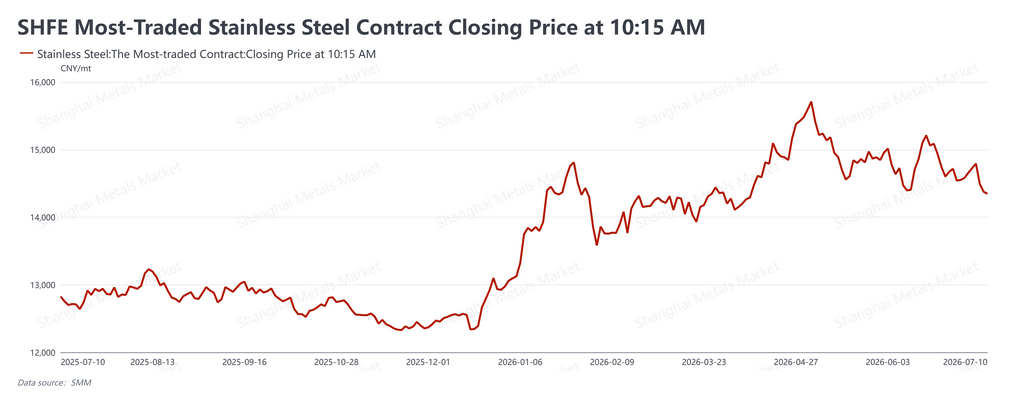

China's stainless steel futures fell sharply this week, breaking a recent range-bound pattern as weakness in nickel prices and soft demand from the traditional summer off-season combined to push the market lower. The benchmark contract settled at RMB 14,345/mt (approximately $2,116/mt) on July 10, down RMB 310/mt (about $46/mt), or 2.11%, from the prior Friday's close of RMB 14,655/mt (approximately $2,162/mt). The contract closed below the closely watched RMB 14,500/mt (about $2,139/mt) level on three consecutive sessions from Wednesday onward and failed to recover it. The week's defining feature was a widening gap between futures and spot: futures tracked nickel lower, while spot prices held up much better, supported by mills defending their sales prices and low social inventories.

Macro signals were mixed and offered only partial offset

Overseas, sentiment stayed cautious but directionally unclear. Minutes from the US Federal Reserve's latest meeting showed a small minority of officials still saw a case for a June rate hike, though most favored holding rates steady, with a leaning toward dropping the "easing bias" language from the policy statement — reflecting real division over the path ahead. Fed Governor Christopher Waller argued that forward guidance isn't necessarily better when there's more of it, and said inflation risk now outweighs employment risk. European Central Bank Governing Council member Mullen said inflation has retreated following the recent oil price slide, putting the ECB in a "favorable position" after its last hike. The IMF trimmed its global growth forecast while raising its China outlook, and US trade data showed the May deficit widening to its largest in over a year on broad import growth and softer exports.

Domestically, China's June CPI rose 1.0% year-on-year and PPI rose 4.1%. The full RMB 200 billion allocation for the "two new" equipment-upgrade program has now been disbursed. The June RatingDog services PMI came in at 54.1, down 0.3 points but still marking 42 consecutive months of expansion. The People's Bank of China launched a RMB 1 trillion reverse repo operation on July 6, ending three straight months of net liquidity contraction. These domestic signals leaned supportive but weren't enough to offset the direct drag from falling nickel prices on the futures market.

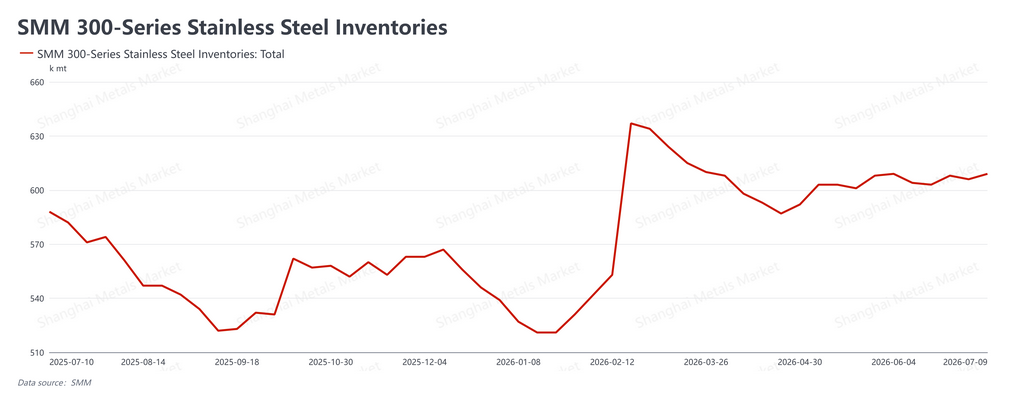

Destocking stalled, but spot prices held their ground

SMM's tracked social inventory came in at 943,700 mt this week, up roughly 8,300 mt from the prior reading of 935,400 mt on July 2. Destocking has stalled and turned into a mild build, though the increase is modest and absolute inventory remains at a relatively low level, limiting the pressure on spot prices for now.

Spot resilience this week rested on three factors. First, mills have kept a firm hand on ex-works pricing, which has capped the volume of material reaching the market and kept actual supply pressure limited. Second, traders have mostly been drawing down their own inventories to sell rather than dumping stock at discounts, so no panic selling has emerged. Third, while downstream buyers remain cautious and are largely purchasing on an as-needed basis, routine restocking demand has held up reasonably well, and news of planned maintenance and output cuts at mills has reinforced the firmer spot tone.

That said, the broader picture is still soft. The market has fully entered its traditional low season, end-user demand is naturally weak, and the ongoing futures slide has dented trading confidence — keeping overall transaction volumes thin. This remains the key bearish factor in the fundamentals.

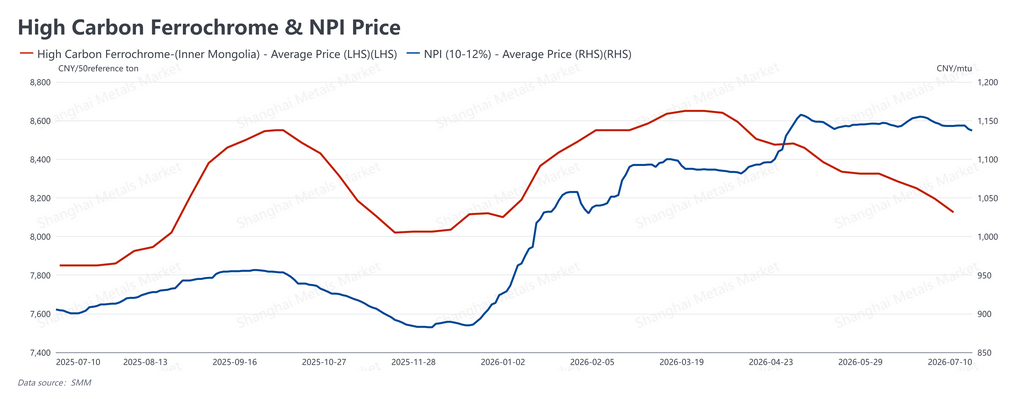

Raw material costs eased, lifting mill margins

Nickel Pig Iron (NPI) prices came in at RMB 1,131/nickel point (about $167/nickel point) this week, down slightly from RMB 1,133/nickel point (about $167/nickel point) the prior week. High-carbon ferrochrome held at RMB 8,100/50mt basis ton (about $1,195) for the entire week, down RMB 25 (about $4) from RMB 8,125/50mt basis ton (about $1,198) previously.

Raw material prices fell faster than finished product prices, improving the cost-price spread. Combined with spot prices holding firm on mill support, this widened smelting margins across the sector this week, a modest improvement in the profitability environment. That, in turn, is providing some support for current production schedules, and there's no clear sign yet of supply tightening in the near term.

Outlook

This week's market showed a two-sided pattern: mixed macro signals and falling nickel prices pushed futures through a key support level, while mill price discipline, low inventories, and maintenance-related supply expectations kept spot prices propped up — widening the futures-spot gap. Looking ahead, the key variables are whether the deepening off-season will further erode end-user demand and whether nickel prices can find a floor; both will determine how long spot support can hold. If downstream buying weakens further or inventory builds accelerate, the resilience in spot pricing could come under pressure. The futures contract is likely to stay in a weak, range-bound pattern in the near term, with the support zone having shifted lower following this week's break. Industry clients are advised to weigh macro-driven volatility rationally, watch off-season spot transaction volumes and actual inventory digestion closely, be cautious about chasing moves in either direction, and maintain a steady operating stance.