the spot market further amplifying price swings. Early-year easing expectations had already front-loaded valuation potential, and short squeezes in the spot market pushed prices to extreme highs that deviated from fundamentals. Subsequently, rate-cut expectations reversed completely, and the high-rate environment continued to suppress precious metals’ financial attributes, serving as the core driver of the H1 downtrend.

For H2, the turning point signal in Q3 US inflation data and marginal shifts in the Fed’s policy stance will remain the key macro observation windows. The direction of the US dollar index and real yields on US Treasuries will directly determine the pace and scope of silver’s valuation repair. Before a clear turning point emerges in macro headwinds, silver is expected to maintain a consolidating and subdued trend overall. Meanwhile, fundamental factors such as the supply-demand pattern in the spot market should be watched, as they may serve as important triggers for periodic rebound rallies.