I. H1 Market Review

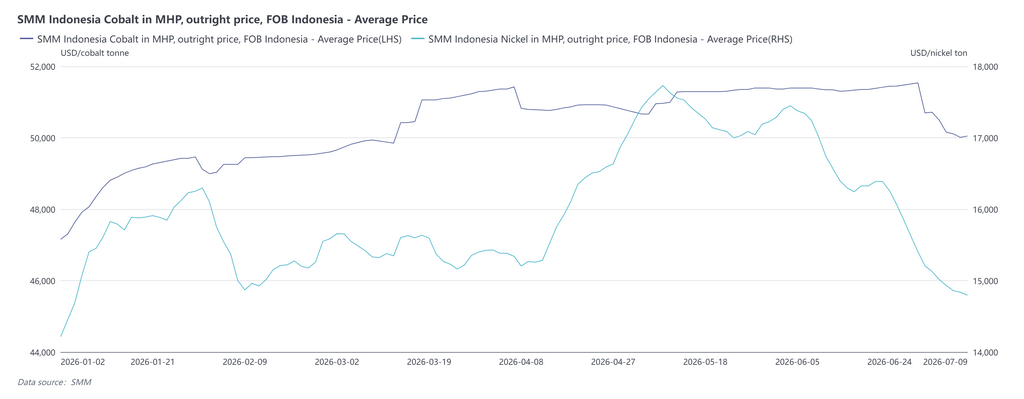

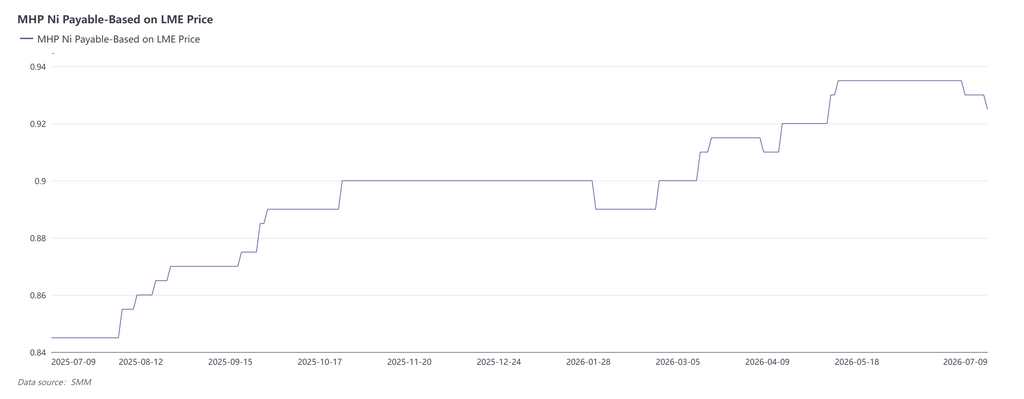

In H1 2026, the MHP market generally followed a logic of “continuously tightening supply and nickel and cobalt payables consolidating higher.” Nickel and cobalt payables rose steadily, only pulling back this month. Notably, the impact of the auxiliary material sulphur on MHP supply-demand gradually shifted from providing cost support to directly constraining supply, becoming a new core variable for the market this year. This article will review the MHP market in H1 from the supply-demand and cost perspectives and provide an outlook.

II. Supply Side: Macro disruptions combined with sudden accidents, causing continued production contraction

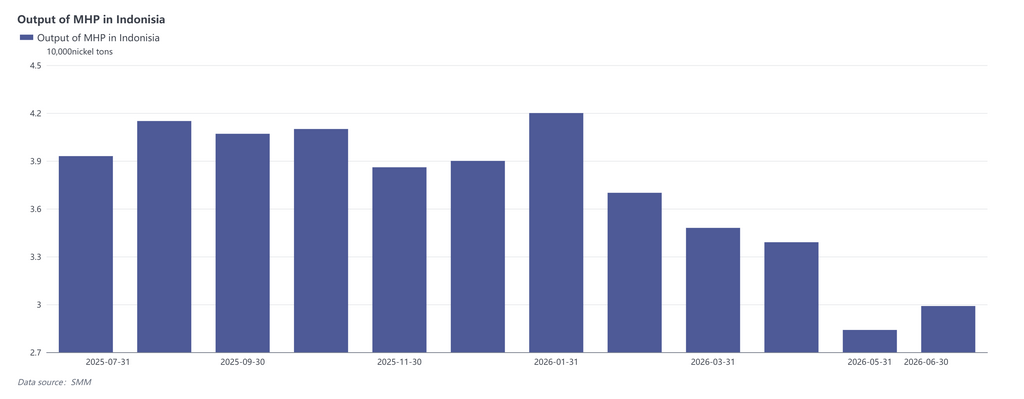

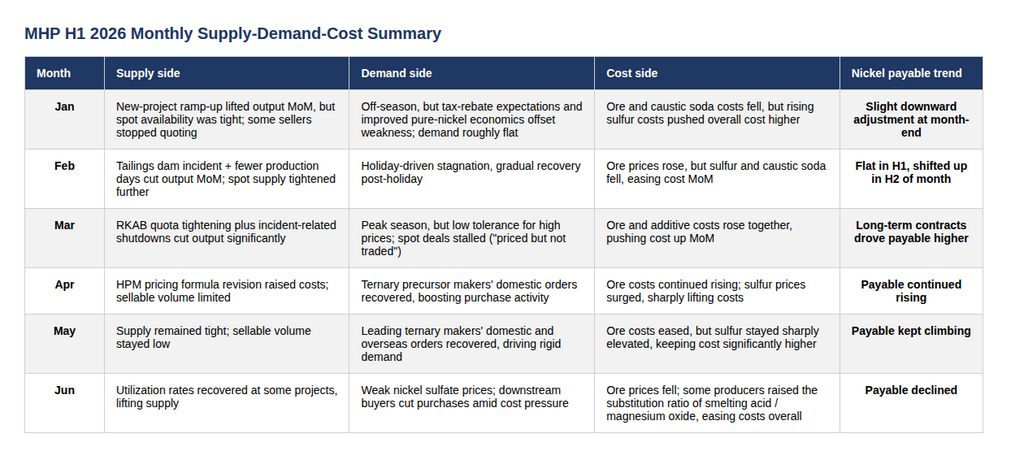

January was characterized by “coexistence of production ramp-up and tight spot cargo.” At some Indonesian MHP projects, production remained stable, while capacity ramp-up at new projects drove overall production upward; however, very limited spot cargo was available for sale, some sellers stopped quoting, and spot circulation was actually tight.

In February, production declined MoM, dragged down by a tailings dam accident and fewer production days. An accident at an Indonesian industrial park led to low-load operation of some MHP project lines; combined with fewer production days, output fell MoM, spot circulation tightened further, and some sellers held back from selling and ceased quoting.

From March, expectations of sulfur shortages and accident-related production stoppages reinforced one another, making supply contraction the central tension in the market. Accidents continued to affect production schedules at some projects, and together with the risk of sulfur supply disruptions, MHP production dropped markedly, keeping supply persistently tight.

From April to May, supply contraction continued, and available sellable volume stayed low. Indonesia’s revision of the HPM pricing formula pushed up costs for limonite ore; coupled with the persistent risk of sulfur supply disruptions, MHP production remained under pressure, sellable volumes held at low levels, and bargaining power in the market kept tilting toward sellers.

In June, the Middle East situation gradually eased, and production schedules at some projects rebounded. After the Strait of Hormuz reopened, expectations of tight sulfur supply were relieved to a degree, capacity utilization rates at some MHP projects recovered somewhat, providing supply-side growth.

III. Demand Side: Recovery in New Energy Orders Drives Payables Higher

Demand in January showed a "stronger-than-usual off-season" characteristic. Although January is traditionally an off-season for new energy, stockpiling ahead of the Chinese New Year and expectations of the removal of tax rebates for some new energy products in April prompted some downstream enterprises to increase their purchase willingness in advance. Meanwhile, high nickel prices improved the cost-competitiveness of refined nickel, leading to increased procurement demand from refined nickel plants. These two factors offset the off-season effect, keeping overall demand stable in January.

February was affected by the Chinese New Year holiday, with market trading following a pattern of "sluggish before the holiday, stagnant during, and recovering after." During the holiday, some nickel salt smelters suspended production, while operating enterprises mainly consumed inventory raw materials, with few transactions in the market. After the holiday, as downstream operations gradually resumed, market procurement and sales activity gradually recovered.

Although March entered the traditional peak season for new energy, insufficient acceptance of high prices led to "prices but no deals." Downstream procurement enthusiasm improved compared to pre-holiday levels, but was constrained by a slight decline in nickel sulphate prices, resulting in low acceptance of high-priced MHP by smelters. The psychological price gap between buyers and sellers continued to widen, making spot orders difficult to conclude, and the market fell into a stalemate.

From April to May, downstream orders continued to recover, and rigid procurement supported the rise in payables. From April to May, orders in China's ternary market continued to recover, generating rigid procurement demand, which boosted purchase willingness and drove MHP transaction payables steadily higher.

In June, the mid-year period saw weaker downstream procurement sentiment, and falling nickel and cobalt salt prices pressured MHP payables. At mid-year, downstream nickel salt and cobalt salt prices showed weakness, with significant losses pressures, making salt plants relatively less willing to accept high-priced MHP, thus weighing on MHP payables.

IV. Cost Side: Auxiliary Material Prices Dominated the Cost Curve, Sulphur Price Fluctuations Particularly Notable

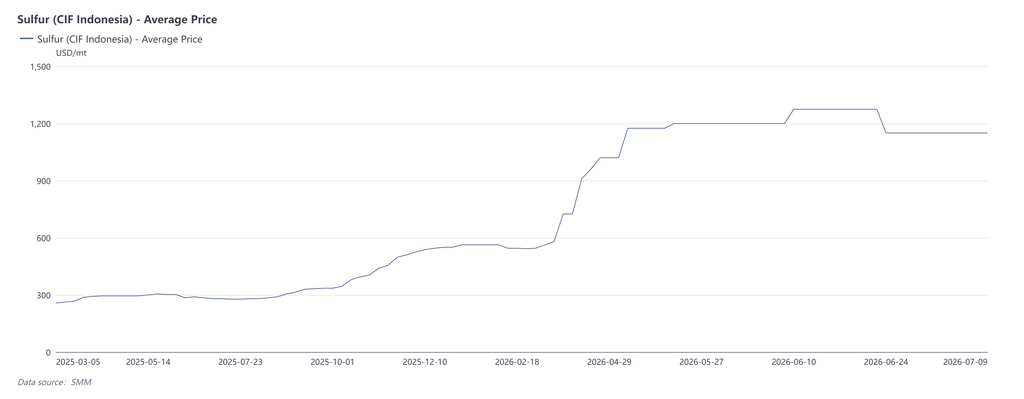

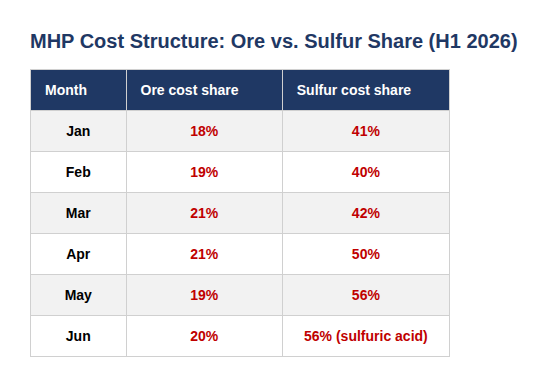

In H1, the total production cost of MHP exhibited a trend of "auxiliary material-led, high initially then moderating," with high volatility in auxiliary material prices standing in sharp contrast to relatively stable ore material costs: limonite ore prices moved sideways throughout the year, with the ore material cost share steadily staying within the 18%–21% range and having limited marginal disturbance to the cost curve. What truly dominated the cost trend were sulphur prices—their share climbed continuously from 41% in January to 56% in May-June, shifting cost pricing power from "ore-led" to "sulphur-led."

In terms of specific pace, sulphur prices were in a high-level standoff phase in January-February, and the cost trend was largely stable with slight fluctuations. From March, amid disturbances from the Middle East geopolitical situation, sulphur prices entered an accelerated upward channel, and unfolded into an "explosive" extreme market in April-May, driving the total production cost of MHP up significantly for two consecutive months and becoming the steepest phase of the cost curve in H1. In June, as the geopolitical premium quickly exited the market, coupled with some producers increasing the substitution ratio of smelting acid, magnesium oxide, etc. to hedge against rising sulphur prices, cost pressure only marginally eased and overall production cost pulled back somewhat. However, the share of sulphur (sulphuric acid) remained at a high level of 56%, indicating that the easing of cost pressure came more from the peaking and pullback of prices, rather than substantial cost reduction from structural substitution hedging.

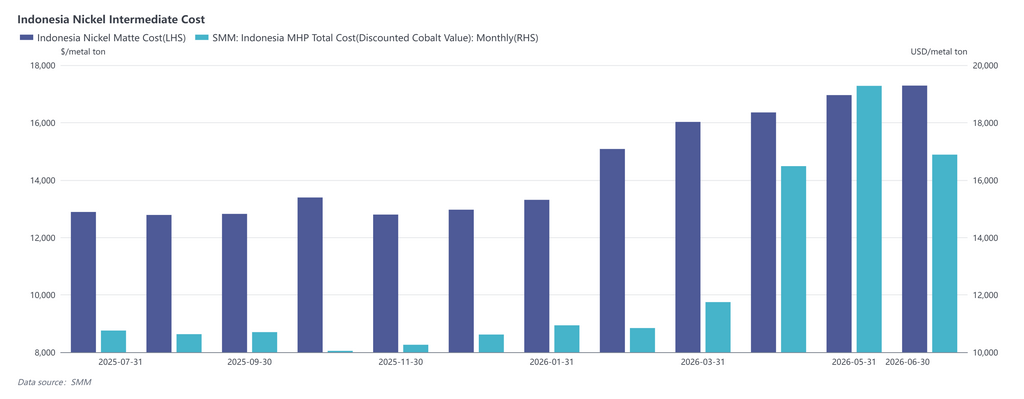

The rise in sulphur prices not only affected MHP supply itself; due to the substitutability among various raw materials in the nickel industry chain, the economic landscape between MHP and high-grade nickel matte was also reversed by sulphur: the production of high-grade nickel matte, with significantly lower sulphur consumption than MHP, saw its spot production cost temporarily lower than that of MHP in May. At current sulphur prices, for integrated enterprises producing nickel sulphate, MHP has become less economical than high-grade nickel matte.

V. Monthly Supply-Demand Cost Summary

VI. Market Outlook

For this year, starting from July, as existing hydrometallurgy intermediate product projects gradually resume production schedules and new projects are commissioned successively with capacity release, MHP supply is expected to see growth compared to H1. Full-year production is expected to reach 470,000–490,000 mt in metal content, up 6% YoY, with the supply growth factor under overall pressure. (Risk warning: This production forecast is based on a mild pullback in sulphur prices after Q3 arrivals, with MHP operating rates gradually recovering. Caution is needed for the risk that persistently high sulphur prices could prevent MHP project operating rates from rebounding.)

In the long term, as the sulphur issue is gradually resolved, Indonesian intermediate product project commissioning is expected to return to a normal pace. Indonesia’s intermediate product production is expected to rise to 700,000–800,000 mt in metal content in 2027, up over 50% YoY. Based on the growth scale of nickel sulphate demand, the new energy sector will struggle to fully absorb the MHP growth, putting the pricing factor under pressure. Meanwhile, future MHP surplus could put pressure on refined nickel inventories.

The reversal of this oversupply trend will rely on potential policy controls in the short term and on industry self-adjustment in the long term. Policy side, the core uncertainty for hydrometallurgy production schedules next year lies in Indonesian nickel ore quotas. Based on MHP production estimates for next year, an additional 30–40 million mt of nickel ore quota will be needed compared to this year. If the Indonesian government implements measures to control nickel ore quotas, it may reduce hydrometallurgy operating rates (or further squeeze out pyrometallurgy conversion supply). In addition, MHP also faces risks of additional taxation or export controls, which could similarly affect supply.

In terms of industry self-adjustment, first, the oversupply of hydrometallurgy may squeeze out pyrometallurgy. On one hand, MHP’s share in the raw material mix for nickel sulphate and refined nickel production may gradually increase, progressively squeezing out RKEF conversion to nickel matte. On the other hand, there is also substitution logic between NPI and refined nickel in the stainless steel sector. Second, in MHP production itself, there is also a cost curve. For example, differences in long-term sulphuric acid contracts, pipeline ore transportation, magnesium oxide, and tailings sulphur extraction may give some hydrometallurgy projects cost advantages. If nickel prices continue to decline in the future, it will force enterprises to undertake further reforms. Projects without sufficient CAPEX may further reduce operating rates, thereby reversing the MHP oversupply trend.