SMM, July 10:

I. PV-grade EVA Resin: A Complete "Roller Coaster" Market

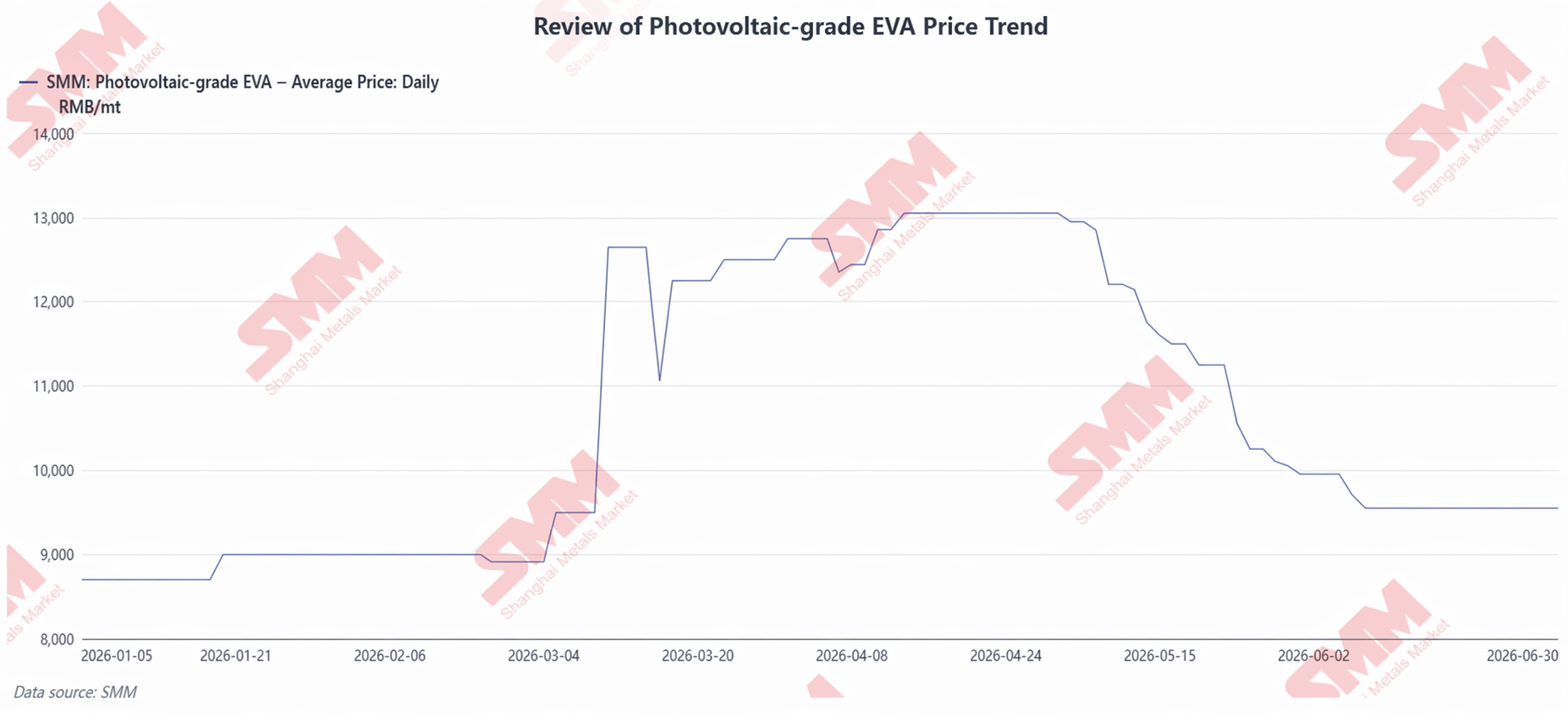

In H1 2026, PV-grade EVA resin prices went through a full cycle of "moving sideways at lows – surging on impulse – consolidating at highs – accelerating declines – hitting bottom and stabilizing," with swings exceeding 50%.

1. Price Trend

At the beginning of the year, PV-grade EVA resin prices hovered in a low range of 8,700-9,000 yuan/mt. Petrochemical plants faced high inventory pressure, and the industry was in a loss-making or low-profit situation. Downstream film producers mainly worked through earlier raw material stockpiles, and their procurement pace was cautious. The export rush window opened just before the removal of export tax rebates took effect in March. China's module scheduled production surged from 27.19 GW in February to 36.46 GW, boosting film scheduled production, and resin prices were quickly pushed from 9,000 yuan/mt to 12,650 yuan/mt, an extremely rapid rise. In April, resin prices consolidated at highs of 12,250-13,050 yuan/mt, and mid-month prices hit the H1 peak. Entering May, the module export rush window officially closed, end-user scheduled production pulled back sharply, film raw material demand weakened quickly, and industry resin inventory continued to build. Additionally, with the easing of US-Iran tensions, international crude oil prices declined noticeably, and the cost support for EVA raw materials weakened, pushing resin prices into a sustained downward trajectory. In June, as petrochemical plants proactively controlled production to support prices, and downstream film producers' essential restocking demand continued to materialize, industry inventory destocked steadily. The earlier high inventory pressure was clearly alleviated, and PV-grade EVA prices stopped falling and stabilized around 9,550 yuan/mt.

2. Supply-Demand Pattern

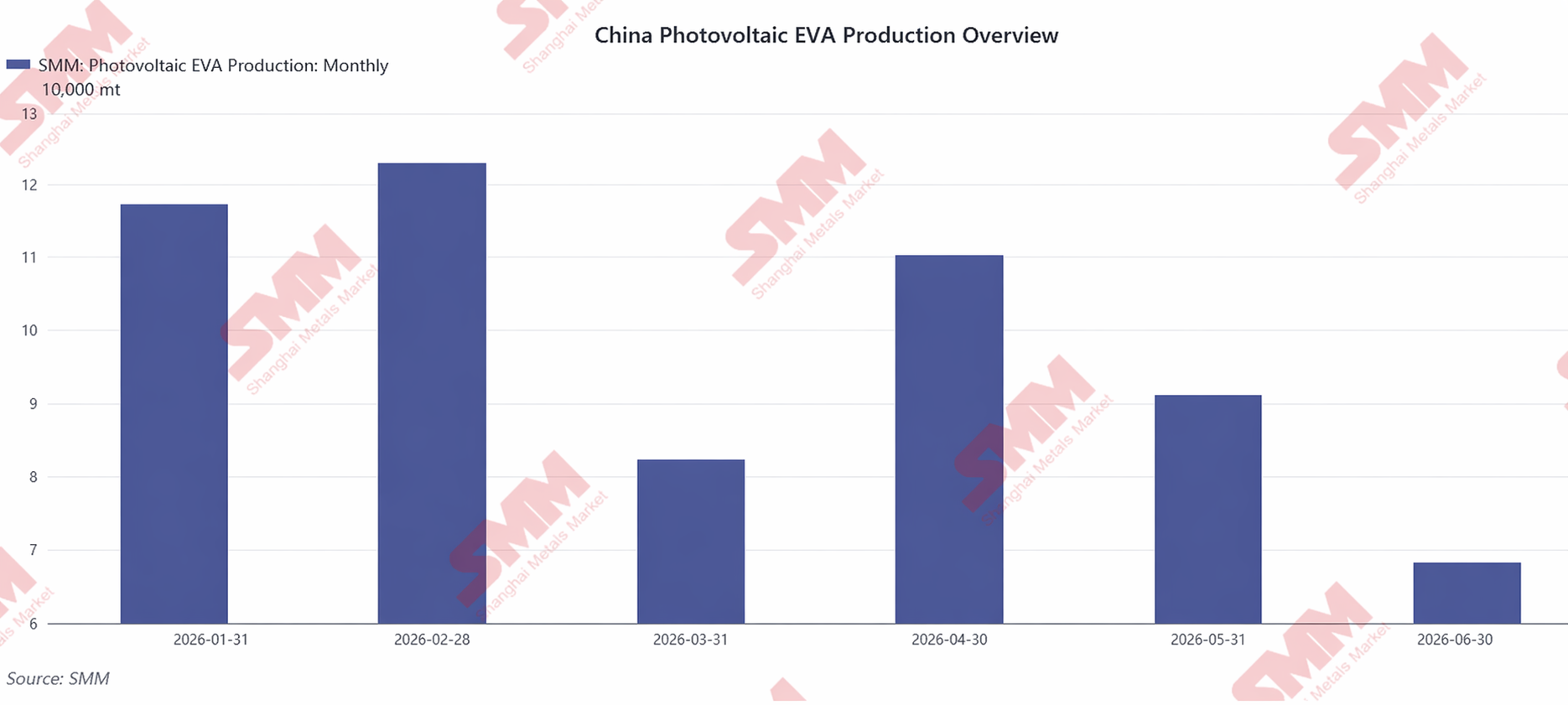

In H1 2026, China's total PV-grade EVA production was approximately 592,700 mt, down 18.16% YoY. In March, the module export rush drove scheduled production sharply higher, and film operation rates climbed in tandem. However, due to intensive maintenance at multiple facilities and proactive production control by petrochemical enterprises, PV-grade EVA production dropped significantly by 33.2% MoM, meaning supply did not keep pace with the demand surge, further amplifying the short-term supply-demand mismatch. In April, module scheduled production retreated to 28.8 GW, and the resin supply released earlier gradually became surplus. In the middle to later part of Q2, although downstream module scheduled production saw a mild recovery, film manufacturers adopted a conservative procurement strategy, buying only on an as-needed basis. At the same time, petrochemical enterprises continuously adjusted their production schedules between PV-grade and non-PV-grade materials to proactively control volumes, and overall industry supply pressure continued to ease.

3. Cost and Profitability

Ethylene and vinyl acetate, the two core raw materials, together account for about 80% of the PV-grade EVA production cost. In H1, resin costs completed a three-phase cycle of "geopolitical conflict escalation – consolidating at highs – demand weakening and pulling back," which was one of the core factors driving wild swings in EVA resin prices. From January to April, escalating US-Iran geopolitical tensions pushed up international crude oil, and ethylene and vinyl acetate climbed in tandem. Moreover, the increase in resin spot prices significantly outpaced the rise in raw material costs, and petrochemical plants' profits continued to recover. From May to June, as the module installation rush window ended, end-use demand weakened, dragging down EVA resin prices sharply. Meanwhile, enterprises' earlier high-priced raw material inventories were continuously consumed, and industry profitability simultaneously shrank rapidly.

II. PV-grade POE Resin: A High-Elasticity Market Driven by Import Dependence

Due to different supply-demand fundamentals and localisation progress, POE resin showed a clear divergence from EVA in terms of volatility magnitude and recovery pace.

1. Price Trend

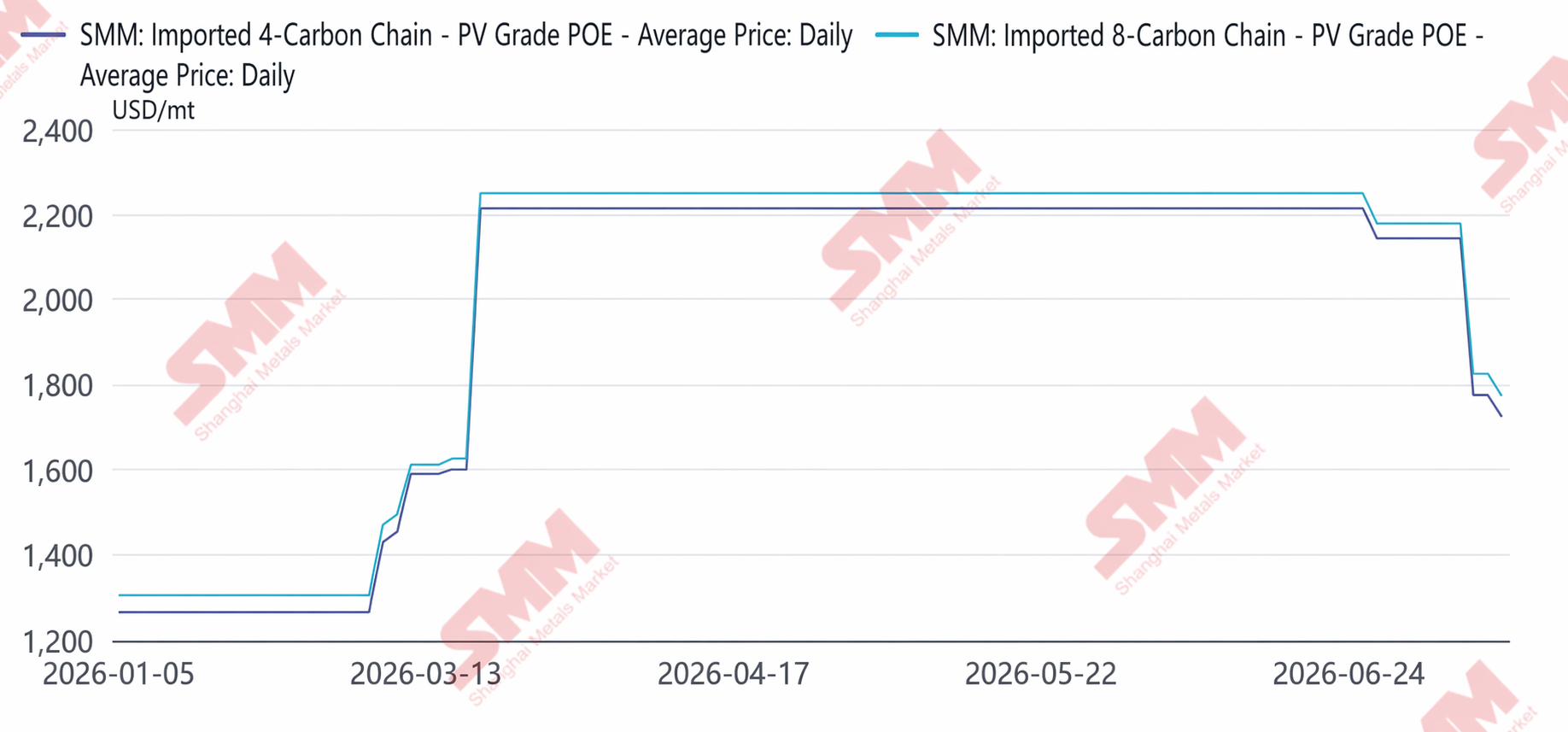

Imported C4-based POE climbed from $1,265/mt at the start of the year, was pushed to $2,215/mt in March by Middle East tensions, consolidated at the high of $2,215/mt from April to May, and eased to $2,144/mt in June. Domestic C4-based PV-grade POE prices moved sideways in a low range of 11,281-11,400 yuan/mt from January to February. In March, a significant cost-side increase rapidly lifted POE prices, and C4-based POE further surged to 16,000 yuan/mt in April, a cumulative increase of over 40% in two months. Entering May, as geopolitical tensions eased, downstream demand weakened, and new domestic POE capacity continued to come online, the supply-demand imbalance gradually intensified, and prices retreated from highs. In June, the market imbalance worsened further, POE prices accelerated downward, and by end-June C4-based POE prices had fallen back to around 13,000 yuan/mt.

2. Unique Characteristics of POE

POE localisation achieved phased breakthroughs, but in the short term, full import substitution still faces significant obstacles. In H1, domestic POE capacity steadily ramped up, and corresponding overseas import volumes shrank simultaneously. However, constrained by technical barriers such as product stability and catalysis processes, the Chinese market still needs imported grades to supplement supply. At the same time, due to relatively high raw material costs and the high technical threshold for pure POE film production, downstream film manufacturers had limited actual absorption capacity, making it difficult for end-use demand to see a large-scale release in the short term. The pace of supply expansion was significantly faster than demand growth.

III. H2 Outlook

In H2, both types of resin will face a tug of war between "expectations of demand recovery" and "supply growth pressure," but EVA will be under heavier pressure overall. For EVA, nearly 600,000 mt of new capacity may be released mainly from late Q3 to Q4, capping upside room for prices. Although there may be phased recovery opportunities during peak season, the upside is limited given the wave of capacity. For POE, new capacity release pressure also lies ahead, but under the weight of industry profitability pressure, some planned start-ups may be delayed, and actual incremental output could be lower than planned. From a long-term perspective, with the mandatory national energy consumption standard expected to take effect in 2027 and the advancement of industry capacity governance surveys, if these measures can effectively force the exit of outdated, high-energy-consuming capacity, the medium and long-term supply-demand pattern of both PV-grade EVA and POE resin is expected to continuously improve.

![2026 H1 PV Wafer Market Analysis and Outlook – Trade Barriers, Technology Iteration, and Capacity Rationalization [SMM Analysis]](https://imgqn.smm.cn/usercenter/VprpL20251217171738.jpg)

![[SMM PV News] TCL Solar Debuts at Vietnam International PV and Energy Storage Exhibition 2026](https://imgqn.smm.cn/usercenter/HfeeS20251217171739.jpg)