I. Key Points

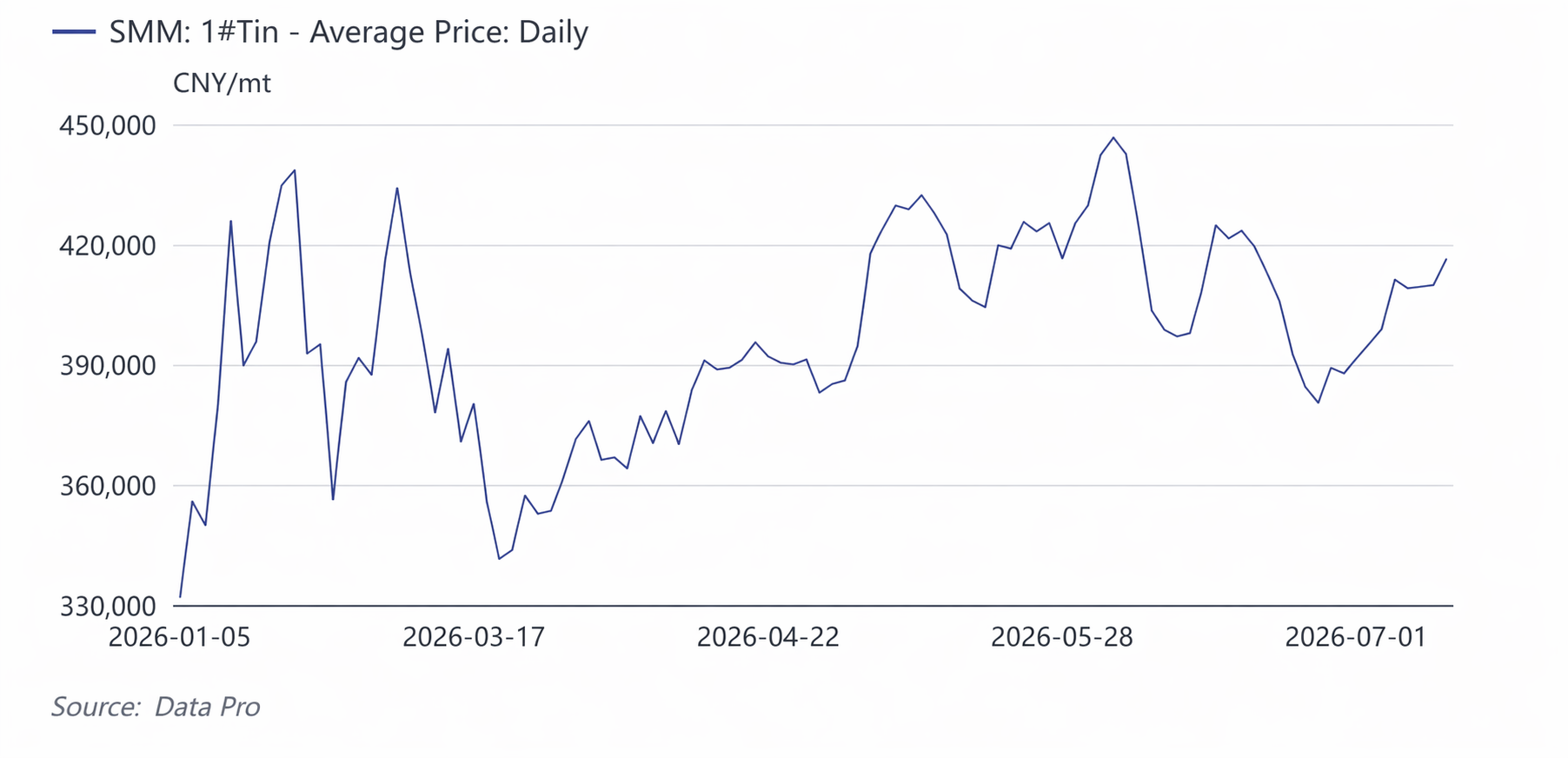

In H1 2026, tin prices exhibited a wide-range, see-saw pattern of “hitting historical highs — pulling back to consolidate — surging again — consolidating at highs”. The most-traded LME tin contract surged from about $42,000/mt at the beginning of the year to a historical high of $59,000/mt, pulled back to $40,500/mt in March, then surged again to near $58,000/mt in April-May, and retreated below $50,000/mt by end-June; the most-traded SHFE tin contract rose from 330,000 yuan/mt at the start of the year to a historical high of 470,000 yuan/mt, dipped to 322,600 yuan/mt in March, touched 451,000 yuan/mt again in early June, and pulled back below 400,000 yuan/mt by month-end.

The driving logic of this price cycle was the interweaving resonance of persistently below-expectation production resumption in Myanmar's Wa State, tightening of Indonesia's export policies, and geopolitical conflict in the DRC three supply-side mainlines with explosive AI computing power capex and semiconductor cycle recovery demand-side mainlines. The tin price center shifted systematically higher compared to 2025 — the average LME spot price in H1 was $50,291/mt, up 56.59% YoY; the average price of the most-traded SHFE tin contract was 396,000 yuan/mt, up 51.11% YoY. The tight-balance logic of “supply rigidity + AI-driven growth” , combined with low inventories, amplified price volatility.

Key tracking variables for H2 2026 tin prices: First, the pace of production resumption acceleration in Wa State after the rainy season (May-July) , and whether the Man Maw mining area can move from the current 40-50% of pre-ban levels toward 70%. Second, the implementation pace of Indonesia's annual RKAB approval , on the export data front, Indonesia's tin ingot exports in June 2026 amounted to 2,995 mt, up 5.09% MoM from May but down 32.55% YoY compared to the same period last year. Cumulative H1 data show that Indonesia's total tin ingot exports from January to June 2026 stood at 18,715 mt, a decrease of 25.14% YoY from 25,000 mt in the same period of 2025. Overall, while single-month exports in June extended the trend of modest MoM recovery, total H1 exports still contracted significantly compared to the same period last year. Third, whether capex on AI servers, advanced packaging, and optical modules can continue to materialize, as global tin demand from AI in 2026 is approximately 12,000-15,000 mt, accounting for only 3-4% of the global consumption of 370,000 mt, but virtually all incremental demand comes from AI. Fourth, whether global visible inventory can break out of the low-range level . Under a neutral scenario, LME tin is expected to trade in a range of $50,000-$56,000/mt in H2, with SHFE tin at 380,000-440,000 yuan/mt .

2. Macro Environment – Liquidity Reversal, Geopolitical Shock, and Revaluation of “Compute Metal”

1. US Fed “From Dove to Hawk,” Warsh Nomination Reverses Easing Expectations

At the start of the year, the market was betting on 50–100bp rate cuts in H1 2026, the US dollar index fell below 97, and the non-ferrous metals sector broadly rose. At end-January Warsh was nominated as Fed Chairman , driving the US dollar to bottom out and base metals to collectively pull back. Tin prices began their first deep correction from 470,000 to 320,000. The June dot plot leaned hawkish, the logic of “easing realization” was systematically revised, and with rate hike fears, tin prices pulled back again in June from 450,000 to below 400,000.

2. Middle East Geopolitics Extends from “Safe-Haven Trade” to “Physical Shipping Impact”

In March, the US-Israel joint military strike on Iran and disturbances in the Strait of Hormuz not only pushed up energy premiums but, more directly for tin, was the disruption of the Indonesia-Europe refined tin shipping route . After the mid-June US-Iran ceasefire, energy and safe-haven premiums faded, and tin prices simultaneously peaked and pulled back.

3. RMB “Two Strengths” + US Adding Tin to Critical Minerals List

The onshore RMB rose from 6.98 to 6.79, reducing import costs and opening a window, but the domestic challenge for tin was not import shocks (Indonesia’s exports were already halved) but the US’s 2026 push for tin supply chain independence – as a member of the US critical minerals list, tin was included in the “strategic resource revaluation” narrative, enjoying capital premiums alongside copper and nickel.

3. Industrial Policy – Wa State’s “More Bark Than Bite” and Indonesia’s “Resource Nationalism” Dual Tightening

1. Myanmar’s Wa State: “Triple Shackles” of Output Resumption After Mining Ban

Wa State banned mining in August 2023 and didn’t issue extraction permits until July 2025, but actual output resumption was far below expectations , with capacity currently restored to only 40–50% of pre-ban levels:

- Physical Shackle : Deep mine tunnels were severely flooded; water pumping cost sharing was officially implemented in March 2026, and low-altitude, high-grade mining areas slowly reached full production;

- Institutional Shackle : Exports were shifted to a 30% in-kind tax replacing cash tax; some ore was retained for local smelting, reducing incremental flows to China. In January-April, although physical imports reached 69,100 mt, up 88% YoY (low base effect), the metal-equivalent amount was only 22,500 mt, up 36% YoY, with minimal MoM growth;

- Unforeseen Shackle : A massive explosion at the Bangkang explosives factory in Wa State on April 7 led to suspensions and rectifications at all chemical/explosives plants in the state, cutting off civilian explosives supply. Coupled with restricted open-pit mining and road transport during the traditional rainy season from May to July, no large-scale growth is expected before August .

2. Indonesia: From RKAB Term Shortening to Windfall Tax, Refined Tin Exports "Halved"

Indonesia, the world's largest refined tin exporter, saw a flurry of policy packages in 2026:

- The RKAB approval was changed back from a three-year to an annual cycle, and quotas for some enterprises for 2026 were revoked and re-reviewed, sending export uncertainty surging;

- refined tin exports in April were just 2,255 mt, down 53.7% YoY and halved MoM, mainly due to permit renewals, tighter quotas, and industry rectification;

3. DRC's Bisie Mine: The "Long-Tail Shortfall" from Armed Conflict

Bisie accounts for about 6% of global supply. After the shutdown in March 2025 due to armed conflict, output was not fully recovered for the whole year, and early 2026 landslides plus geopolitical setbacks created a third disruption on the supply side.

4. Raw Material Chain: Cost Transmission from Tin Concentrates → Refined Tin → Solder

1. Tin Concentrates: TCs Rebound, but "Marginal Easing" Does Not Equal "Easing"

In H1 2026, domestic tin concentrate TCs were cumulatively raised by 5,500 yuan/mt, a confirmation of marginal improvement in raw materials at the price level, yet domestic ore itself showed no growth, easing outside China fell short of expectations, and no significant easing was seen at the ingot end.

- The import structure has shifted structurally: in 2022, Myanmar accounted for 77% of China's tin concentrate imports, which dropped to 26% in 2025, while DRC rose to 24%, Australia 12%, and Bolivia 10% – diversification mitigated supply disruptions, but the absolute volume could not fill the gap left by Myanmar.

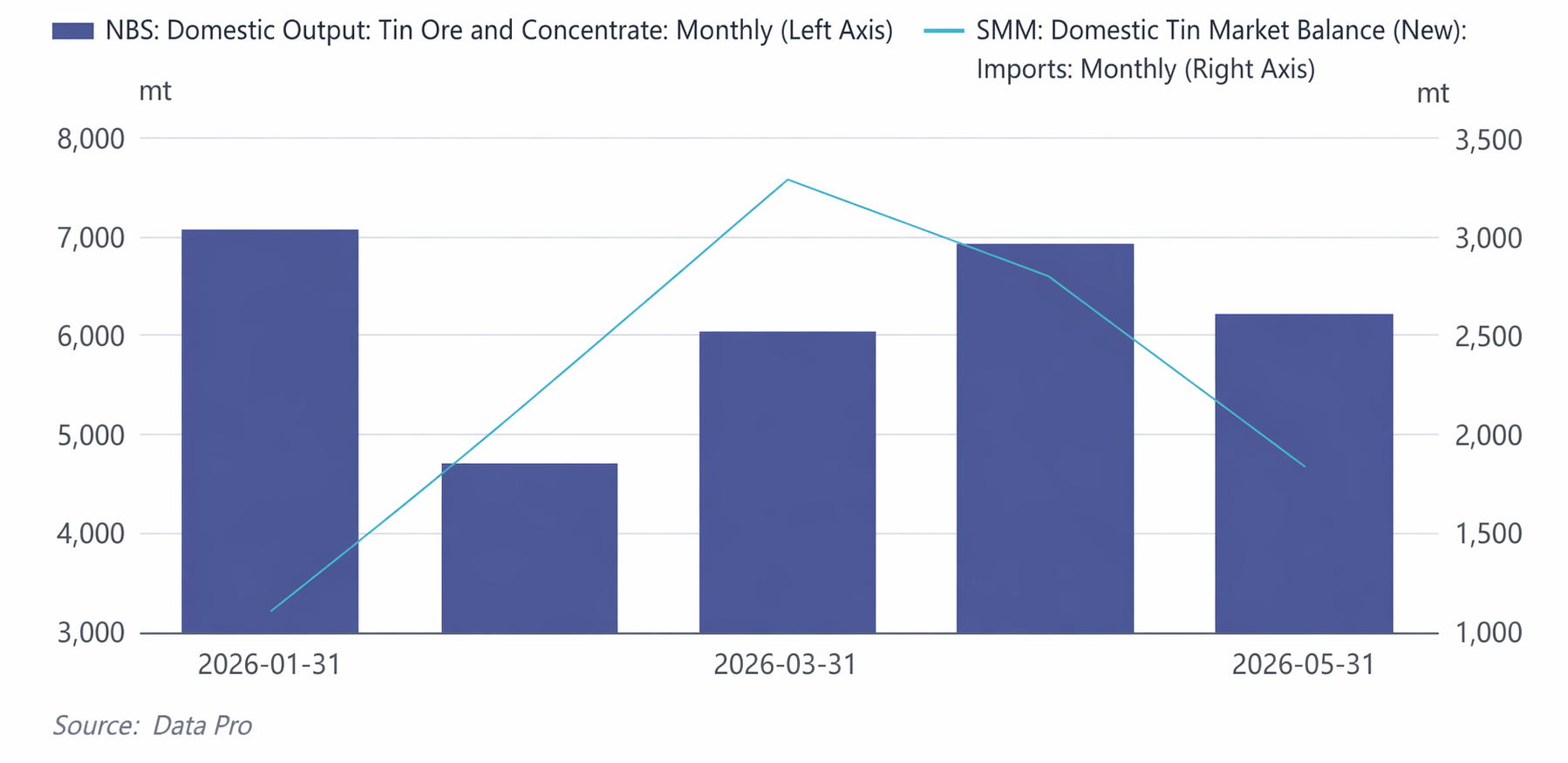

- Domestic Tin Ore: from January to May, cumulative domestic tin ore and concentrate production was about 30,600 mt, averaging about 6,187 mt per month. January's output of 7,062 mt was the peak for the period, February plunged to 4,708 mt (down 33.3% MoM) due to Chinese New Year, and March to May gradually recovered to the 6,000–7,000 mt range.

- Tin Ingot Imports: January imports were only 1,101 mt (the year's low), climbed to 3,287 mt in March (the year's peak), then pulled back to 2,802 mt and 1,838 mt in April and May. Cumulative imports from January to May were about 11,200 mt, averaging about 2,239 mt per month.

Tight Balance at the Mine End: domestic ore production growth was limited, and imports fell back from the March peak, resulting in total mine-side supply in May of about 8,049 mt (domestic + imports). The overall pattern was one of "domestic ore rising steadily, with volatile import supplements," and the tightness at the mine end provided bottom support for tin prices.

2. Refined Tin Production: In H1, SMM's cumulative refined tin production was approximately 86,800 mt.

In February, production dropped to 11,490 mt due to Chinese New Year maintenance (the H1 low), then quickly rebounded to 14,950 mt from March. From April to June, it stabilized in the range of 14,670-15,430 mt, with June posting the H1 high of 15,430 mt, demonstrating that smelters maintained high production enthusiasm despite tight raw material supply.

- Recycled Tin Proportion: Cumulative production of recycled refined tin from January to June was about 17,200 mt, accounting for around 19.8% of total output. In February, recycled tin was only 1,770 mt (affected by the Chinese New Year shutdown), gradually recovering to 3,000-3,220 mt from May to June. The supply elasticity of recycled material was limited.

- Operating Rate: The average operating rate of smelters pulled back from 62.7% in January to 47.7% in February (Chinese New Year), then remained in the 54.3%-57.1% range from March to June, recovering to 57.1% in June. The overall operating rate was at the industry mid-level, reflecting the constraint of tight ore supply on the release of smelting capacity.

3. Solder/Tin Chemicals: The 'Hidden Consumption' of the AI Computing Power Chain

Traditional solder (PCB, home appliances, automotive) demand was stable but weak, whileAI servers consume over four times more tin per unit than traditional servers, with tin consumed in every link from advanced packaging to optical module solder joints. In 2026, AI-related tin demand is 12,000-15,000 mt, while tin used in PV underwent adjustment, and semiconductor solder demand resilience remained.

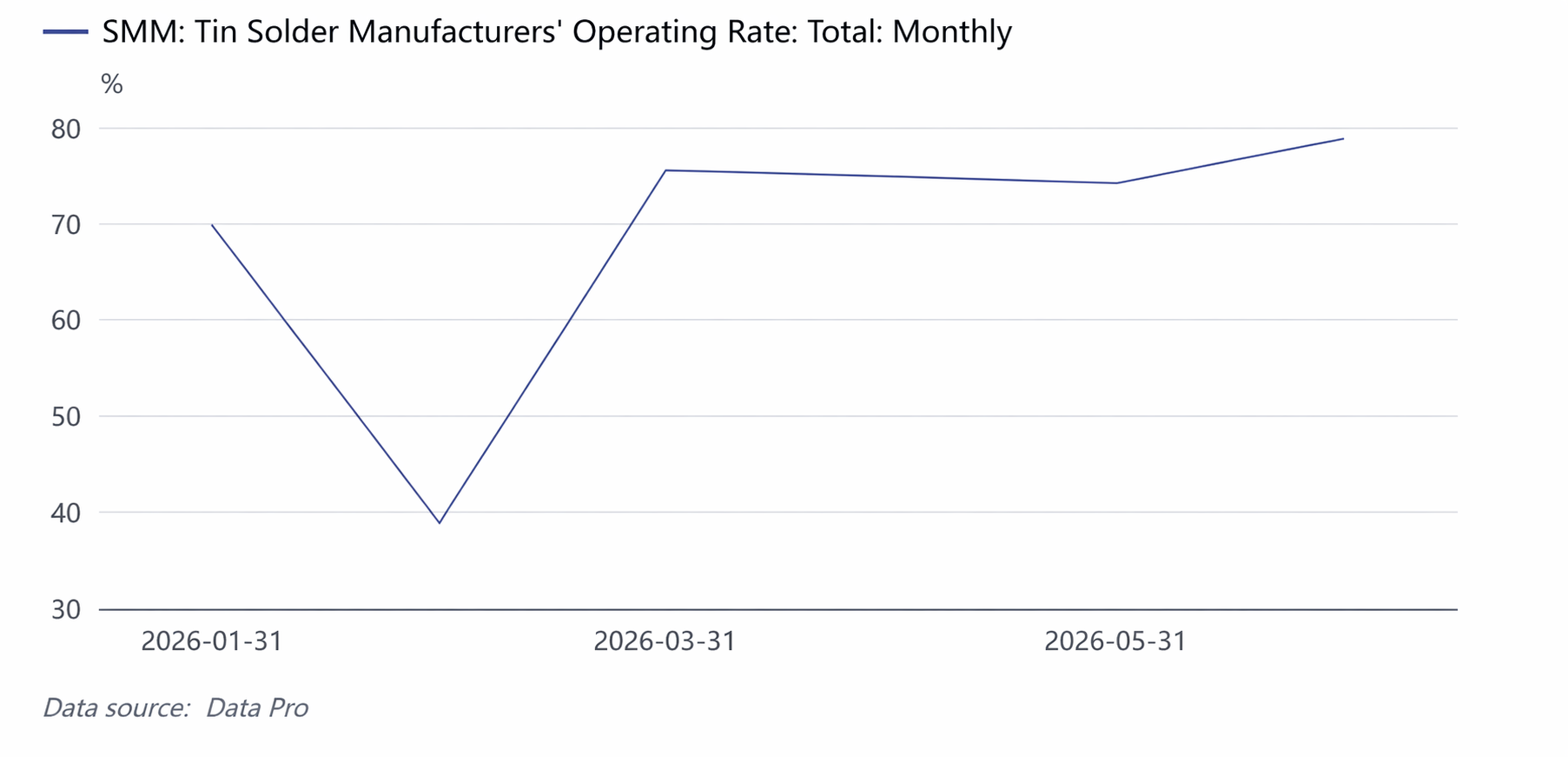

Solder Operating Rate as a Key Tin Consumption Indicator: Tin solder consumption accounts for over 60% of China's total refined tin consumption, directly reflecting the actual demand strength from downstream end-use sectors such as electronics and PV.

- Performance Characteristics: The operating rate was 69.7% in January (driven by pre-Chinese New Year stockpiling), plunged to 39.0% in February (Chinese New Year break + high tin prices curbed purchases), rebounded strongly to 75.5% in March (post-holiday restocking), remained in the high range of 74.2%-74.9% from April to May, and climbed further to 78.8% in June, hitting the H1 peak.

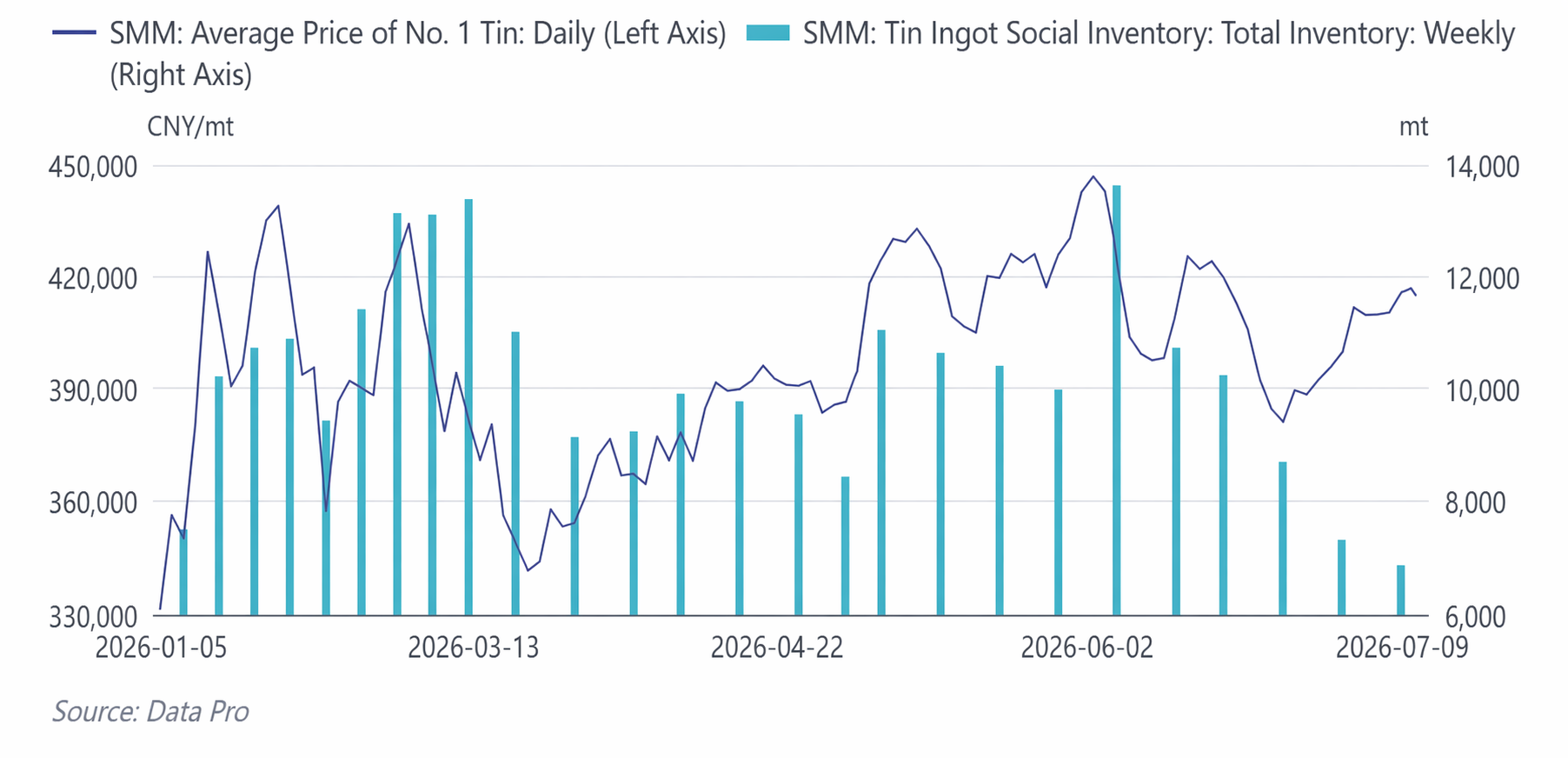

- Key Signal: In June, the solder operating rate bucked the trend and climbed to 78.8%, while the source price pulled back from the high of 446,700 yuan/mt, significantly increasing downstream dip-buying willingness. This was highly consistent with the rapid destocking of tin ingot social inventory from 13,604 mt to 6,861 mt during the same period, confirming the industry chain transmission link of 'price correction → downstream restocking → accelerated inventory digestion'.

V. H2 2026 Risk Warnings and Tin Price Forecast

In H2, tin prices are expected to maintain a pattern of'supply game dominance, AI amplifying elasticity, and low inventories underpinning', with key focuses on: ① accelerating production resumption in Wa State after the August rainy season; ② the implementation strength of Indonesia's RKAB; ③ Q3 AI capex guidance (Microsoft/Google/Meta earnings reports); ④ production status at Bisie in DRC; ⑤ whether global visible inventory can accumulate.

Scenario-based analysis:

|

Scenario |

Trigger Conditions |

LME Tin Range ($/mt) |

SHFE Tin Range (10,000 yuan/mt) |

|---|---|---|---|

|

Bearish |

Wa State's accelerated production resumptions + Indonesia's quota relaxation + AI capex downgrade + macro hawkishness |

$47,000—51,000 |

36—40 |

|

Neutral(highest probability) |

Wa State mild production resumptions + AI sustaining high growth + low inventory |

$50,000—56,000 |

38—44 |

|

Bullish |

Post-rainy season further delay in Wa State + DRC disruptions + AI exceeding expectations + inventory destocking |

$54,000—60,000 |

42—47 |

In terms of pace, in Q3, just after the rainy season in Wa State, production resumption data will be intensively verified, making it the most critical pricing window of the year; in Q4, entering the AI new product release cycle, the price center is expected to retest the H1 highs. From the full-year balance sheet perspective, SMM expects a global refined tin deficit of approximately 5,100 mt—tight balance + low inventory + AI, tin's pricing logic has shifted from a "non-ferrous metals follower" to a "computing power metal frontrunner".

![Tightening expectations outside China have softened somewhat, the most-traded SHFE tin contract is consolidating around 416,000 [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/XUPwI20251217171751.jpg)