SMM, July 10:

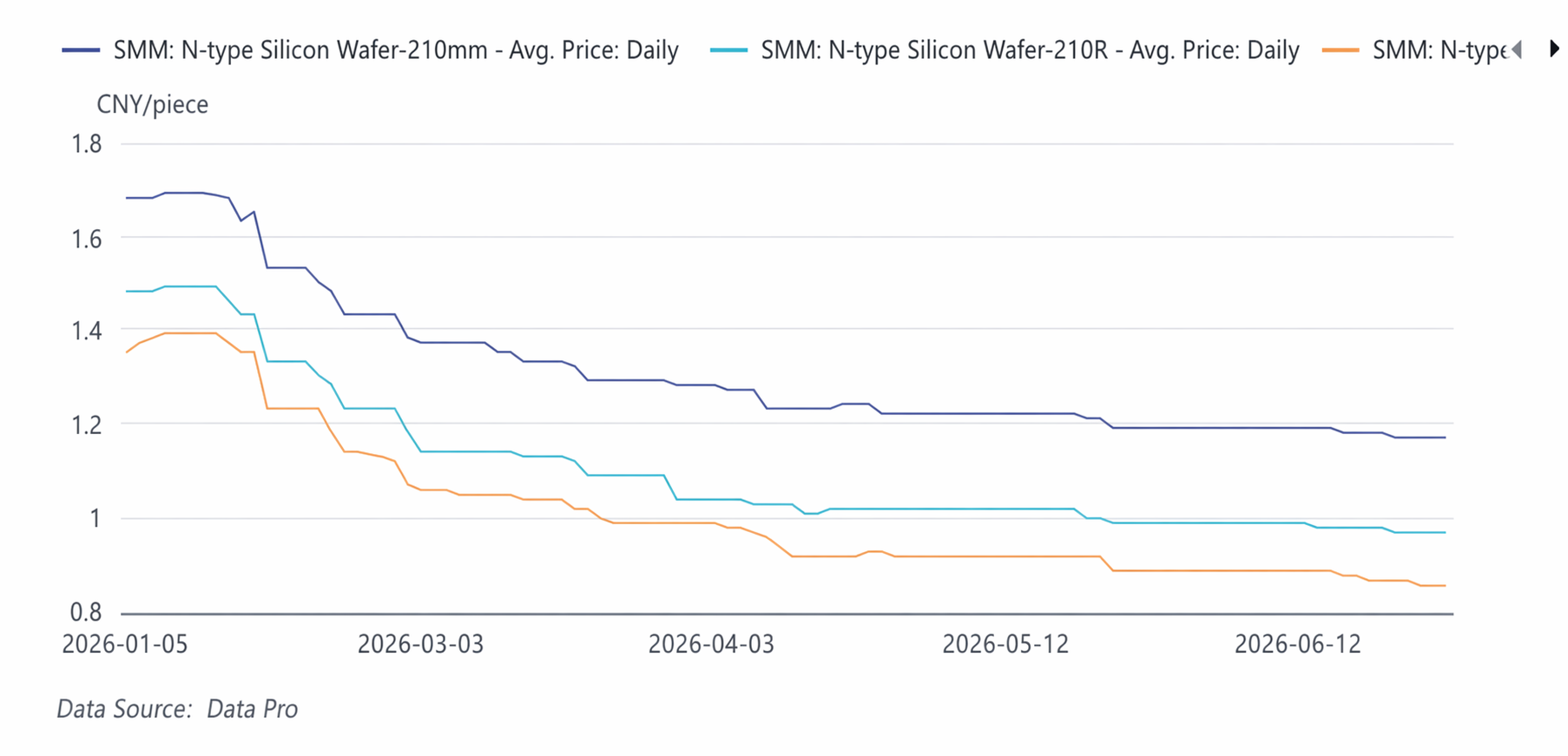

In H1 2026, the PV wafer market, under the combined pressure of supply-demand imbalance and policy adjustments, underwent a cycle of stepwise price declines, production schedules that rose first then fell, and accelerated capacity rationalization.

Mid-January to Mid-February: A sharp decline cycle. Prices entered the year building on a rebound triggered by the National Energy Administration's campaign against industry involution at the end of 2025, but as the Chinese New Year off-season set in and the earlier restocking cycle in the industry chain concluded, demand weakened rapidly, driving prices sharply lower. The 182mm wafer index pulled back from a mid-January high of 1.39 yuan/piece to 1.14 yuan/piece in mid-February, a cumulative drop of roughly 18% over one and a half months.

Late February to Mid-April: The decline narrowed and prices stabilized in stages. In March, wafer producers’ production schedules rose 10.71% MoM, but downstream solar cell plants simultaneously raised operating rates significantly, fueling a phased destocking of wafers, which visibly slowed the price decline. In April, producers proactively cut production schedules by 5.4%, market prices stopped falling, and small and mid-sized producers followed the pricing of top-tier players.

Late April to End-June: Top-tier producers held prices firm, while smaller producers saw divergent grinds lower. Leading wafer enterprises jointly defended their price floor, but downstream, an oversupply in the solar cell sector combined with falling silver prices drove cell prices below cash costs, exerting constant pressure upstream on wafers to push for lower prices and sell. The market showed a clear tiered pattern: large producers maintained higher price ranges, while second- and third-tier producers offered discounts to move volume. The market weakened further in June, with 210N low-end prices probing down to 1.16 yuan/piece, while 183 small-format wafers experienced the most pronounced price pressure.

Supply-Demand Summary:

The wafer market persistently faced a slight oversupply in H1 2026, with production fluctuating by rising first and then falling, while inventory underwent a process of "destocking—inventory buildup—divergent acceleration of inventory buildup." Production stayed high in January-February. In March, driven by an increase in calendar days and a demand boost from an export rush ahead of tax rebate cancellations, production schedules increased by roughly 10.71% MoM. In April, enterprises proactively cut production schedules by about 5.4%. May output was largely flat MoM. In June, the production schedule was expected to land in the 54-55 GW range, keeping overall supply slightly ahead of demand.

On the inventory side, a temporary destocking occurred in March, driven by high production schedules at downstream cell producers. From April onward, as production cuts at cell plants outpaced those at wafer plants, inventory began to rebuild. In June, due to sequentially weakening export orders and the pressure on exports from soaring ocean freight rates, the pace of inventory buildup accelerated. At the same time, production cuts at integrated enterprises and the concentration of toll processing orders further disrupted the pace at which supply and demand aligned.

Outlook:

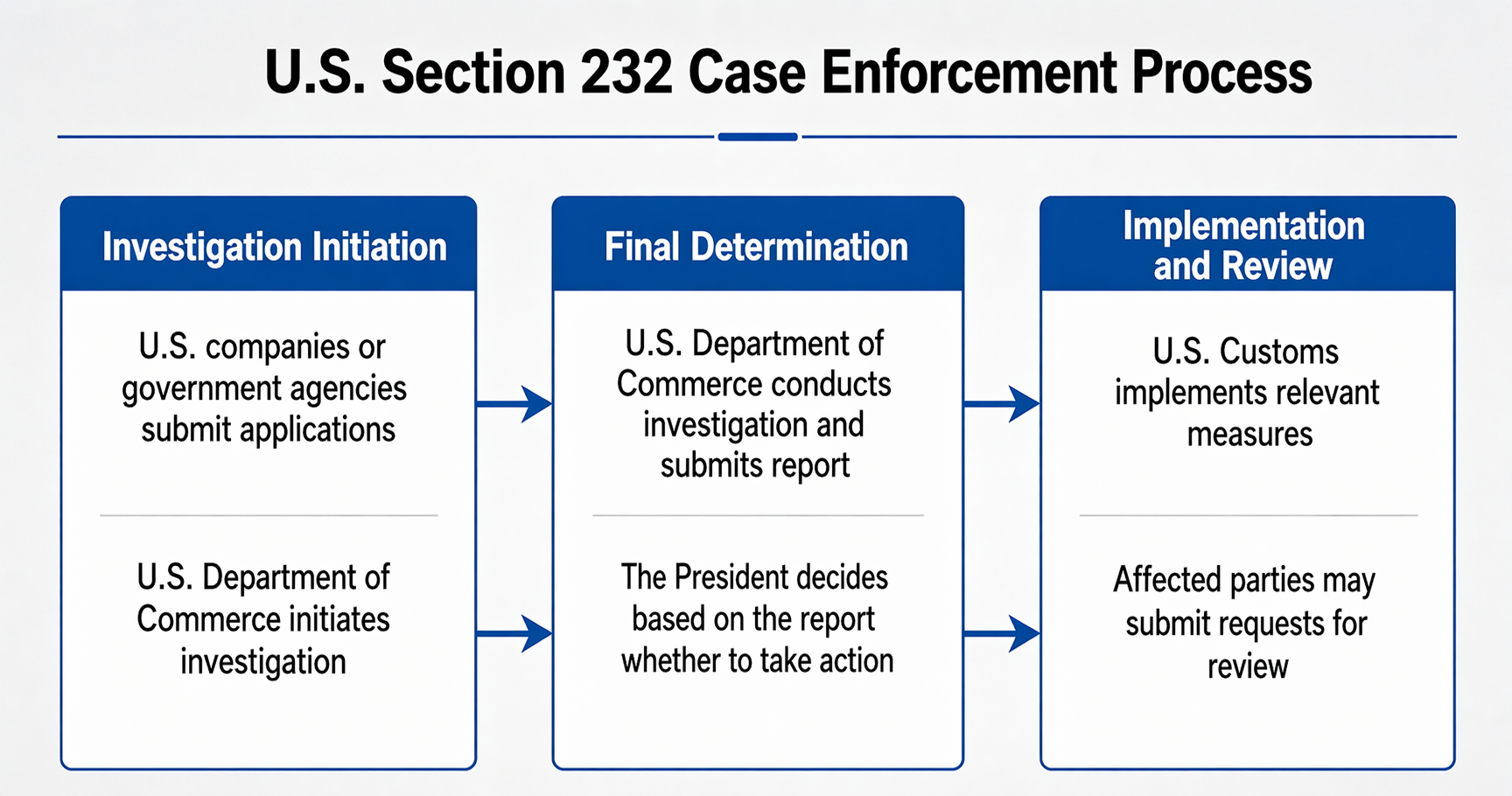

US Section 232

Since 2024, overcapacity and insufficient domestic demand have forced PV enterprises to go overseas and explore external markets. However, results have been poor. Field trips have revealed multiple obstacles hindering Chinese enterprises' expansion, including industry chain support, policy risks, and labour costs. The future model of pure export trade will change, and the path to earning overseas profits will shift towards joint ventures and building factories abroad.

In H2, a key focus will be the US Section 232. Section 232 of the US Trade Expansion Act of 1962 authorizes the Department of Commerce to investigate imports on national security grounds, with the President empowered to impose additional tariffs or set import quotas on foreign goods. We assess that this resides within the President’s authority. If he chooses to execute it this year, there will be two impacts:

1. China’s PV trade will be traced all the way back to the polysilicon stage, meaning traditional transshipment trade will theoretically become unworkable. Overseas polysilicon enterprises will no longer cooperate with origin laundering, and overseas polysilicon capacity will be dedicated to directly supplying US installations.

2. In the future, only regions with overseas wafer capacity will be eligible to participate in global trade. Chinese-funded enterprises in India and Southeast Asia will compete directly, while "laundered" capacity in Europe will shift to self-use.

The US is currently a country where PV products command excess returns. Taking local TOPCon modules as an example, their selling price is roughly 3-4 times the domestic China level. If domestic Chinese enterprises want to make a long-term overseas deployment, establishing joint ventures is likely the optimal choice, allowing them to escape the trap at home where scaling up only magnifies losses.

Tungsten Wire Diamond Wire Penetration Rate

As 18μm thin tungsten wire diamond wire achieves large-scale mass production, coupled with cost optimization brought by falling tungsten raw material prices, the advantages of using tungsten wire for cutting over traditional carbon steel diamond wire have been fully realized.

According to SMM model calculations, thanks to a smaller kerf that improves the number of wafers cut per kilogram of silicon ingot, 0.05 yuan in polysilicon cost can be saved per wafer. After deducting 0.03 yuan in extra diamond wire consumable costs, a net cost saving of 0.03 yuan per wafer remains, and a single GW of capacity can save nearly 2.96 million yuan in expenses. In an environment where PV wafer selling prices continue to fall and the industry has entered a phase of rivalry for existing capacity, the scope for compressing polysilicon costs is gradually narrowing. Refined management of non-silicon costs, exemplified by substituting tungsten wire diamond wire, serves as a crucial lever for producers to widen their profit margins and fend off price-driven involution. The substitution of carbon steel diamond wire with fine tungsten wire is already an unmistakable industry development trend.

Market-Driven Capacity Rationalization

We believe the average price bottom will occur in 2027, but the lowest point in terms of timing has already been reached recently. Differentiating from some market views, we do not believe the situation will become entirely desperate. Cash cost is the life-and-death red line. If prices fall below it, enterprises shut down; if they rise above it, they restart. Shutting down and staying below it for too long means they will not be able to restart. The paths for subsequent wafer capacity rationalization are limited to just the following: either local governments organize state-owned enterprises to acquire, technologically transform and upgrade plants, and then restart them; or foreign capital injects funds to revive the enterprises; or enterprises merge, where big fish eat little fish. The likelihood of outright bankruptcy is relatively small, as the residual value of wafer enterprise equipment remains very high.

Finally, we would also like to express a view: low-end capacity will not disappear as long as there is demand. PV enterprises that over-pursue new technology and advertise themselves as uniquely different are often the first to collapse when the tide goes out. This is just like the 18X product, which was launched in 2020 and continues to hold its share today—long-lived and enduring. In contrast, some technologies trumpeted over the past two years as being ahead of their time ultimately have not even survived half as long as this product.

![[SMM PV News] TCL Solar Debuts at Vietnam International PV and Energy Storage Exhibition 2026](https://imgqn.smm.cn/usercenter/HfeeS20251217171739.jpg)

![[SMM PV News] Central State-Owned Enterprises Ramp Up High-Efficiency Technology, AIKO Wins Bid for Datang's 4 GW BC Section PV Module Centralised Procurement](https://imgqn.smm.cn/usercenter/RGBgE20251217171739.jpg)