News on July 10, 2026:

In H1 2026, chrome ore prices exhibited notable phase-specific fluctuations, rising continuously in Q1 and grinding lower in Q2.

I. Price Review: Cost-driven increase; surplus-driven grinding lower

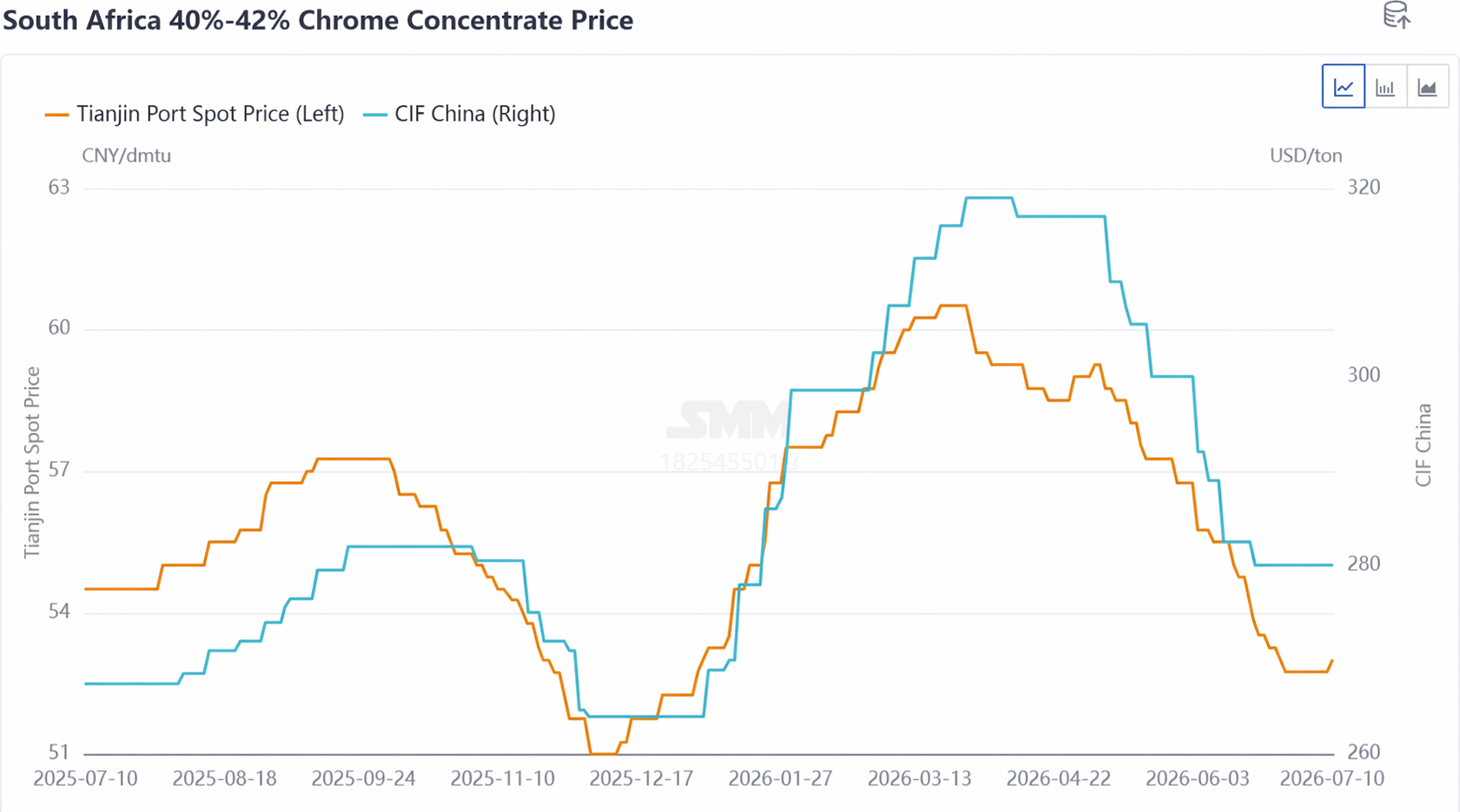

Taking 40-42% South African chrome concentrate as an example, the Q1 domestic spot price rose from 52.5 yuan/mtu to 60.5 yuan/mtu, and the offers from major overseas mines increased from $264/mt to $319/mt. Earlier, influenced by Indonesia's tightening of nickel ore quotas, stainless steel prices rose notably. Stimulated by bullish expectations, the overseas chrome ore market took the lead in raising offers. Coupled with stocking demand for Chinese New Year by domestic ferrochrome plants, spot offers in China followed the uptrend. Subsequently, the outbreak of the Middle East US-Iran conflict caused fuel prices to soar, significantly pushing up ocean freight rates for chrome ore. The elevated costs underpinned a further upward adjustment in chrome ore prices.

In Q2, an evident surplus of chrome ore emerged, and mounting shipment pressure drove chrome ore offers to start grinding lower. The Middle East conflict eased somewhat, and shipping costs for chrome ore stopped rising and stabilized. Meanwhile, global chrome ore shipments remained at a relatively high level of 2.8-3 million mt, resulting in ample supply. With concentrated port arrivals, chrome ore port inventories accumulated continuously. At the same time, ferrochrome producers had completed concentrated stockpiling earlier, so their willingness to purchase was limited, and they mostly adopted a wait-and-see attitude toward chrome ore price trends, leading to insufficient actual transactions. Confidence among chrome ore suppliers weakened, and they began to sell off at lower prices to surrender profits. South African chromite concentrate prices, which were in abundant supply, dropped significantly from 60.5 yuan/mtu to 55 yuan/mtu; while high-grade chrome concentrate and mainstream chrome ore spot cargoes were relatively tight, so their declines were limited, presenting an overall divergent trend.

II. Supply Landscape: Stable shipments, inventories continuously hitting new highs

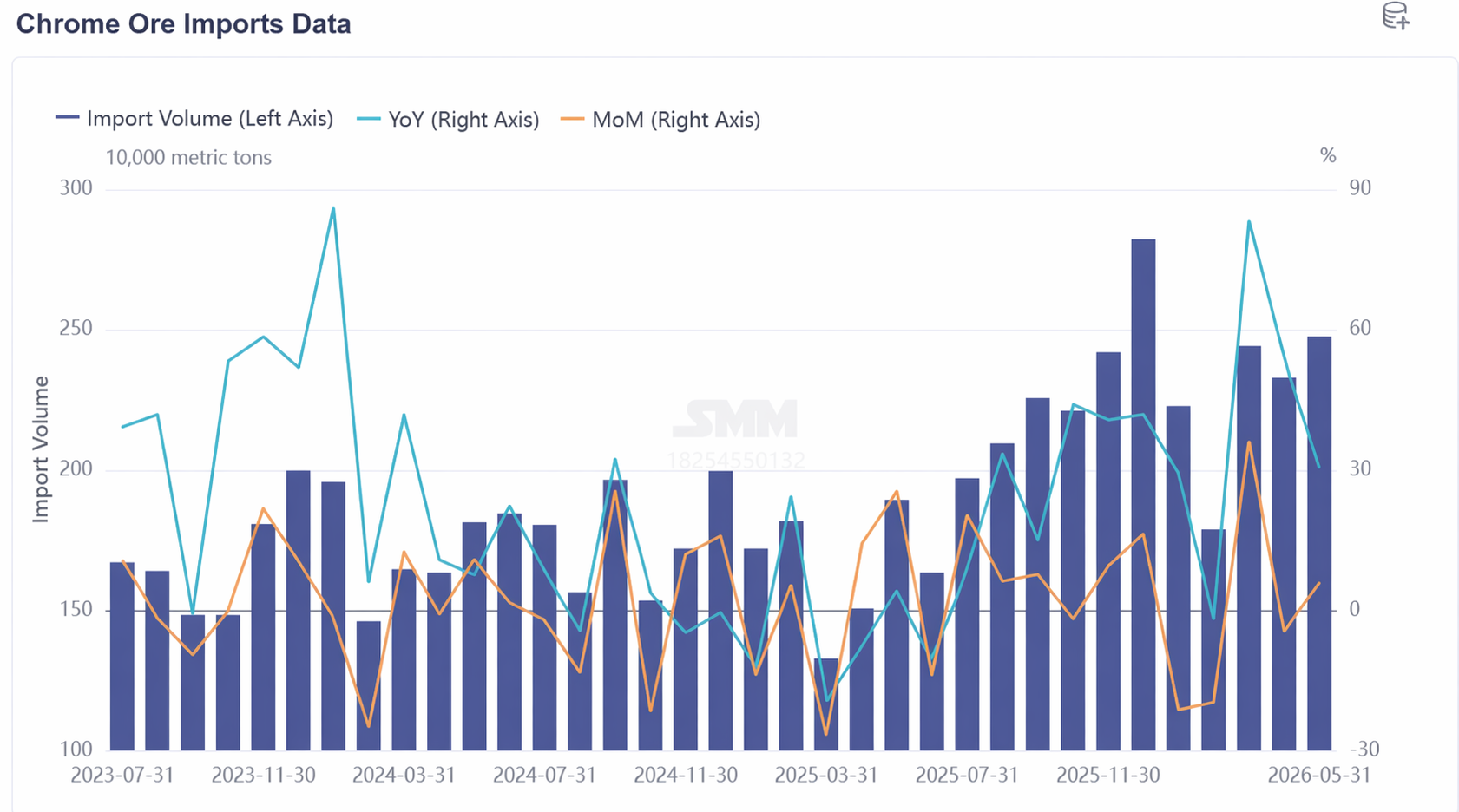

According to SMM data, from January to June 2026, global chrome ore shipments totaled 16.0796 million mt, up 13.87% YoY, with monthly shipments maintained at 2.8-3 million mt. Meanwhile, China's total chrome ore imports from January to May 2026 amounted to 11.2556 million mt, averaging 2.2511 million mt per month, up 36.36% YoY. Except for February, when flooding during South Africa's rainy season disrupted chrome ore transportation, chrome ore supply in H1 2026 remained at high levels overall, and the loose supply landscape was unlikely to change in the short term.

From a compositional perspective, South Africa continued to dominate firmly. In H1 2026, chrome ore imports from South Africa totaled 8.96 million mt, up 29.91% YoY, accounting for 79.64%. In 2025, massive ferrochrome production cuts in South Africa caused local chrome ore absorption capacity to plummet, prompting mines to focus more on exports, leading to a continuous increase in South African chrome ore supply. At the same time, supplies from Zimbabwe and Turkey also showed a clear upward trend. Chrome ore imports from Zimbabwe reached 989,600 mt, up 44.3% YoY, representing 8.8%; imports from Turkey reached 694,600 mt, up 170.17% YoY, accounting for 6.13%.

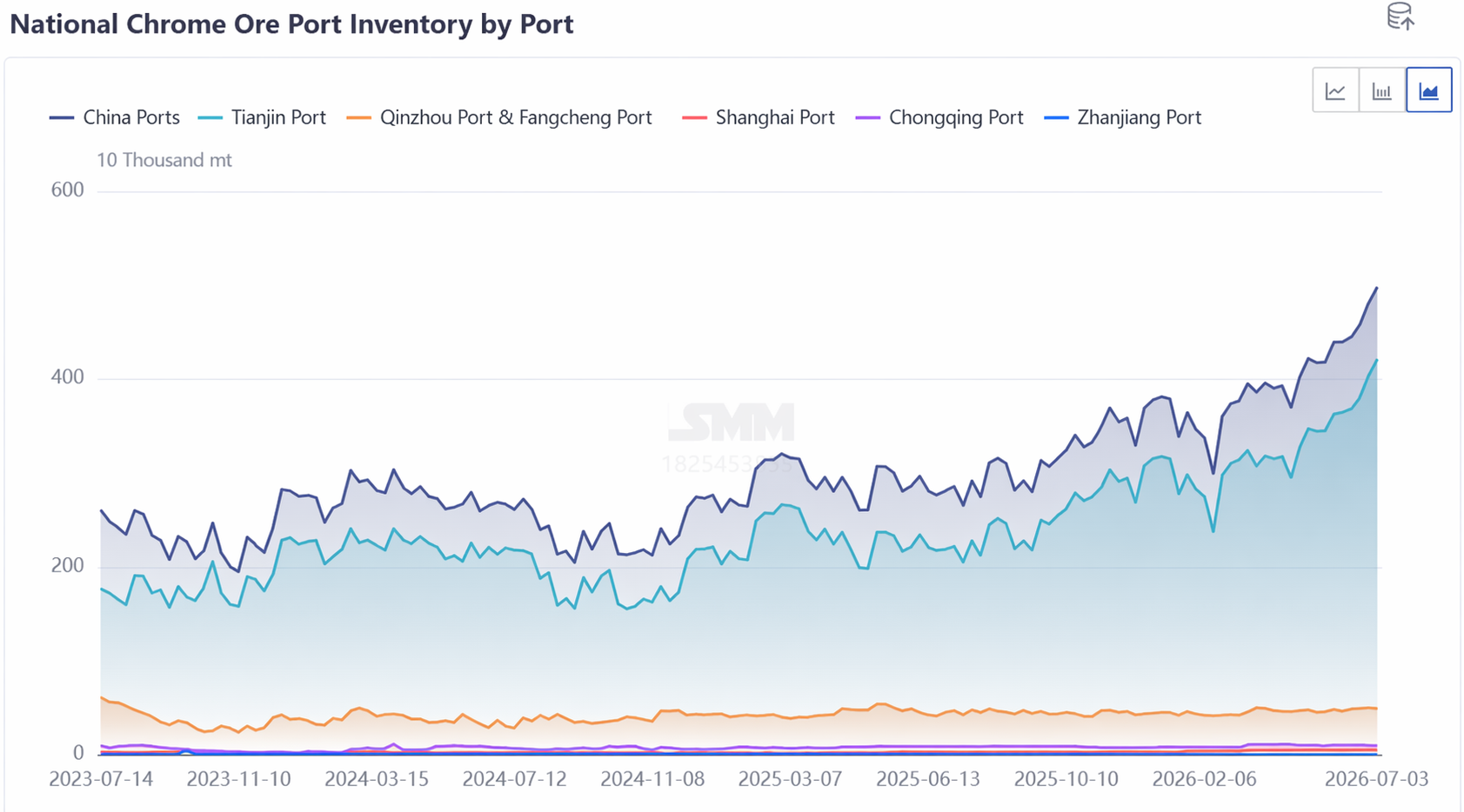

Concentrated port arrivals and rising warehouse inflows pushed port inventories to repeatedly break highs. By the end of June, China's chrome ore port inventory totaled 4.7 million mt, up 67.86% compared to the same period last year. Affected by bearish expectations from the downstream consumption off-season, ferrochrome producers on the demand side mostly maintained a wait-and-see stance, with limited purchasing interest, and chrome ore has yet to see a destocking inflection point.

III. Demand Landscape: Stable production, but sluggish procurement pace

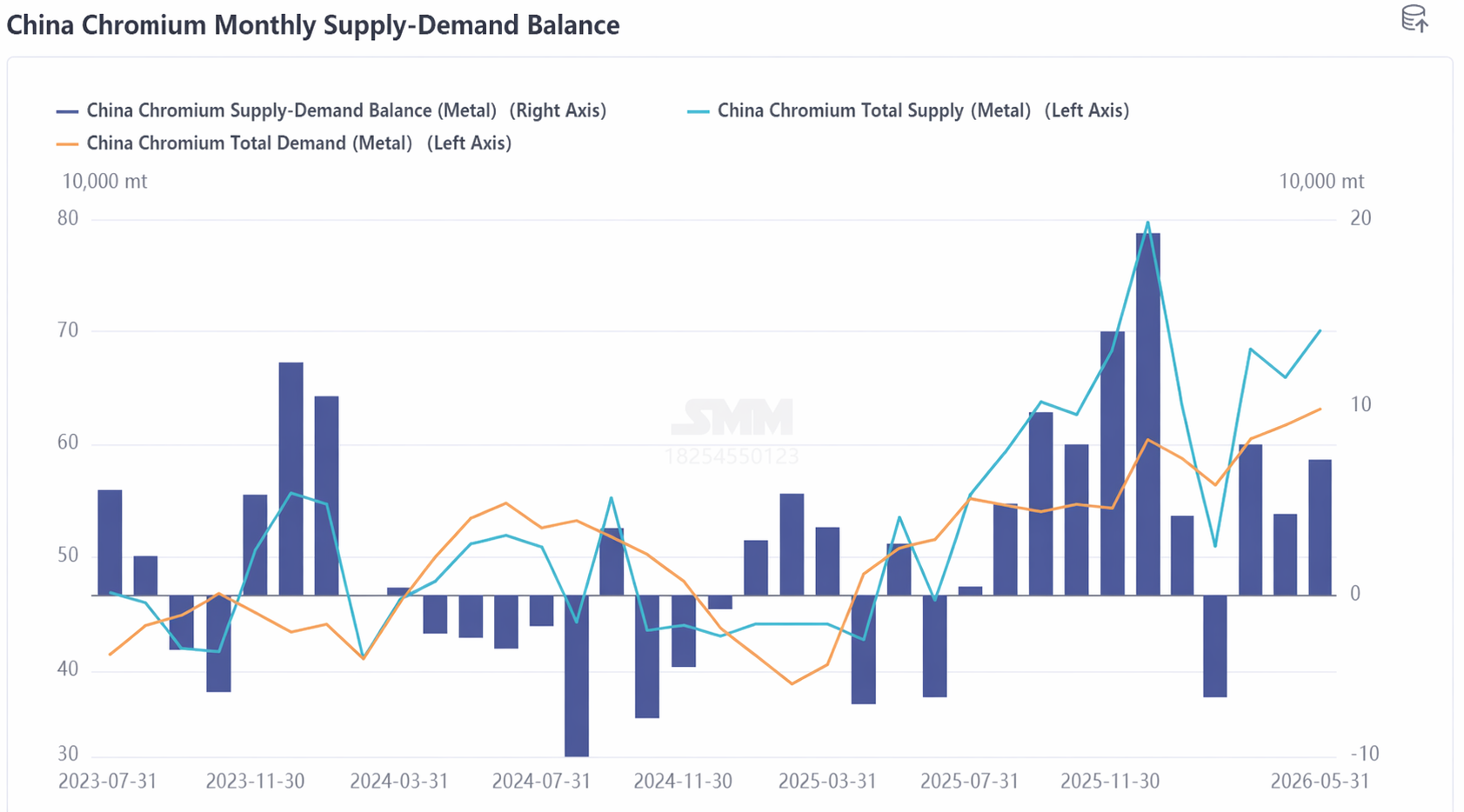

In H1 2026, domestic ferrochrome production trended upward overall, averaging 900,200 mt per month, up 36.79% YoY, providing bottom-level rigid demand support for chrome ore. However, ferrochrome producers mostly completed raw material stockpiling in Q1. In Q2, influenced by the drifting lower of downstream stainless steel, they adopted a hand-to-mouth strategy with no long-term stockpiling. Consequently, inquiry and procurement demand for chrome ore raw materials appeared relatively weak, forcing chrome ore prices to grind lower. Also, considering the evident loose chrome ore supply, ferrochrome producers maintained a strong wait-and-see attitude and, affected by weakening ferrochrome prices amid oversupply, lacked confidence in future prospects. They pushed for lower prices, resulting in a tug-of-war stalemate between buyers and sellers.

IV. Market Outlook:

In the short term, under oversupply conditions, the chrome ore market is expected to continue moving sideways in a narrow range. On one hand, South Africa's ferrochrome production resumption process is slow, and local chrome ore absorption capacity remains weak. Monthly exports are expected to stay high at an average of 2.4 million mt, so the likelihood of a decline in chrome ore shipment supply is relatively small. On the other hand, the consumption off-season continues to weigh on the stainless steel market, with steel mills carrying out production cuts and maintenance. Pessimistic expectations will be transmitted upward, dragging down ferrochrome prices. Ferrochrome producers will mainly purchase as needed, so chrome ore demand will be less than port arrivals, keeping port inventories high with little chance of destocking in the short term. However, given the high uncertainty in the international situation, overseas chrome ore mining and transportation costs will provide bottom support, limiting the room for deep declines, and prices are expected to remain largely stable. Attention should be paid to developments in South Africa's ferrochrome production resumption, downstream stainless steel and ferrochrome production schedules, and changes in the macroeconomic and international situation.

![[SMM Analysis] 2026 Chrome Ore Market Review: Supply-Demand Dynamics Reversed, Soaring Inventories Weigh on Prices](https://imgqn.smm.cn/usercenter/ZsMtd20251217171723.jpeg)

![Market wait-and-see sentiment is strong, and spot price gains are limited [SMM SiMn Weekly Review]](https://imgqn.smm.cn/usercenter/tjmLW20251217171722.jpeg)

![[SMM Manganese Ore Weekly Review] Overseas market broadly declined, coupled with weak demand, and manganese ore prices were under pressure and stagnant.](https://imgqn.smm.cn/usercenter/cgspx20251217171725.jpg)