I. Operating Rate: Sharp Year-on-Year Decline; Extended Holidays Hamper Resumption of Production

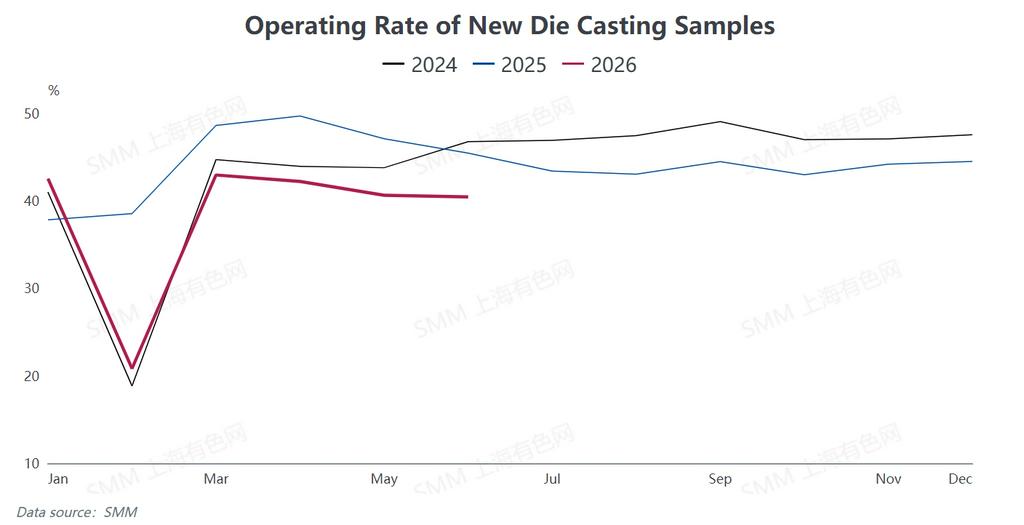

Per SMM statistics, the average operating rate of domestic die-casting zinc alloy manufacturers from January to June 2026 dropped by 6.25 percentage points year-on-year versus the same period in 2025, marking an evident slowdown in overall production activity.

Around the Spring Festival, zinc prices surged beyond expectations, stoking price aversion and wait-and-see sentiment among downstream end-users. As a result, industrial holiday durations were extended more than anticipated, with the average factory shutdown period hitting 23.5 days, 1.1 days longer year-on-year; some enterprises even suspended production for as long as 44 days.

The industry saw a sluggish overall resumption pace post-festival, with operating rates only recovering gradually after the Lantern Festival. The market briefly entered a seasonal peak in March, pushing the operating rate up to 51.8%, yet the upturn failed to sustain. Sustained high zinc prices dampened downstream purchasing willingness starting in April, driving consecutive declines in operating rates across May and June. The June operating rate settled at 40.46%, down a slight 0.18 percentage points month-on-month and 5 percentage points year-on-year.

Terminal demand displayed prominent structural divergence: orders from electronics and auto parts sectors remained relatively stable; demand for real estate hardware stayed persistently weak, weighing on overall rigid consumption; light industrial orders such as luggage and zippers featured distinct seasonal swings between off and peak seasons. Meanwhile, ongoing geopolitical tensions in the Middle East disrupted foreign trade, leading to a sustained slump in domestic hardware export orders destined for the region.

II. Cost and Profit: Raw Material Prices Stay Elevated, Alloy Process Fees Raised to Offset Risks

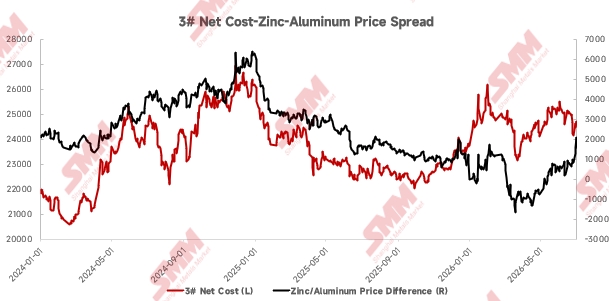

In the first half of 2026, prices of three base metals — zinc, aluminum and copper — remained at elevated levels, continuously lifting raw material costs for die-casting zinc alloy producers and triggering a periodic shrinkage of industrial profit margins. Cost pressures emerged prominently at the start of the year. The average monthly price spread between zinc and aluminum narrowed sharply from 1,144 yuan/ton in December last year to merely 140 yuan/ton in January. By the end of Q1, an extreme market scenario took shape where aluminum prices surpassed zinc prices temporarily. Copper prices also lingered steadily above 100,000 yuan/ton, further squeezing manufacturers’ earnings.

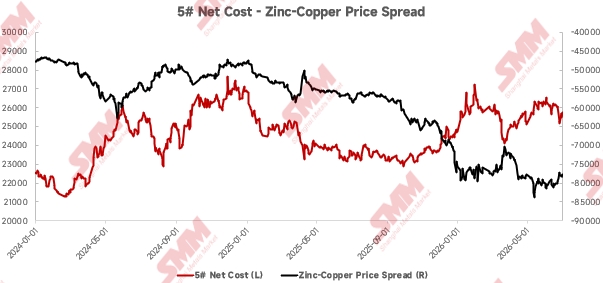

To offset losses stemming from expensive raw materials, domestic alloy smelters generally lifted processing fees to ease operational strains. As market conditions gradually recovered, the zinc-aluminum price spread rebounded to a monthly average of 209 yuan/ton in May, delivering a mild recovery in profit margins for 3# zinc alloy. In June, the zinc-copper price spread narrowed, yet marginal improvements appeared in profitability of 5# zinc alloy. Though overall industrial profit pressure eased slightly, earnings still stayed in a weak range on the whole.

III. Import & Export: Imports Keep Shrinking While Exports Surge

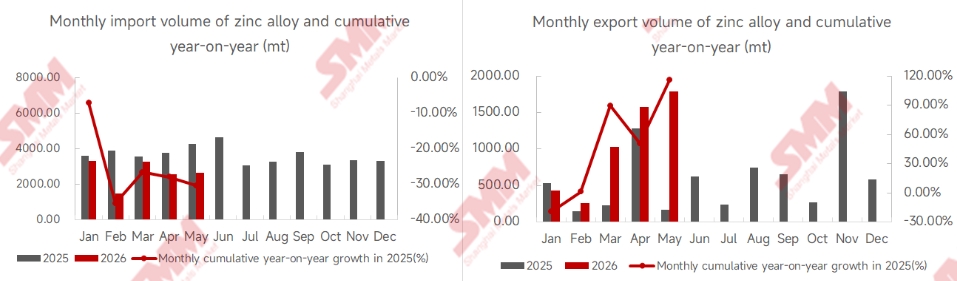

In the first half of 2026, the import and export of die-casting zinc alloys maintained a pattern of rising exports and falling imports. According to customs statistics, China’s cumulative imports of die-casting zinc alloys reached 13,259 tons from January to May, representing a year-on-year decline of 30.39%; cumulative exports stood at 5,088 tons, jumping sharply by 115.80% year-on-year.

Sustained capacity expansion and worsening overcapacity at domestic smelters have boosted substitution of imported alloys by domestic products, leading to a continuous slump in imports. On the export side, manufacturers benefited from price competitiveness driven by the weak Shanghai-London zinc ratio, alongside robust demand from emerging markets such as Southeast Asia. In May shipments, Taiwan region of China and Vietnam together accounted for nearly 88% of total exports, with Asia as a whole making up over 97%.

II. Outlook for the Second Half: Stable Fundamentals with Hidden Risks, Multiple Factors to Dictate Market Trends

Demand Side: Policy Support Yet Limited New Demand, Exports to Maintain Resilience

Looking ahead to the second half of 2026, end-user demand for domestic die-casting zinc alloys will follow a pattern of stable overall volume with structural divergence. Although successive property market stabilization policies have been rolled out, there is an obvious lag before policy effects filter through to construction hardware demand. Cumulative completed housing floor space fell 23.4% year-on-year as of May, leaving limited room for short-term demand recovery.

The automotive sector receives sustained backing from the vehicle replacement subsidy policy. However, lightweight upgrades for new energy vehicles have steadily cut zinc alloy consumption per vehicle, resulting in weak incremental support from this segment. The home appliance industry enjoys dual tailwinds of replacement subsidies and new purchase incentives, yet the fading subsidy effect has gradually weakened marginal demand stimulation.

From a seasonal perspective, June to August marks the traditional off-season with subdued overall demand. A cyclical demand rebound is expected in the September–October peak season, but overall domestic demand growth for the full year will remain modest. Compared with sluggish domestic consumption, exports, albeit small in volume, are set to be a major bright spot for annual demand. The persistently favorable Shanghai-London zinc ratio plus steady demand growth in overseas markets including Vietnam, China’s Taiwan region and Bangladesh will likely sustain sharp export growth of die-casting zinc alloys in the second half.

Supply Side: Severe Overcapacity to Persist, Industrial Consolidation to Accelerate

Supply-side pressure remains prominent as domestic smelters keep expanding die-casting zinc alloy capacity, leaving the industry saddled with persistent overcapacity. Private alloy manufacturers face mounting competition from low-cost alloy supplies released by smelters, driving a growing shift toward trading-oriented business models across the sector.

Dual headwinds of surplus capacity and stagnant domestic demand have created a paradox of cut-throat price competition alongside elevated raw material costs, exacerbating operational strains for small and medium private enterprises. Some manufacturers have pivoted to customized alloy production and differentiated operation to stay viable, yet the industry-wide overcapacity situation cannot be reversed in the short run, and industrial consolidation will speed up continuously.