Price

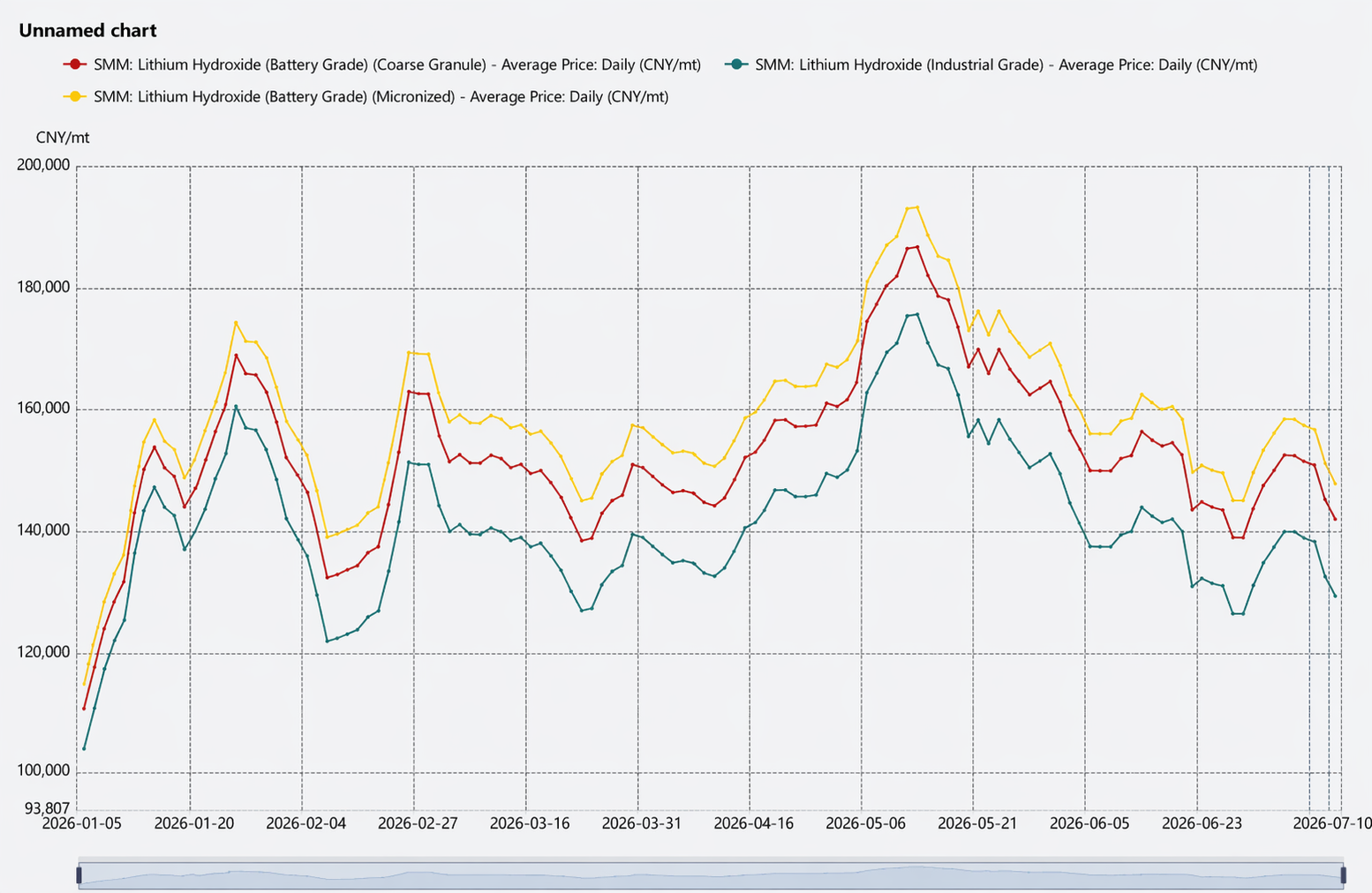

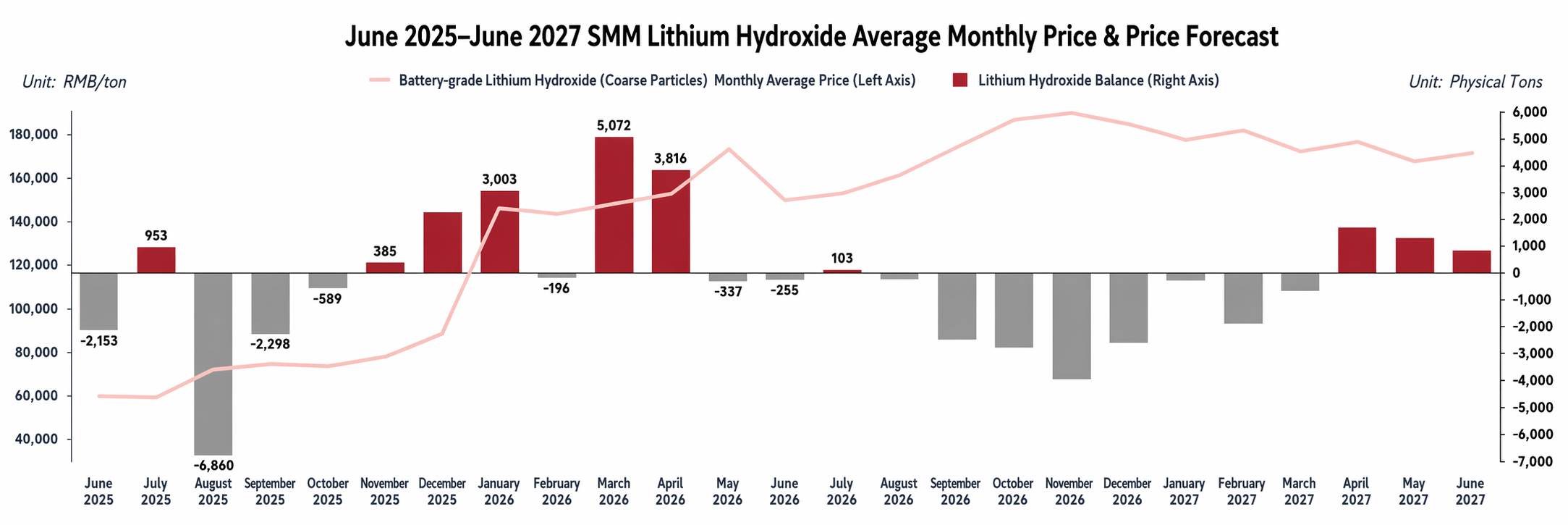

In H1, China's lithium hydroxide prices showed a trend of "surge—consolidation at highs—loosen and pull back", with the price center rising initially and then falling amid the interplay of multiple factors.

In January, prices surged sharply. Concentrated maintenance at leading lithium chemical plants tightened spot supply, while costs of lithium carbonate and lithium ore continued to climb, prompting lithium chemical plants to hold prices firmly. This drove the monthly average lithium hydroxide price to soar 65% MoM. Although ternary cathode material enterprises maintained just-in-time procurement and were cautious about spot orders, and the price spread between Chinese and overseas markets led to some import backflows, phased shortages and cost support still pushed prices to highs.

In February, prices consolidated at highs with trading activity turning sluggish. Macro sentiment dragged lithium prices lower overall, but smelters' firm pricing sentiment persisted. Downstream ternary cathode material manufacturers had sufficient inventories and some entered maintenance, easing raw material tightness, with purchases mainly based on monthly average prices. During the Chinese New Year, lithium hydroxide transportation stalled due to its hazardous chemical nature, and the market entered a seasonal quiet period. Post-holiday restocking demand was mediocre, and prices lacked upward momentum, resulting in wild swings throughout the month.

In March, price increases narrowed significantly. Battery cell manufacturers' cargo pick-up pace fell short of expectations, new orders for ternary cathode materials were limited, and increased customer-supplied materials mid-month caused spot orders to plummet. Market trading was sluggish, the upward price channel was blocked, and the monthly average price edged up only 3.4% MoM.

In April, prices fell first and then rose. In the first half, limited new orders for ternary cathode materials led to muted demand for spot orders, and prices were slightly under pressure. In the second half, driven by pre-holiday stockpiling and new orders, ternary cathode material manufacturers increased inquiries, and combined with sharp rises in lithium carbonate and lithium ore prices, lithium hydroxide prices strengthened, with the monthly average price up 2.73% MoM.

In May, prices retreated after a rapid rise. In the first half, expectations of improving demand and supply-side disruptions pushed lithium carbonate and lithium ore prices higher, pulling lithium hydroxide up in tandem. In the second half, lithium market sentiment weakened, traders and material manufacturers increased point-price transactions, and with the trend of ternary demand already set, upstream suppliers' firm pricing stance loosened, leading to a slight correction. The monthly average price reached 174,000 yuan/mt, up 13.6% MoM.

In June, prices pulled back notably with heightened price range volatility. Supply disturbances at the lithium resource side were frequent, and market fluctuations amplified significantly. Suppliers became cautious, quoting prices in line with market conditions. Upstream players adjusted prices flexibly, and traders maintained deep discounts (discount of more than 15,000 yuan/mt to the most-traded lithium carbonate contract). On the demand side, total ternary cathode material demand remained weak MoM, but in the 135,000-145,000 yuan/mt range, downstream players showed strong willingness to stockpile at lows, forming some bottom support and intensifying price range consolidation. The monthly average price fell 11.52% MoM.

From a price trend perspective, the linkage between lithium hydroxide prices and lithium carbonate futures prices strengthened over the past six months. On the one hand, upstream enterprises adopted a “lithium carbonate price × discount coefficient” approach in pricing as a floor price; on the other, traders leveraged the lithium carbonate-lithium hydroxide price spread and price differences in and outside China, importing lithium hydroxide and selling it with reference to lithium carbonate futures prices, further reinforcing this price linkage.

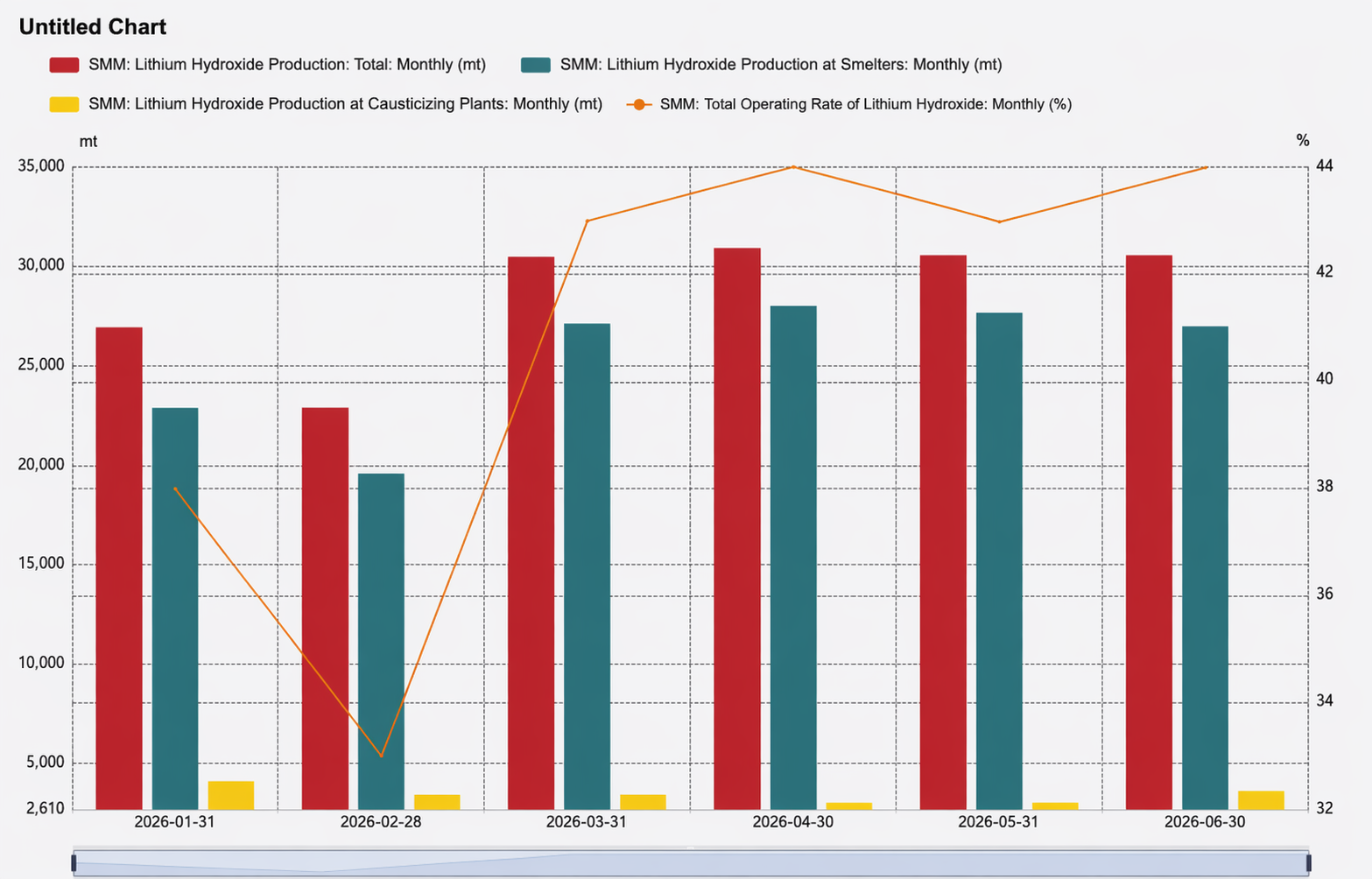

Production

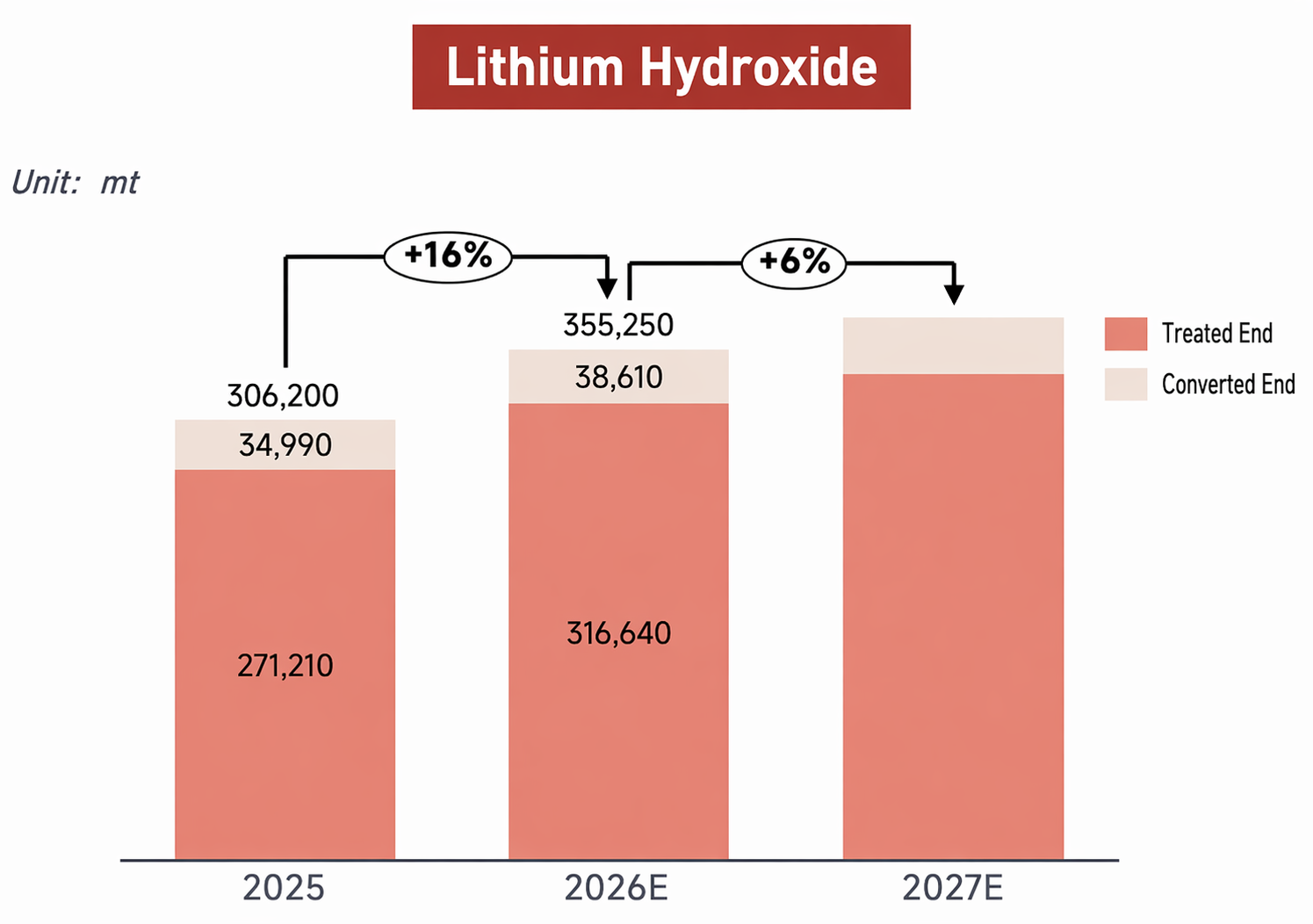

Production side: In H1 2026, China’s total lithium hydroxide production reached 172,000 mt, up 21% YoY, with relatively robust downstream demand driving notable growth. By output structure, the smelting segment contributed the largest share at around 88%. Among this, production ramp-ups at new lines of top-tier players added some volume, while other enterprises mainly relied on downstream orders for steady output; overall smelting segment production increased 18% compared to the same period last year. For the causticisation segment, most operating enterprises maintained stable production, with the H1 CR5 reaching 72% and market concentration remaining at a high level.

Regarding capacity utilization rate, although some capacity had already been switched to lithium carbonate production, the lithium hydroxide industry’s operating rate hovered below 50% throughout the first half, and overcapacity trends persisted.

Cost and profitability: In the smelting segment, lithium ore raw materials were relatively tight in H1 2026, with ore prices staying at a relatively high level and highly linked to lithium carbonate prices, providing strong cost support for lithium hydroxide. As a result, non-integrated producers faced significant sales pressure, and their product discount prices did not fall further, offering marginal support to profit margins at current price levels. In the causticisation segment, supply of salt-lake-based lithium chemicals increased over the past six months, and raw materials for causticisation were relatively abundant; the linkage between actual enterprise procurement costs and industrial-grade lithium carbonate quotes weakened, alleviating cost pressure on enterprises purchasing lithium carbonate externally to some extent and resulting in actual causticisation segment profitability exceeding theoretical estimates.

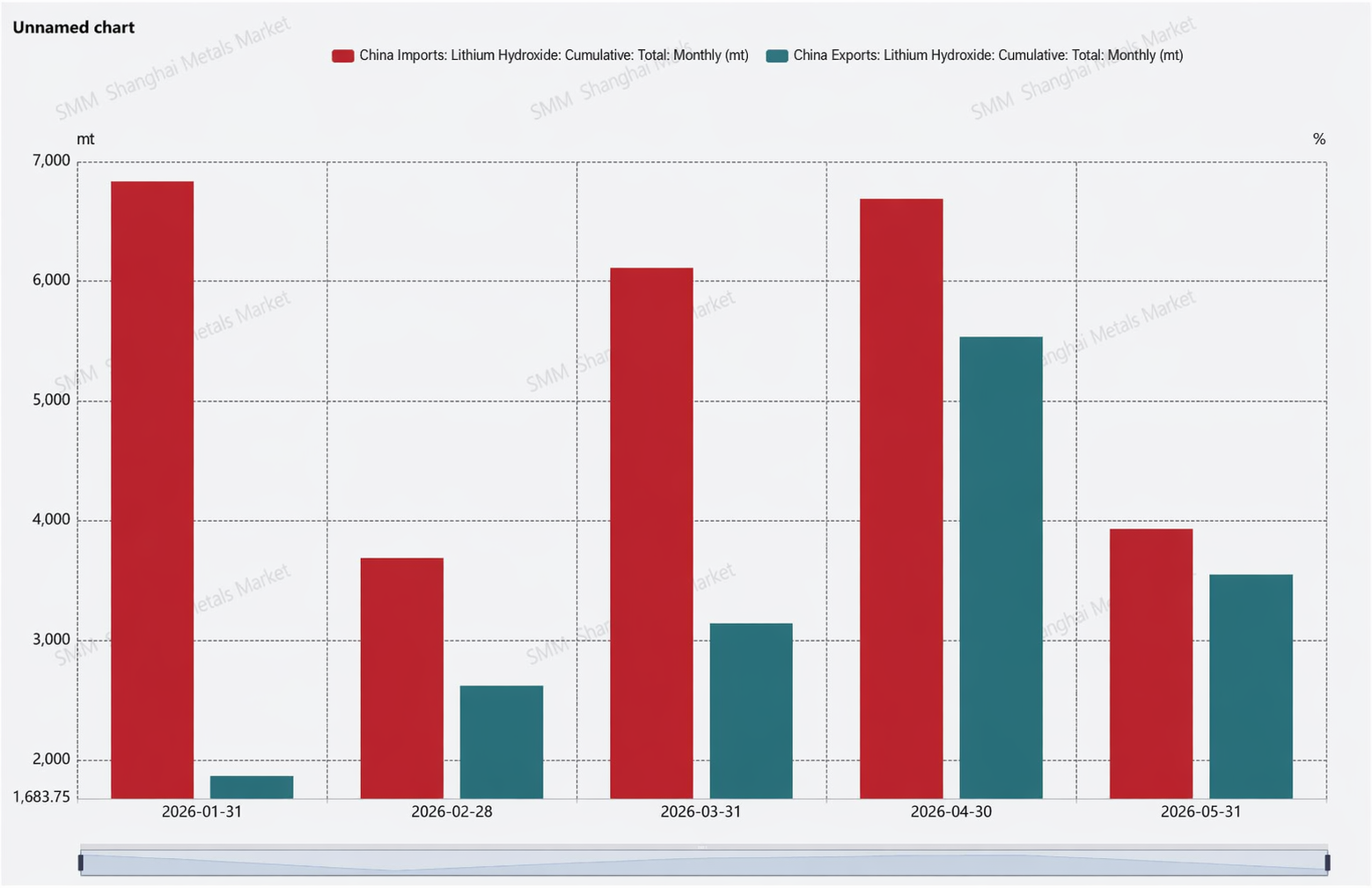

Imports and Exports

The pattern of imports and exports also underwent a notable reversal. On the export side, since H2 2025, some overseas ternary enterprises shifted to outsourcing processing to domestic toll manufacturers, causing products originally destined for export to be delivered domestically and effectively pushing down exports. Meanwhile, overseas ternary cathode material demand remained sluggish, downstream material plants showed weaker purchase willingness for Chinese lithium hydroxide, and local production lines outside China gradually ramped up, jointly keeping exports at low levels over the past six months. On the import side, driven by weak overseas demand, high prior inventories, and arbitrage opportunities, import volumes stayed at a relatively high level, further reinforcing the net import trend.

Balance and Inventory

The surge in import data led to a supply surplus in most months in H1. However, considering directly usable lithium hydroxide products, the overall market remained in a relatively tight balance, effectively supporting upstream price control efforts.

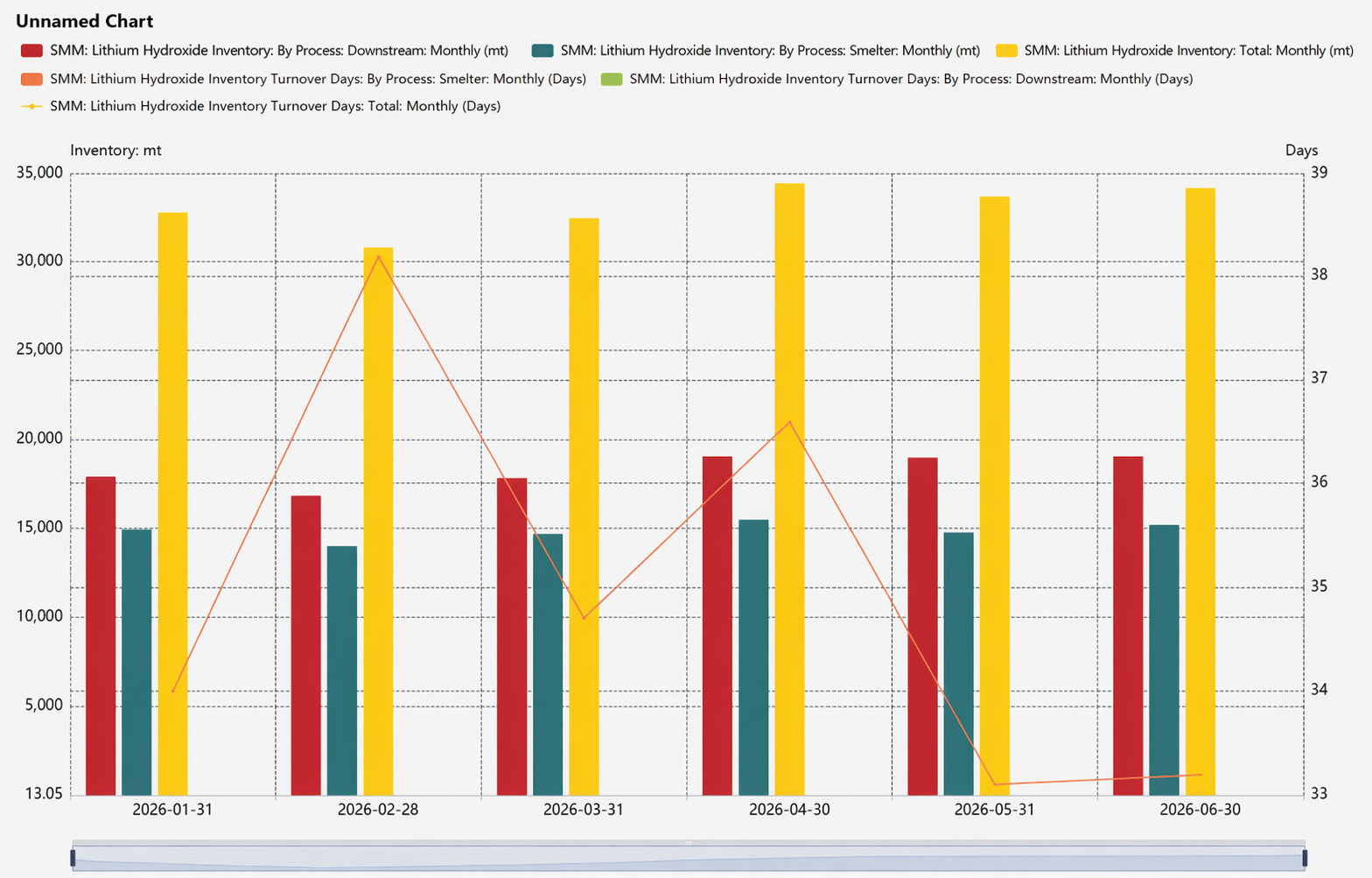

Regarding inventory levels, current lithium hydroxide inventories have improved significantly compared to the same period last year, driven primarily by two factors: first, some inventory was digested by converting into lithium carbonate and flowing into the market; second, operating enterprises flexibly adjusted their output pace, bringing days of inventories down to approximately one month.

Outlook

Going forward, although the LFP route continues to squeeze the ternary route, ternary cathode materials still face no rivals in the high-nickel segment. Additionally, the cost advantage of 6-series materials has opened up further possibilities for the ternary route. From the perspective of end-user production schedules, ternary battery demand is expected to maintain good momentum in H2 2026, with growth of approximately 36% compared to H1, which in turn brings about a 7% QoQ increase in demand for ternary cathode material output in H2. As ternary cathode materials continue trending toward higher nickel content, this generates a certain incremental growth trend in demand for lithium hydroxide. Meanwhile, considering that most lithium hydroxide production lines have the flexibility to switch or use carbonisation purification, lithium hydroxide production is expected to see approximately 6% growth in demand QoQ. Combined with a slight recovery in ternary demand outside China, the supply-demand balance for lithium hydroxide is expected to remain tight from 2026 to 2027.

In terms of pricing, given the highly concentrated supply structure, lithium hydroxide prices are primarily determined by the supply-demand relationship of its own industry chain and closely follow the price trend of lithium ore and lithium chemicals, currently consolidating above 150,000 yuan per mt.

Finally, regarding the listing of lithium hydroxide futures, Q2 saw frequent related developments.

The Guangzhou Futures Exchange and the Lithium Branch of the China Nonferrous Metals Industry Association explicitly stated their intention to continue strengthening cooperation and jointly promote the futures listing of lithium hydroxide and other lithium battery industry chain products; the draft of Guangzhou's 15th Five-Year Plan for the financial sector also explicitly supports GFEX in listing new energy futures products such as lithium hydroxide.

The industry side followed closely with intensive preparations. In June, Yahua, Chengxin Lithium, and Tianqi Lithium all announced approval to apply to GFEX for designated lithium hydroxide delivery factory warehouse qualifications; additionally, Milkyway’s shareholder meeting reviewed and approved a proposal for its subsidiary to apply to become a designated delivery warehouse for battery-grade lithium hydroxide on GFEX. According to media reports, lithium chemical plants (Ganfeng Lithium, Tianqi Lithium, Yahua Group, etc.) are already building out factory warehouse systems, but lithium hydroxide, due to its high hazardous chemical storage thresholds—strong corrosiveness, exothermic reaction with water, and requirement for inert gas protection—has seen no logistics players enter this product category so far.

At the market level, some traders had already positioned themselves in advance due to expectations of the futures listing, and the number of traders involved in lithium hydroxide import trade increased significantly.

In summary, the preparations for the listing of lithium hydroxide futures are progressing in an orderly manner, with positive official statements and accelerated industrial support.

![[SMM Analysis] Raw Material Side Under Pressure and Pulled Back, Graphitisation Costs Rose Sharply, June Anode Material Costs Stayed High](https://imgqn.smm.cn/usercenter/gcOsy20251217171726.jpg)

![[SMM Analysis] Expectations vs Fundamentals: Soft Volatile Co H1 2026, Stock Drawdown Offset by Surging Secondary Cobalt](https://imgqn.smm.cn/usercenter/BmqWy20251217171726.jpg)

![[Lithium Battery: Shanshan Shares Expects H1 2026 Net Profit Up 262% To 334% YoY]](https://imgqn.smm.cn/usercenter/QGlKw20251217171730.jpg)