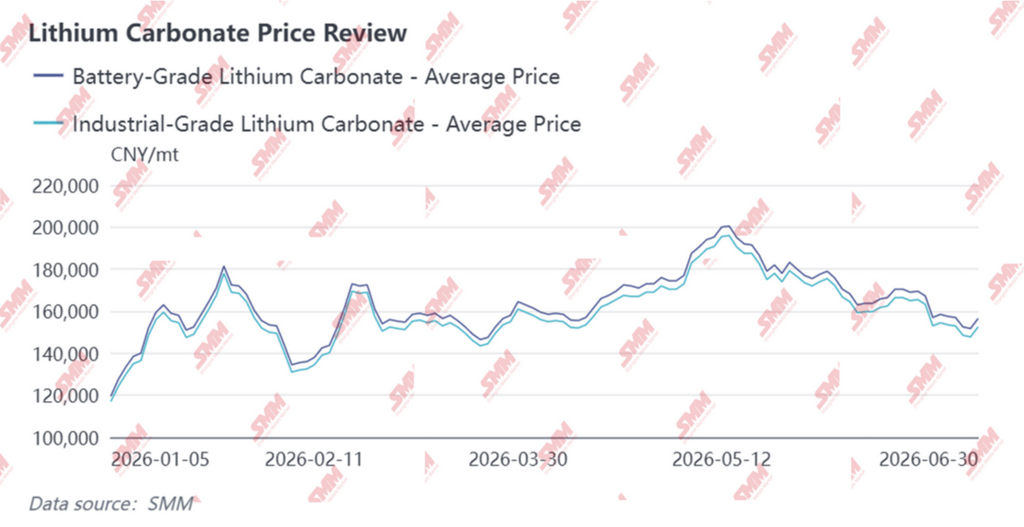

1. Price Review

In the first half of 2026, the domestic battery-grade lithium carbonate market experienced a period of dramatic and wide-ranging volatility, with the price centre shifting upwards overall. The interplay between supply and demand persisted throughout, whilst market sentiment fluctuated between optimism and caution. The average price range for the first half of the year was between 149,600 and 177,000 yuan per tonne, reflecting significant fluctuations.

First Quarter: Pre-holiday stockpiling and price-supporting manoeuvres led to prices rising, then falling, before rebounding

In January, spot prices for lithium carbonate showed a trend of sharp, volatile upward movement, with the monthly average price standing at 156,000 yuan per tonne—a month-on-month increase of as much as 55 per cent. On the supply side, output remained largely stable; however, as the proportion of long-term contracts signed with upstream and downstream partners declined, lithium salt manufacturers reduced their fulfilment of such orders. Consequently, there was little willingness to sell spot orders, and a growing sentiment of holding back sales to prop up prices emerged. On the demand side, downstream materials manufacturers stockpiled ahead of the Spring Festival in February, but their acceptance of rapidly surging spot prices was limited. They generally adopted a 'buy on dips' strategy, replenishing stocks only when prices corrected. During the month, the spot price of battery-grade lithium carbonate peaked at 181,500 yuan per tonne, before retreating to around 168,000 yuan per tonne by month-end.

In February, prices followed a pattern of falling first and then rising, with the monthly average standing at 149,600 yuan per tonne—a slight month-on-month decline of 3.5 per cent. At the start of the month, downstream players continued their pre-holiday stockpiling, but their procurement strategy remained cautious, focusing primarily on buying on dips. From the middle of the month onwards, downstream enterprises had largely completed their stockpiling, market trading activity slowed, and most adopted a wait-and-see approach. On the supply side, upstream lithium salt producers remained reluctant to sell spot orders, maintaining their stance on supporting prices; only a small volume of sales occurred at high price levels, leaving the market in a state of stalemate.

In March, prices strengthened once again, with the monthly average rising by 5 per cent month-on-month. On the supply side, as the maintenance season drew to a close, production gradually resumed, and lithium salt manufacturers showed increased willingness to sell at relatively high levels of around 170,000 yuan per tonne; on the demand side, cathode material manufacturers continued their strategy of buying on dips, showing strong willingness to purchase within the 140,000–150,000 yuan per tonne range. Due to sustained favourable demand, some enterprises engaged in substantial restocking at lower price levels. Prices surged to 172,500 yuan per tonne at the start of the month before retreating to around 163,000 yuan per tonne by month-end.

Second Quarter: External shocks compounded by supply disruptions; prices staged a deep V-shaped recovery before peaking and then falling

In April, the market staged a V-shaped recovery, with the monthly average price rising by 6 per cent month-on-month. In the first half of the month, escalating geopolitical tensions in the Middle East fuelled global risk aversion, putting pressure on non-ferrous metals and lithium carbonate prices, which fluctuated downwards. From the middle to the end of the month, a series of supply-side disruptions emerged—including Zimbabwe’s export ban and the licence renewal cycle for mines in Jiangxi—which, combined with rising cost-side support, drove prices to rebound, resulting in a marked upward shift in the price level by month-end. Negotiations between upstream and downstream buyers remained deadlocked, with the psychological price gap widening week by week: upstream suppliers held firm on prices and were reluctant to sell, maintaining high quotations; downstream buyers limited purchases to essential needs only, with their psychological price range centred between 155,000 and 175,000 yuan per tonne. Prices fell to around 155,500 yuan per tonne in the first half of the month, before surging strongly to 177,000 yuan per tonne by month-end.

In May, prices exhibited a trend of fluctuating upwards with a significant rise in the price centre, and the monthly average price rose by 12 per cent month-on-month. Disruptions on the supply side continued to escalate, compounded by downstream cathode materials and battery cell production schedules remaining at high levels, with production schedules for June expected to accelerate further; the mismatch between supply and demand in terms of timing remained unresolved. Upstream lithium salt producers maintained a stance of price support and reluctance to sell throughout the month; downstream, however, the market was divided, with some enterprises restocking at lower prices, whilst the majority had limited acceptance of high prices and focused primarily on purchasing to meet immediate needs, resulting in relatively subdued actual trading volumes. In the futures market, the main contract briefly broke through the 200,000 yuan per tonne mark during the month, leading to a period of euphoria in market sentiment.

Entering June, the price centre of gravity shifted downwards amid volatility. On the supply side, news of licence renewals for mines in Jiangxi continued to unsettle the market; however, China’s lithium carbonate imports reached a record high in May, whilst warehouse receipts at the Guangzhou Futures Exchange remained at a high level of around 50,000 tonnes, resulting in significant pressure from social inventories. Although demand growth met market expectations, it lacked any unexpected increases, leaving prices with insufficient upward momentum. Upstream lithium salt producers showed little willingness to sell spot orders, maintaining their stance of holding firm on prices and withholding sales; downstream materials and battery cell manufacturers continued their strategy of buying on dips, making substantial purchases to replenish stocks once prices fell below 160,000 yuan per tonne, thereby providing some support at the bottom of the market.

Looking back at the first half of the year, the lithium carbonate market experienced wide fluctuations with an upward trend, driven by a combination of factors including supply disruptions, geopolitical tensions and pre-holiday stockpiling. The psychological price gap between upstream and downstream sectors persists, market dynamics are becoming increasingly nuanced, and the correlation between futures and spot prices has further strengthened. As we enter the second half of the year, the pace of supply-side recovery and the actual realisation of end-user demand will become the key determinants of price direction.

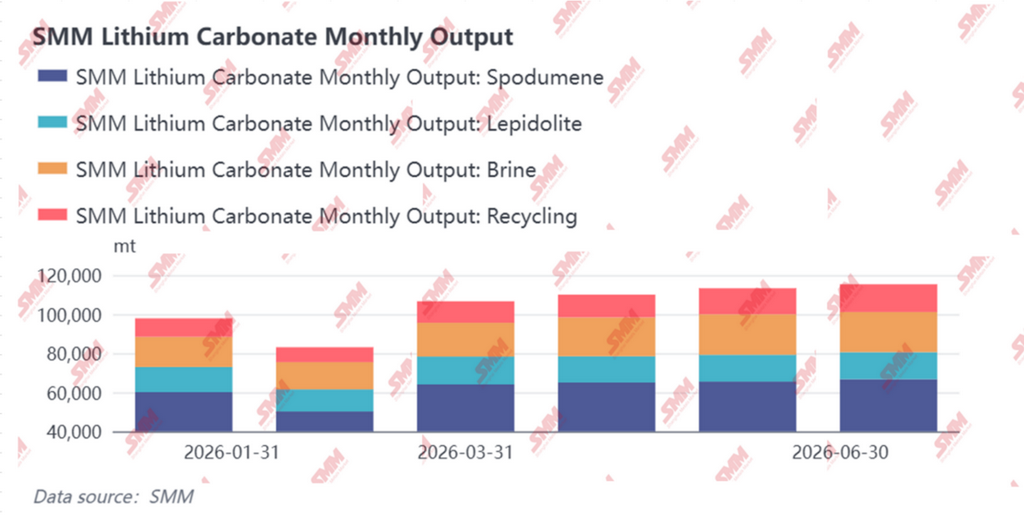

2. Supply Side

In H1 2026, China's lithium carbonate production followed a pattern of initial weakness followed by recovery and a steady ramp-up. Excluding the disruption from February maintenance, monthly output climbed progressively, with cumulative production reaching approximately 622,000 mt. The pace of supply recovery coincided with price movements at key junctures – the acceleration phase of production release aligned with the period when the price center moved higher, while periods of elevated supply overlapped with price pullbacks, underscoring the complex tug-of-war between sellers and buyers.

From a quarterly perspective, Q1 saw the most pronounced production fluctuations. In January, China's lithium carbonate production was 97,900 mt, down 1% MoM. Although some production lines had initiated maintenance plans in mid-to-late January, the continued ramp-up at certain new production lines effectively offset the output reduction from maintenance, leaving overall production largely stable. In February, however, the scope of maintenance expanded further. Coupled with fewer working days during the month, production dropped sharply to 83,100 mt, a MoM decline of 15%. The monthly lithium carbonate price center also pulled back from its January high. The supply contraction limited downside room for prices to some extent; prices fell first and then rebounded during the month, with the average monthly price down only 3.5% MoM — a relatively limited decline. March brought a notable supply rebound. As enterprises that had undergone maintenance after the Chinese New Year resumed production, new lines steadily ramped up, and demand-side strength boosted operating rates at non-integrated lithium chemical plants, monthly output jumped to approximately 106,600 mt, a MoM increase of 28%. The rapid supply recovery coincided with robust downstream procurement demand in March. Against this backdrop of both supply and demand growth, prices continued to drift higher, with the average monthly price up 5% MoM.

Entering Q2, the pace of production ramp-up became steadier. April production was approximately 110,000 mt, edging up about 4% MoM, with the main contributions coming from continued ramp-up at new salt lake lines and further improvement in operating rates at non-integrated lithium chemical plants. Prices in April traced a V-shaped pattern due to geopolitical shocks. While supply-side output remained steady, expectations of tightening raw material supply — triggered by Zimbabwe’s export ban and Jiangxi mine license renewals — provided strong support for the price rebound in the second half of the month. May production rose further to approximately 113,300 mt, up about 3% MoM, with salt lake and recycling operations providing steady incremental gains from ramping up. Notably, although Zimbabwe banned lithium concentrate exports, raw material inventories held by relevant enterprises were sufficient to ensure normal production in May, and output was not materially impacted. During the month, ongoing supply-side disruptions combined with strong demand to lift the price center significantly, with the average monthly price surging 12% MoM. June production was approximately 115,300 mt, basically flat MoM. New capacity in both the recycling and spodumene sectors continued to be released, but factors including maintenance and raw material allocation constraints capped further expansion, keeping overall output stable at high levels. The June price center drifted lower as imports climbed to a record high and warrants hovered around 50,000 mt. With domestic production holding steady, this failed to effectively support prices, and the market center pulled back to around 160,000 yuan/mt.

Looking at the first half as a whole, supply went through three key turning points. First, concentrated maintenance and production cuts in February led to a phase of tightening supply, which — combined with pre-Chinese New Year stockpiling demand — contributed to price resilience in January–February. Second, the concentrated resumption of production in March saw output surge 28% MoM; under the dual-growth pattern of supply and demand, prices continued to rise, confirming that demand elasticity was stronger than supply release during that phase. Third, production plateaued at high levels in Q2, with April–June output stabilizing in the 110,000–115,000 mt range. However, May imports surged to a record high and warrants continued to accumulate, causing total supply pressure to emerge in June and becoming a key reason the price center came under pressure and pulled back that month. Heading into H2, the pace of Jiangxi mine production resumptions, the circulation of spodumene concentrates, and the speed of new capacity releases will be the core supply-side variables to keep tracking.

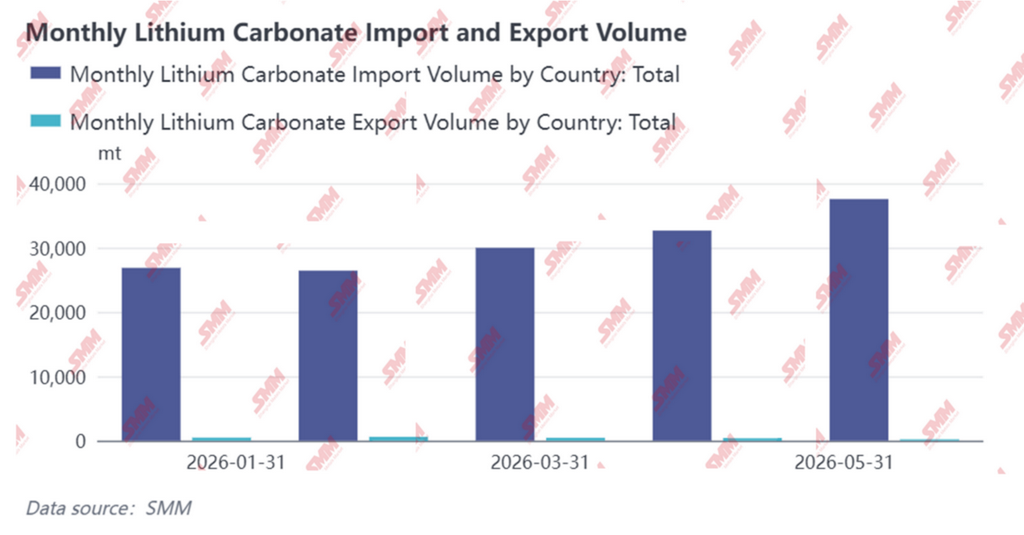

On the Import and Export side, China's lithium carbonate imports climbed month by month in H1 2026, with mounting external supply pressure becoming a significant source of growth for domestic supply. Meanwhile, exports continued to shrink, further reinforcing the net inflow pattern in the Chinese market.

In terms of total imports, China imported a cumulative 153,000 mt of lithium carbonate over January–May, up 53% YoY. Monthly imports rose steadily from the start of the year: January imports stood at 26,858 mt, up 12% MoM; February pulled back slightly to 26,427 mt, down 2% MoM but still surging 114% YoY; March imports rebounded to 29,974 mt, up 13% MoM; April further increased to 32,650 mt, up 9% MoM; and May imports climbed to 37,555 mt, up 15% MoM and 78% YoY, marking the highest monthly import volume in H1.

In terms of import sources, Chile and Argentina remained the two pillars of China's lithium carbonate imports. From January to May, Chile's monthly import share held steady in the 58%–65% range, while Argentina's share gradually increased from 32% in January to the 30%–39% range by May. Together, the two countries accounted for over 90% of China's total imports. Indonesia, as an emerging source, maintained monthly imports in the 1,000–2,100 mt range, representing a share of about 1%–7%—a relatively limited volume but offering some supplementary effect. Notably, imports from Argentina reached 10,353 mt in February, with share rising to 39%, a relatively high level in recent years, reflecting the continuous release of Argentina's salt lake lithium extraction capacity and deepening penetration of supply into the Chinese market.

On the export side, H1 saw a continued contraction. Cumulative exports over January–May were only 2,087 mt, up a marginal 1% YoY. China's position as a net importer of lithium carbonate further strengthened in H1, with imports exceeding exports by more than 70 times.

Lithium sulfate imports also maintained rapid growth. Cumulative imports of lithium sulfate over January–May reached 71,000 mt, up 105% YoY. As an important intermediate raw material for lithium carbonate production, the surge in imports indicates that overseas lithium resources, after initial processing, are entering China in the form of intermediate products, further broadening the raw material sources for domestic lithium carbonate production and serving as indirect evidence of expansion in downstream processing capacity. It should be noted that the import trend may see a phased shift in June. According to Chile's customs shipment data, Chile's lithium carbonate shipments to China pulled back significantly from May to June. Considering shipping schedules, this decline is expected to be reflected in China's import data in mid-to-late June and July, which means China's lithium carbonate imports in June are expected to see a significant MoM pullback.

3. Demand Side

In H1 2026, downstream demand for lithium carbonate showed a quarter-by-quarter strengthening trend. In Q1, the pace was relatively slow due to the Chinese New Year holiday and the impact of subsidy phase-outs, but in Q2, demand expanded significantly driven by both the power and energy storage sectors. Monthly production schedules of cathode materials climbed steadily, becoming the core force boosting lithium carbonate consumption.

Q1: Weakened temporarily in January–February, then rebounded strongly in March. In January, China's NEV market was affected by the previous purchase tax halving policy, which had frontloaded car-buying demand, resulting in a notable decline in sales and visible pressure on power battery demand. In the ESS sector, although the steady ramp-up of new capacity supported a slight increase in ESS battery cell production, it was not enough to offset the drag from the power side, leaving overall electrolyte and cathode demand sluggish. In February, the seasonal off-season around the Chinese New Year further suppressed end-use demand. Demand for both power and consumer electronics batteries remained sluggish, and with fewer effective production days, both ESS and power battery enterprises cut their production schedules. The downstream procurement pace for lithium carbonate slowed markedly, and cathode material producers focused on digesting inventories. In March, the market reached a clear turning point. Automakers intensively launched new car models while simultaneously stockpiling for new products and digesting inventories, leading to a rapid recovery in power battery demand. Large-scale energy storage bases and grid-side ESS projects accelerated construction across multiple regions, and with the implementation of the capacity tariff policy, ESS batteries continued their high-growth trajectory. Battery cell enterprises kept raising their production schedules and operating rates. Purchasing willingness among cathode material producers increased significantly, and they generally restocked heavily within the price range of 140,000–150,000 yuan/mt. Monthly lithium carbonate demand climbed from around 124,700 mt in January to 132,200 mt in March, a MoM increase of about 6%.

Q2: Demand was fully unleashed, with production schedules staying high. From April to June, the industry continued to see growth in both supply and demand. On the power side, China's NEV exports maintained strong momentum. At the same time, rising energy prices pushed up the operating costs of internal combustion engine vehicles, further stimulating NEV consumption. The domestic auto market achieved a slight increase in sales. In the energy storage sector, driven by the long-term rigid demand from the global energy transition and the construction of new-type power systems, project implementation picked up pace, and installed capacity expanded steadily. Entering May–June, production schedules of downstream cathode materials and battery cells remained high. The June production schedule was expected to accelerate further. With the approach of the grid connection deadline (June 30), front-loaded stockpiling demand from the energy storage downstream was released intensively. The overall improvement in end-use demand prompted battery cell enterprises to keep ramping up production. Monthly lithium carbonate demand further increased from around 140,400 mt in April to 147,700 mt in May, then climbed to 151,000 mt in June, representing demand growth of approximately 14% from end-Q1 to end-Q2. On the procurement strategy front, downstream enterprises generally adopted a "buy on dips" approach. They stockpiled intensively when prices retreated to the range of 155,000–175,000 yuan/mt, with some making large purchases to stockpile below 160,000 yuan/mt, demonstrating strong price flexibility. Structurally, in the ternary cathode material sector, although the cancellation of the export VAT rebate policy has intensified cost pressure on cathode material producers targeting markets outside China, overseas battery cell manufacturers have not opted to switch suppliers, and Chinese cathode material producers have maintained irreplaceable competitiveness by leveraging their technology and cost advantages. Top-tier producers are accelerating the construction and validation progress of their overseas bases in South Korea, Europe and other regions, and it is expected that in H2 2026 and 2027, overseas new capacity will begin a substantial ramp-up in shipments. However, affected by the slowdown in global NEV sales growth and the US policy rollback, overseas ternary cathode production is expected to decline by about 6.5% in 2026. In the LFP sector, markets outside China are at a critical stage of transitioning from reliance on Chinese imports to local supply. South Korean enterprises are accelerating their transition from the ternary to the LFP technology route. Multiple enterprises have officially announced capacity plans, and it is expected that South Korea will gradually build up LFP capacity in H2, making it one of the faster countries in terms of capacity rollout outside China. Alongside the accelerated deployment of energy storage projects by overseas battery plants and the rollout of certain power battery projects, overseas demand for LFP cathode materials is gradually increasing. However, local production is relatively tight, and in the short term, it still relies heavily on imports from China, which provides a certain level of demand support for Chinese cathode material exports.

Overall, H1 lithium carbonate demand went from a "low-then-high" pattern in Q1 to a full-scale volume release in Q2, with monthly demand climbing steadily from 124,700 mt in January to 151,000 mt in June, representing cumulative growth of about 21%. The structural characteristics of demand were equally distinct: the dual-drive pattern of power and energy storage deepened continuously, with the growth elasticity in the ESS sector significantly outperforming that in the power battery sector; downstream procurement was highly price-sensitive, and the "buying on dips" strategy prevailed throughout, forming clear demand support at key price levels.

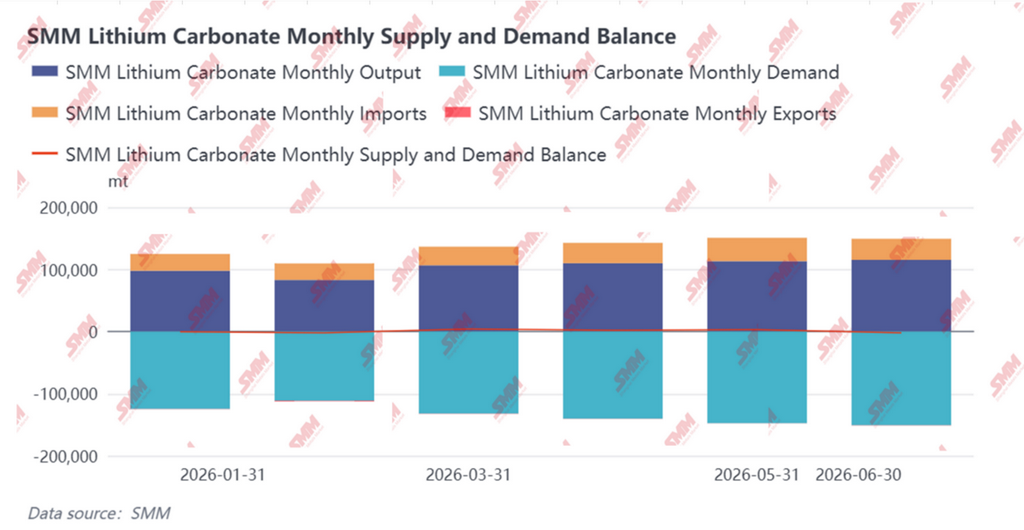

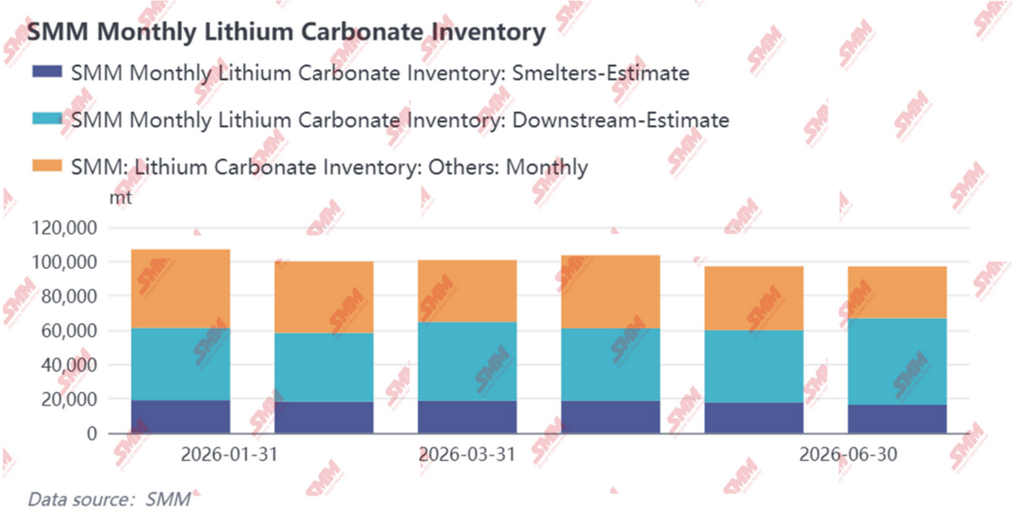

4. Supply-Demand Balance and Inventory

From a supply-demand balance perspective, China's lithium carbonate market exhibited a tight balance in H1 2026, with sellers and buyers continuously seeking new equilibrium points amid bargaining.

In H1 2026, lithium carbonate inventory shifted from the "demand-led destocking" of 2025 to "structural fluctuations driven by price bargaining". Upstream price-firming and downstream cautious purchasing constrained each other, and the declining proportion of long-term contracts intensified the volatility of the spot market. Although overall inventory did not accumulate significantly, inventory transfers between stages were frequent — upstream swung between holding back from selling and making shipments; downstream switched between restocking on dips and consuming inventory; traders became the main buffer amid price fluctuations. The market is gradually moving from the destocking phase driven by supply-demand mismatch in 2025 to a fragile balance state with high price sensitivity in H1 2026.

5. H2 2026 Outlook

Looking at H1 2026, the lithium carbonate market, driven by both supply disruptions and demand resonance, experienced wild swings with an upward shift in the price center. Entering H2, how the supply-demand pattern will evolve has become the market's focus. According to the latest SMM data, China's lithium carbonate market is expected to show persistent shortages in H2, and the price center is likely to rise further, supported by destocking.

Supply Side: Multiple Growth Drivers Gradually Materializing, Notable Increase in Operating Rates

China's lithium carbonate production is expected to reach approximately 786,000 mt in H2. By raw material, lepidolite sources, benefiting from expected production resumptions at major mines in Jiangxi, will see actual effective supply increase YoY. Spodumene remains the core source of growth for the full year; supported by resilient end-use demand and an upward shift in the lithium price center, toll processing orders for non-integrated enterprises will surge, production line operating rates will improve, and production will grow notably. Salt lake and recycling sources, driven by the accelerated commissioning and steady release of new capacity, will see steady production increases, directly contributing to the full-year growth. Overall, robust end-use demand combined with rising lithium prices will significantly improve production profit expectations for lithium chemical enterprises, driving them to increase production loads. The full-year operating rate is expected to rise notably YoY. Imports and Exports: Lithium

Concentrate Imports Gradually Recover, Net Import Pattern of Lithium Carbonate Continues

On the import side, driven by overseas long-term contract orders and toll processing demand for lithium sulfate raw materials from some domestic smelters, monthly imports are expected to remain at 30,000–32,000 mt. On the export side, given China's relatively small lithium carbonate export scale, coupled with relatively high domestic lithium carbonate prices and sustained demand improvement, enterprises have limited willingness to export. Additionally, lithium carbonate produced from salt lakes outside China still retains a certain cost advantage. Overall, China’s lithium carbonate exports are expected to stay stable going forward.

Demand Side: LFP Sustains Strong Momentum, Ternary Market Steady with Progress

Looking ahead to H2 2026, the LFP market is expected to continue its growth trend. In the second half, a significant amount of new capacity will gradually be completed and enter the ramp-up phase, with total industry capacity expected to exceed 10 million mt/year and full-year production reaching 6.12 million mt. However, the pace of new line ramp-ups and actual attainment of full production will need to be monitored for their impact on the supply rhythm. In terms of product mix, demand for high-compacted-density materials continues to increase; the promotion of large-format energy storage battery cells and commercial vehicle applications will continue to boost the share of 3.5th- and 4th-generation high-compaction products, while 5th-generation materials gradually scale up to meet downstream demand for higher energy density. The share of lower-generation products is expected to shrink further, with the industry structure continually shifting toward high-end.

In the ternary cathode market, power battery demand both in and outside China remained high in June 2026, with production expected to be flat MoM and up 37.1% YoY. However, as battery cell manufacturers had already built sufficient inventory in Q2, combined with Q3 being the traditional off-season and raw material supply tending to loosen, demand has room to pull back. Meanwhile, the export tax rebate for lithium batteries is about to be cancelled in Q4, which could bring some front-load orders to the Chinese market. China’s ternary cathode production in 2026 is expected to reach 975,000 mt, up 19% YoY.

Supply-Demand Balance and Price Outlook: Sustained Destocking Supports a Fluctuating Upward Price Trend

From a comprehensive supply-demand perspective, the domestic lithium carbonate market will see continued significant destocking in H2. Although supply growth is being steadily released, rigid demand growth, structural upgrades, and limited import supplementation together widen the supply-demand gap. Under this pattern, lithium carbonate prices are expected to maintain a fluctuating upward trend.

![[SMM Analysis] Riding the Winds In and Outside China, Breaking the Iron Law of Old Cycles: 2026 Energy Storage Battery Cell Semi-Annual Review and Outlook](https://imgqn.smm.cn/usercenter/WBREf20251217171728.png)

![[SMM Analysis] Separator Market 2026 Semi-Annual Review: Supply-Demand Pattern Tightens Marginally, Price Center Gradually Moves Up](https://imgqn.smm.cn/usercenter/gcOsy20251217171726.jpg)

![H1 Refined Cobalt Price Surged over 97% YoY; Demand Remains the Current Focus; What Can the Market Expect Going Forward? [Weekly Observation]](https://imgqn.smm.cn/usercenter/oVqJl20251217171730.jpg)