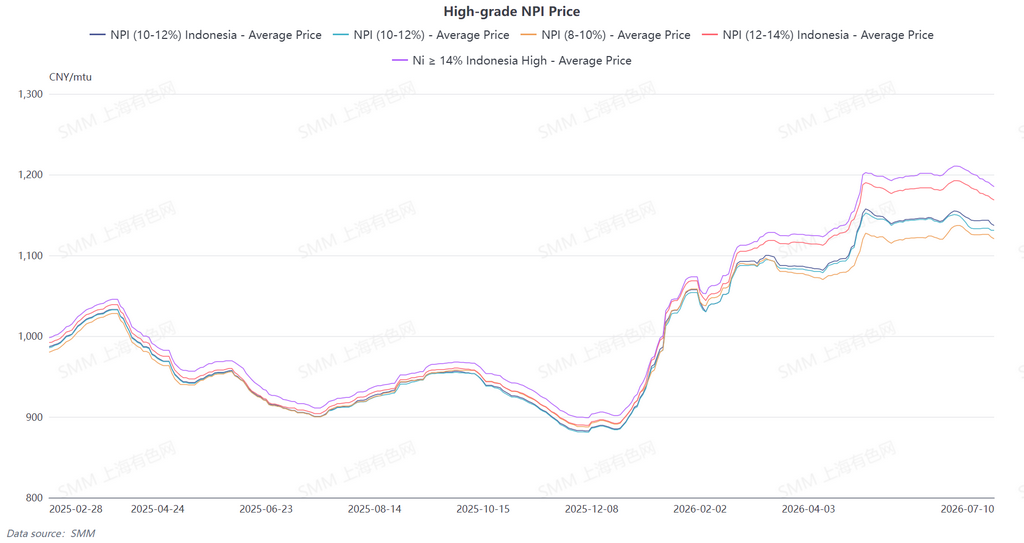

The SMM 10-12% high-grade NPI average price fell WoW by 1.2 yuan/nickel unit to 1,132.5 yuan/nickel unit (ex-factory, tax included), and the Indonesian NPI FOB index average price dropped WoW by $0.46/nickel unit to $146.23/nickel unit. Spot high-grade NPI remained on a downward trajectory this week, with the tug-of-war between longs and shorts intensifying further. Transactions stayed sluggish all week, and price divergences between upstream and downstream widened gradually.

Early in the week, a wait-and-see sentiment took hold, with only sporadic deals concluded. The price spread between different-grade cargoes continued to narrow, and both buyers and sellers were locked in a stalemate with strong wait-and-see sentiment. The futures market moved sideways, failing to spur a recovery in spot trades. In mid-week, bearish expectations further intensified. Downstream steel mills generally anticipated continued price weakness ahead, and their inclination to push for lower prices became more evident. Their procurement pace continued to slow. On the supply side, most sellers held their quotes stable and showed little willingness to adjust prices, intensifying the tug-of-war between supply and demand. In the latter half of the week, downstream demand for low-price purchases was released in a concentrated manner. Major steel mills issued low-price tenders and purchase orders, driving down the market's desired purchase prices accordingly. However, constrained by cost, upstream suppliers were reluctant to sell and lacked the motivation to offer substantial price concessions. The psychological price gap between upstream and downstream kept widening. Inquiries increased, but it was difficult to translate them into bulk transactions. Meanwhile, as the market weakened during the week, the scarcity premium on high-grade cargo was gradually eroded, and the price spread between high-grade and low-grade NPI narrowed. In the short term, the subdued and consolidative pattern is unlikely to change. Stainless steel demand in the off-season showed no signs of recovery, and downstream sentiment for pushing for lower prices persisted. Meanwhile, the bottom support from smelting costs remained firm, and suppliers showed a strong willingness to hold back from selling and hold prices firm. Downside room for prices is limited. Looking ahead, the market is expected to remain in a continuous tug-of-war between upstream and downstream, with price discrepancies difficult to narrow in the near term, spot transactions unlikely to see a significant volume increase, and overall prices consolidating on a weak note within a range.

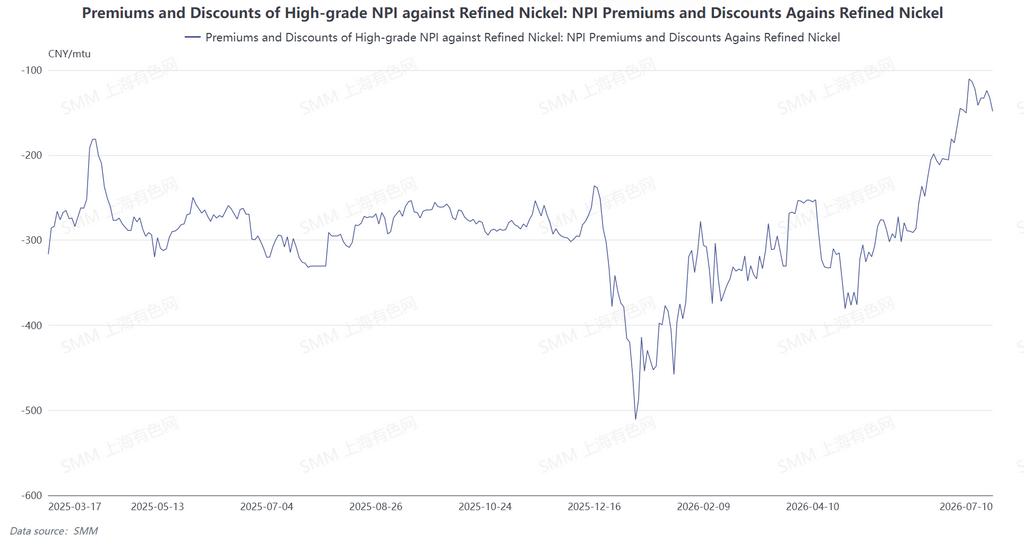

From the perspective of NPI-to-high-grade nickel matte conversion, the discount of high-grade NPI relative to refined nickel widened slightly this week. The change in the price spread was mainly driven by divergent price trends at both ends. On the one hand, the price center of refined nickel edged higher. On the other hand, high-grade NPI continued to be pressured by low tender prices from mainstream steel mills, with downstream buyers releasing concentrated low-price purchase orders, which pulled the spot price center of NPI across the market lower. As a result, the discount on high-grade NPI expanded, with the average discount relative to refined nickel widening slightly to 134.2 yuan per nickel unit. Looking ahead to next week, refined nickel prices are expected to pull back, while NPI, under downstream pressure, lacks sufficient momentum for price recovery. This may drive the discount of high-grade NPI relative to refined nickel to widen further, though the incentive for NPI-to-high-grade nickel matte conversion remains absent.

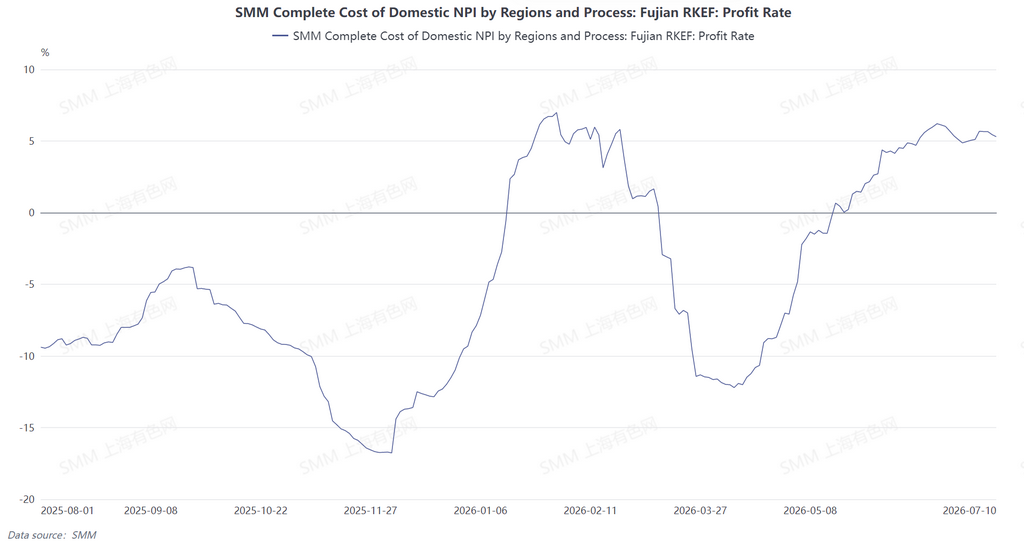

This week, prices of core nickel ore raw materials in China’s smelting sector remained stable, while fuel and auxiliary materials such as coking coal and coke weakened slightly. Overall smelting costs were largely steady with no notable fluctuations. In the Indonesia region, domestic nickel ore prices pulled back, and local smelters continued to increase the proportion of low-cost imported nickel ore. Even though fixed costs like electricity still exerted rigid pressure, the overall comprehensive production cost still had downside room. Smelter profits are expected to recover to some extent.