1. H1 Market Review

Price Trends: Highs Followed by Lows, with the Center Continually Shifting Downward

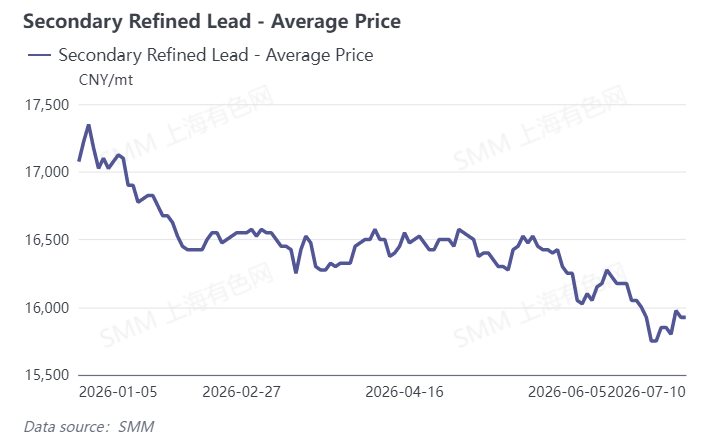

In H1 2026, secondary lead prices overall exhibited a pattern of retreat after rapid rise and drifting lower. According to SMM data, secondary refined lead averaged 17,075 yuan/mt at the start of the year, spiked to the intra-year high of 17,350 yuan/mt on January 7, and then entered a downward trajectory. From late January to February, downstream restocking falling short of expectations during the Chinese New Year and inventory buildup pulled prices back to around 16,500 yuan/mt. From March to April, the market consolidated under pressure, with prices holding in a narrow range of 16,250–16,575 yuan/mt. From late May, the off-season combined with macro headwinds weighed on prices, accelerating the decline, and by end-June they fell below 16,000 yuan/mt. As of July 10, secondary refined lead was quoted at 15,925 yuan/mt, having fallen by 1,150 yuan/mt cumulatively in H1, a decline of 6.7%.

Production: Sliding from Highs, Operating Rates Remain Weak

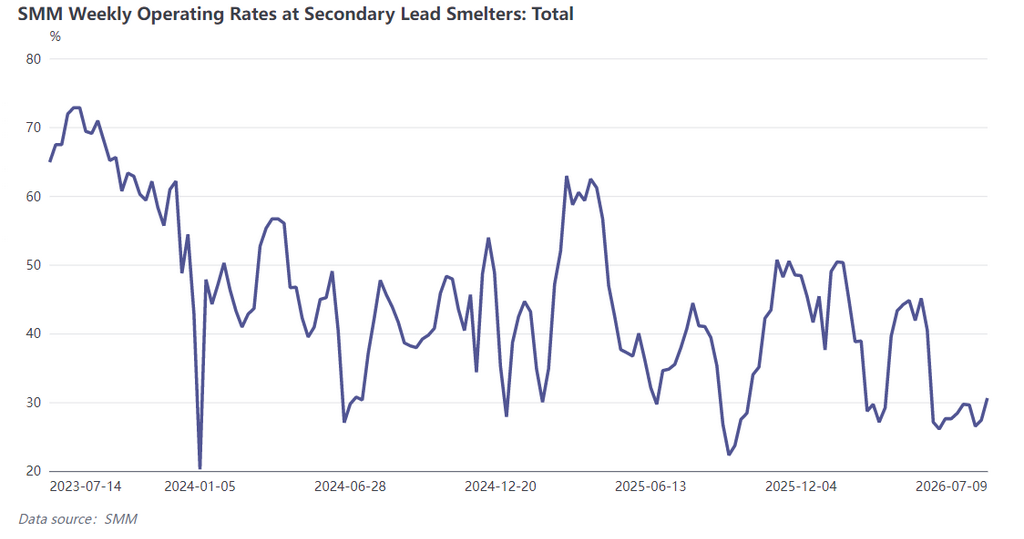

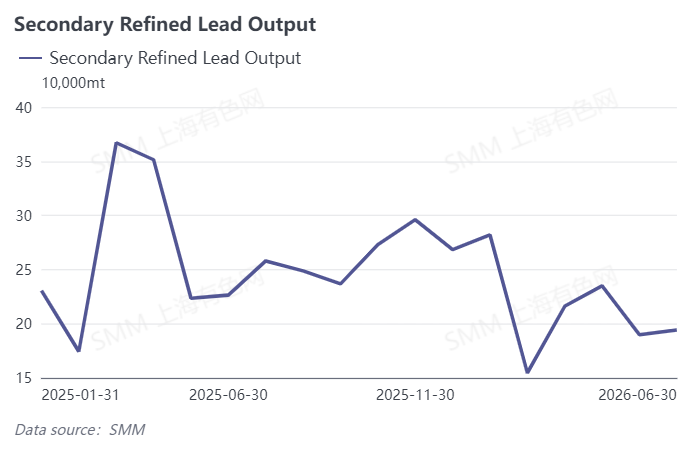

In H1, secondary refined lead production showed a high-early, low-later pattern. January output recorded a peak for the year of 282,000 mt, then declined month by month thereafter. Due to the Chinese New Year, production resumptions were slow in February, and the weekly operating rate across four provinces in China dropped from around 50% in early January to a low of 27.12% in early March. The operating rate briefly rebounded to 43.26% in late March before sliding again. In May, maintenance and production cuts across the industry were implemented intensively; four large smelters in east China, north China and the northwest halted production, and seven large and medium-sized enterprises implemented phased production cuts. Monthly output fell 18.96% MoM and 9.26% YoY. In June, output edged up only 2.23% MoM, representing a pullback of 31.2% from the January peak, and the weekly operating rate in the four provinces remained stuck at low levels of 28.4%–29.7%, with overall industry operating rates sluggish.

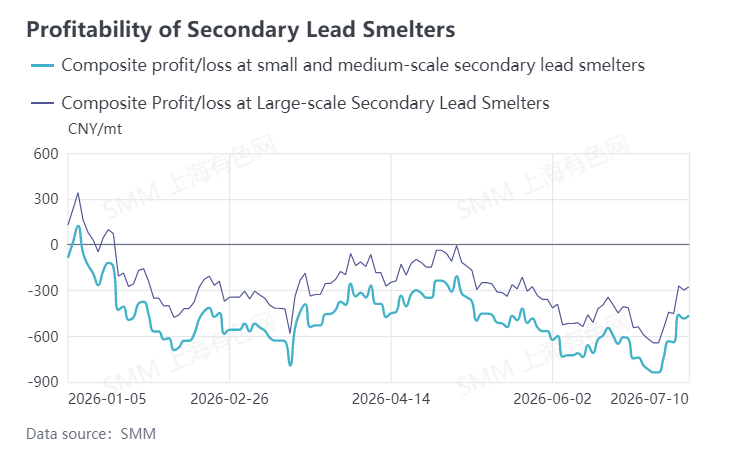

Profit: The Entire Industry Mired in Losses

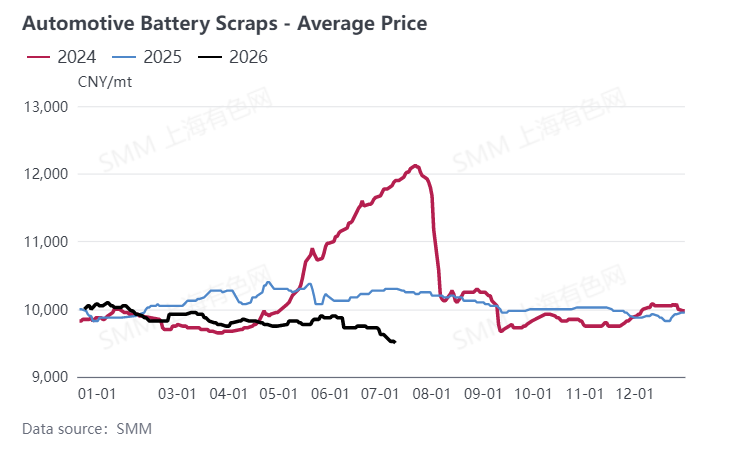

In H1, profitability in the secondary lead sector continued to deteriorate, with the industry suffering losses under pressure throughout. In early January, large enterprises still had a slim profit of 79 yuan/mt, but the average price of waste EV batteries holding at a high cost of 9,725 yuan/mt, combined with selling products at a discount, quickly pushed industry profits into the red. By end-February, losses widened further, with large enterprises losing 344 yuan/mt and small and medium-sized enterprises losing 558 yuan/mt. In subsequent market fluctuations, losses only narrowed briefly and the industry remained unable to return to profitability. As of July 10, large enterprises lost 277 yuan/mt, while small and medium-sized enterprises lost 464 yuan/mt. The core challenge for the sector is the rigid inversion caused by stubborn raw material costs and low selling prices of finished products, together with alternating price inversions between secondary and primary lead, which causes smelters to generally “lose money as soon as they produce.”

II. H2 Market Outlook

Price side, SMM expects secondary lead prices to remain in the doldrums in H2. High scrap battery costs provide rigid bottom support for lead prices, but triple negative factors—macro rate hike expectations, high LME inventories, and the downstream consumption off-season—continue to cap the upside room. If stockpiling demand during the subsequent peak consumption season (August-September) is released as expected, coupled with persistently low supply, prices are expected to stabilize and rebound periodically, but with limited magnitude.

Production side, secondary crude lead production in July is expected to edge up MoM by less than 10,000 mt from June, while secondary refined lead output edges down amid stability. A major east China plant that underwent maintenance in June plans to resume production in early July, and a northwestern smelter that previously postponed operations is watching the market. However, under the triple constraints of tight scrap battery recycling, no significant narrowing of industry-wide losses, and an ongoing end-user off-season, a substantial output surge is hard to materialize. The medium and long-term production recovery depends on three key variables: whether scrap battery recycling circulation can improve, the strength of recovery in battery end-user orders, and the scale of imported lead ingot arrivals.

Profit side, in the short term the industry will continue to bear the double squeeze of “high costs and weak prices.” Profitability improvement hinges on a rebound in lead prices and an easing of scrap battery costs. In H2, the focus will be on the pace of end-user restocking during the peak consumption season and raw material arrivals.

![Lead Market Supply and Demand Both Weak, Beware of Risk of Lead Price Retreat after Rapid Rise before Delivery [SMM Lead Market Weekly Forecast]](https://imgqn.smm.cn/usercenter/LCtEk20251217171721.jpeg)

![Lead Prices Dipped Before Rebounding, While Spot Market Trading Turned Quiet [SMM Refined Lead Spot Market Weekly Review]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)

![End-use Market Consumption Is Weak, Lead-acid Battery Price Increases Are Difficult [SMM Lead-acid Battery Market Weekly Review]](https://imgqn.smm.cn/usercenter/PKFMX20251217171721.jpg)