This week, iron ore prices rebounded from lows, but fundamentals continued to weaken. Global shipments and port arrivals both edged up, while the decline in hot metal production widened, weakening demand-side support. Market rumors of a BHP union strike, coupled with renewed tensions in the Middle East, pushed up crude oil prices and ocean freight rates, jointly driving the most-traded iron ore futures contract to drift higher. However, narrowing profit margins at steel mills, subdued purchasing enthusiasm, and potential environmental protection-driven production restrictions in mid-July led mills to primarily restock as needed, with a strong desire to push for lower prices. This caused spot prices to underperform futures. On port spot cargoes, the weekly average of the MMI 61% index fell slightly below last week's level.

Chart: MMI 61% Port Spot Index

Source: SMM

This week, domestic iron ore concentrate prices edged down. By region, prices in Tangshan, Qian'an, and Qianxi in Hebei were relatively stable; Chaoyang, Beipiao, and Jianping in western Liaoning were also relatively stable; and east China rose by 1-5 yuan/mt. Tangshan area iron ore concentrate prices were relatively stable, with 66% grade concentrate delivered on a dry basis, tax included, at 970-980 yuan/mt. Overall production in the Tangshan area was relatively stable, with mines and beneficiation plants mostly operating as planned; the Chengde domestic ore market saw generally average trading, with tight raw ore availability, constrained producer operations, overall low operating rates, tight spot supply, and strong sentiment among holders to hold prices firm and hold back from selling. Other regions mostly operated as planned. On the demand side, steel mills mostly continued purchasing as needed, overall market transactions were relatively sluggish, and sellers and buyers remained in a tug-of-war.

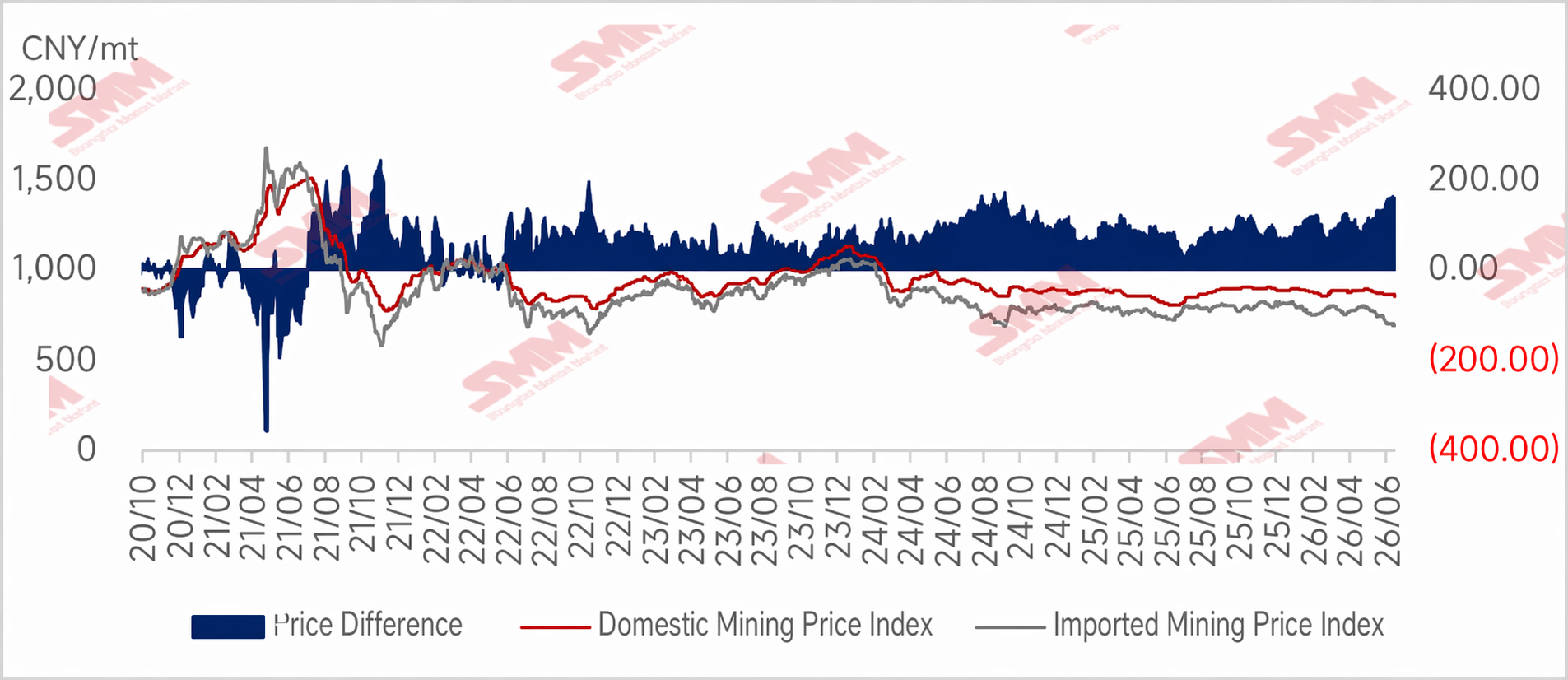

Chart: Domestic Ore Supply Remains Weak; Domestic-Imported Ore Price Spread Stays High

Outlook for Next Week

Imported ore: Looking ahead to next week, iron ore fundamentals are expected to remain weak, with hot metal production having some room to edge down further while supply remains high. The supply-demand gap may widen further, and port inventories face inventory buildup pressure, weighing on ore prices. However, next week marks a critical verification period for several major rumors, and market uncertainty is strong. With bullish and bearish factors interwoven, iron ore prices are expected to move sideways.

Domestic ore: Looking ahead to next week, China's iron ore concentrate prices are expected to remain tight, with the domestic fundamental landscape difficult to change. At steel mills, overall blast furnace hot metal production is estimated to trend lower, weakening support for iron ore concentrate demand. Overall, domestic concentrate prices are expected to be in the doldrums in the short term.

![Limited Short-Term Upside and Downside for Ferrous Metals [SMM Steel Industry Chain Weekly]](https://imgqn.smm.cn/usercenter/MXbup20251217171745.jpg)