On July 9, Xingye Silver&Tin's stock price fell, closing down 2.65% at 32.35 yuan per share on the 9th.

In terms of news: On July 8, Xingye Silver&Tin stated on the investor interaction platform that the company's current capacity supply mainly relies on existing mines in operation, and details of annual capacity can be found in the company's periodic reports.

On July 8, Xingye Silver&Tin stated on the investor interaction platform that,the preparatory work for the Yinman Phase II project has been largely completed, and the company is currently coordinating and finalizing arrangements for the commencement of construction, planning to start in July. Once the specific start date is determined, the company will disclose it through an announcement as soon as possible.

On July 8, Xingye Silver&Tin stated on the investor interaction platform that, according to the JORC Code, the Competent Person SRK only uses the current Measured and Indicated Resources as the basis for ore reserve conversion and the production schedule plan. However, in actual operations, through continuous production drilling and exploration, the company may upgrade some Inferred Resources, which will then be incorporated into the actual mining and processing plan. Meanwhile, the Competent Person SRK uses Deswik software to generate stope shapes through stope optimization, which may be inconsistent with the stope layouts adopted in the company's routine production planning. Therefore, the company's actual future production schedule and operating performance may differ from the production schedule and related forecasts presented by the Competent Person SRK.

On July 8, Xingye Silver&Tin stated on the investor interaction platform that regarding the production of various metals in H1, please refer to the 2026 Semi-Annual Report scheduled to be released on August 29, 2026, in designated information disclosure media.

On the evening of June 30, Xingye Silver&Tin announced that it plans to acquire a 25% stake in Atlas Tin SAS held by Toyota Tsusho Corporation and Nittetsu Mining Co., Ltd. through a newly established overseas subsidiary, for a total consideration of $23.1136 million. After the transaction, the company will indirectly hold 100% equity in the target company, achieving full ownership of the Achmmach Tin Mine Project, aiming to simplify the governance structure, improve decision-making efficiency, and maximize the release of value from the tin ore assets.

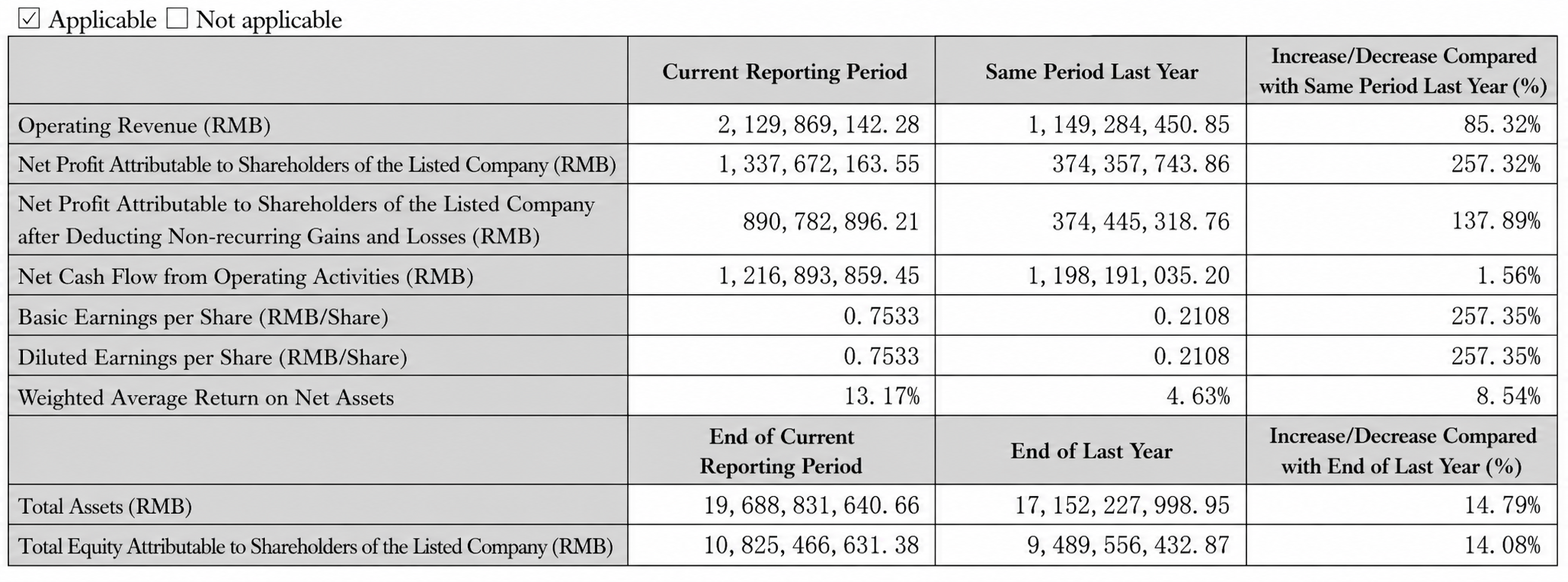

In terms of performance: Xingye Silver&Tin disclosed in its Q1 report that in January–March 2026, the company achieved operating revenue of 2,129.8691 million yuan, an increase of 85.32% over the same period last year; net profit attributable to shareholders of the listed company was 1,337.6722 million yuan, an increase of 257.32% over the same period last year. As of March 31, 2026, the company’s total assets were 19,688.8316 million yuan, and the net assets attributable to shareholders of the listed company were 10,825.4666 million yuan.

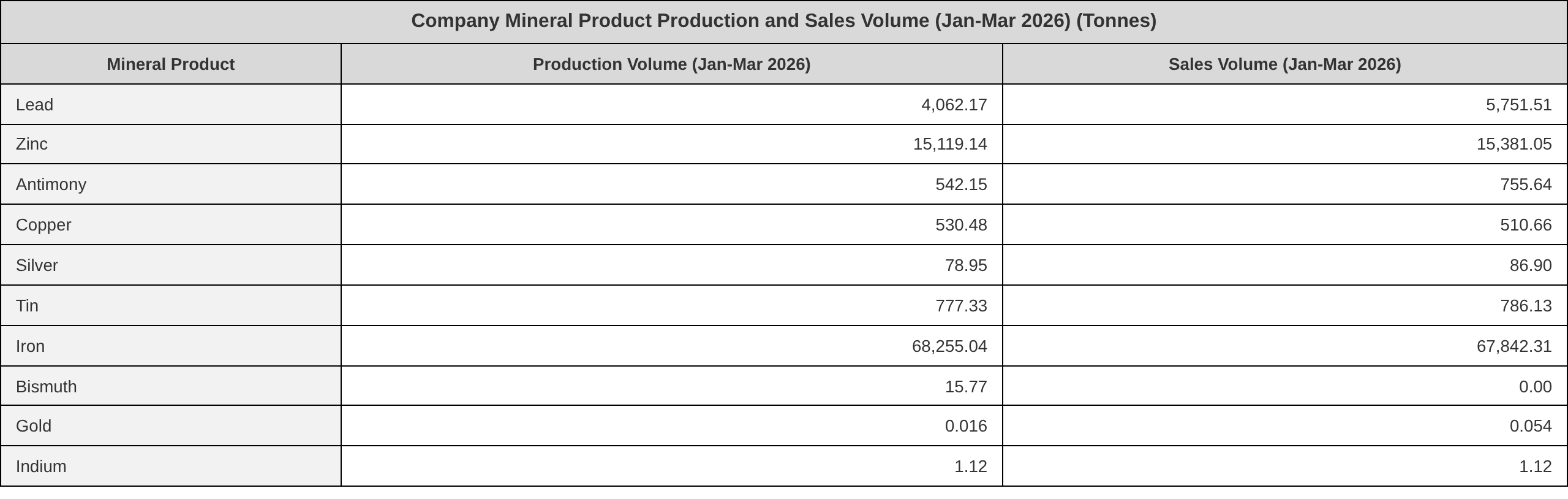

Revenue composition: For January–March 2026, the proportion of operating revenue from the company’s main ore products to total operating revenue was as follows: ore-derived silver RMB1,410.11 million, accounting for 66.21%; ore-derived tin RMB234.04 million, 10.99%; ore-derived zinc RMB228.12 million, 10.71%; ore-derived lead RMB71.85 million, 3.37%; ore-derived antimony RMB53.10 million, 2.49%; ore-derived gold RMB51.02 million, 2.40%; ore-derived iron RMB44.17 million, 2.07%; ore-derived copper RMB35.65 million, 1.67%; ore-derived indium RMB524,100, 0.02%; of which, ore-derived tin and ore-derived silver combined accounted for 77.19%.

Xingye Silver&Tin stated in its Q1 report: Operating profit for the current period increased by 238.16% compared with the previous period, total profit increased by 236.36%, and net profit attributable to owners of the parent company increased by 257.32%; the main reasons were: Selling prices of the company’s main ore products such as silver and tin rose YoY during the reporting period; Yubang Mining’s capacity was gradually released, leading to a significant YoY increase in ore-derived silver production and sales volume; the transfer of a 60% equity interest in Shuangyuan Nonferrous resulted in investment income of RMB321 million.

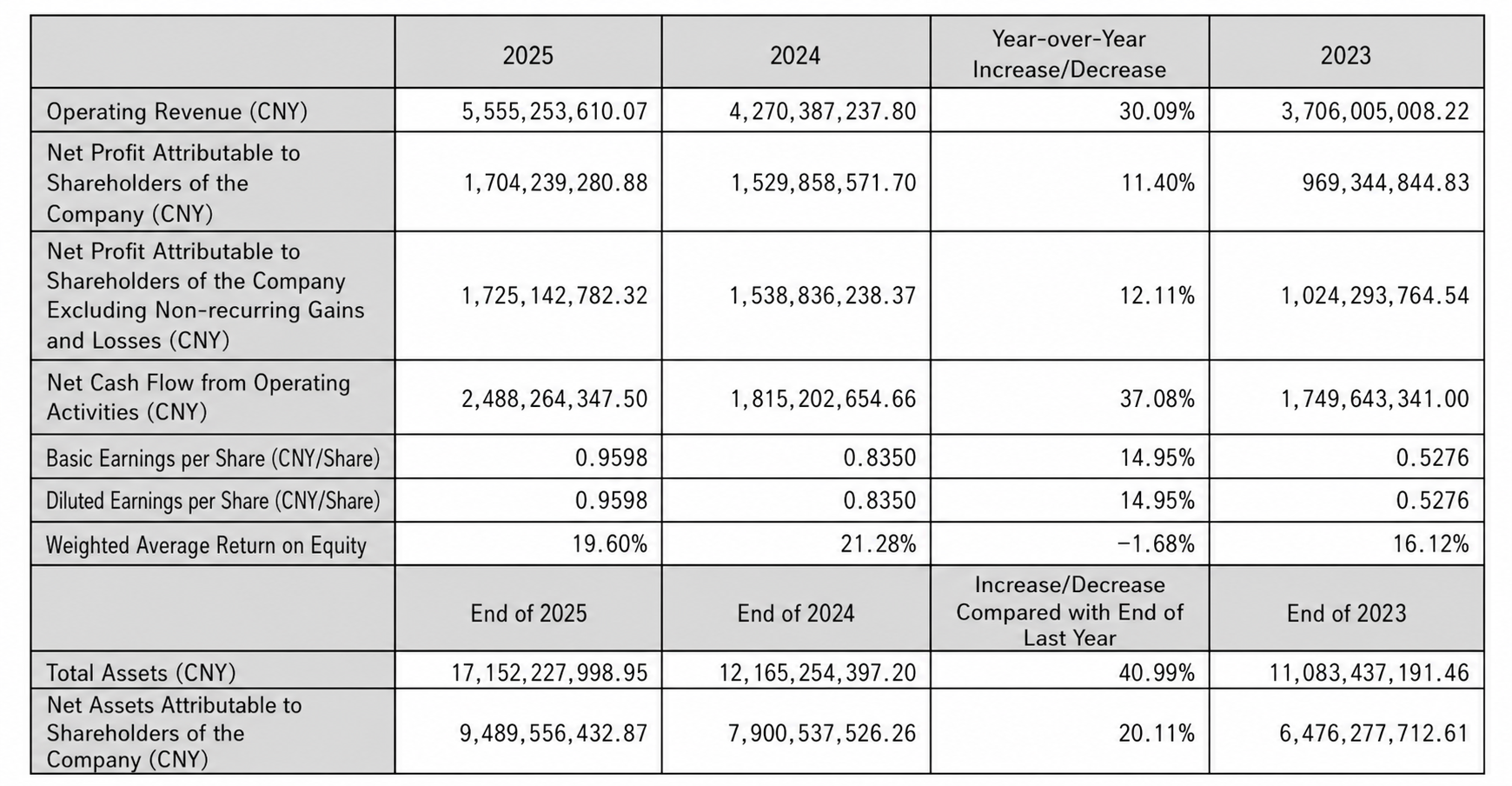

Xingye Silver&Tin’s published 2025 annual report shows that in 2025, the company achieved operating revenue of RMB5,555.25 million, up 30.09% YoY; total profit of RMB2,096.24 million, up 18.75% YoY; and net profit attributable to shareholders of the listed company of RMB1,704.24 million, up 11.40% YoY.

According to Xingye Silver&Tin’s announcement: In 2025, the proportion of operating revenue from the company’s main ore products to total operating revenue was as follows: ore-derived silver RMB2,175.78 million, accounting for 39.17%; ore-derived tin RMB1,649.64 million, 29.70%; ore-derived zinc RMB975.87 million, 17.57%; ore-derived lead RMB220.95 million, 3.98%; ore-derived iron RMB180.38 million, 3.25%; ore-derived copper RMB133.00 million, 2.39%; ore-derived antimony RMB100.36 million, 1.81%; ore-derived gold RMB82.34 million, 1.48%; ore-derived bismuth RMB16.67 million, 0.30%; of which, ore-derived tin and ore-derived silver combined accounted for 68.86%.

Regarding its main business and key performance drivers, Xingye Silver&Tin stated in its 2025 annual report: "The company is a large-scale mining group principally engaged in the exploration, mining and mineral processing of non-ferrous metals and precious metals."As of the disclosure date of this report, the Company has more than 20 subsidiaries, including 8 in-production mining companies, namely Yinman Mining, Qianjinda Mining, Yubang Mining, Rongguan Mining, Xilin Mining, Rongbang Mining, Ruineng Mining, and Bosheng Mining; the Achmmach tin mine of Atlas Tin SAS under Atlantic Tin is in the construction phase; Tanghe Shidai Mining is in the suspension phase; Yitong Mining and Yunnan Xingui are in the exploration phase. Hainan Fund is mainly engaged in equity investment management; Xingye Gold (Hong Kong) is principally involved in metals and mining trade and enterprise mergers and acquisitions, and is responsible for expanding markets outside China and acquiring high-quality mineral resources ex-China; Hainan Guomao and Tianjin Guomao are mainly engaged in the sale of non-ferrous metal ore products and the procurement of some raw materials; Xingye Ruijin primarily conducts process research, technology R&D, and upgrading in areas such as prospecting, mining and dressing, and the comprehensive recycling and utilization of tailings. Tibet Shannan Antimony & Gold, Tibet Xinda Mining, and Hinggan League Fuxingtun Mining serve as the Company's regional resource integration platforms. During the reporting period, the Company successfully acquired an 85% equity stake in Yubang Mining. Based on statistics as of the end of 2023 compiled by The Silver Institute, the Yubang single-silver mine ranks first in Asia and fifth globally. This acquisition further strengthened the Company's resource advantages and laid a solid resource foundation for its sustainable development. Simultaneously, using its subsidiary Xingye Gold (Hong Kong) as the investment vehicle, the Company intensified its investment in mineral resources ex-China and successfully acquired a 100% equity stake in Atlantic Tin. This acquisition is a key measure in implementing the Company's "going global" strategy. According to the classification criteria for large-scale tin mines in the "Standards for Classification of Mineral Resources/Reserves Scale" (DZ/T 0400-2022), the Achmmach tin mine owned by Atlantic Tin is now equivalent to 5 large deposits. Through this integration of tin resources outside China, the Company has further improved its international tin mining footprint and reserved significant strategic resources for its long-term development. The Company's primary source of performance is its non-ferrous metal mining and dressing business. During the reporting period, revenue from the non-ferrous metal mining and dressing segment accounted for 99.64% of total operating revenue in 2025. Key factors affecting the operating performance of this segment include the production and sales volumes of major products, market prices, and the costs of the non-ferrous metal and precious metal mining and dressing business.

Regarding its operating plan, Xingye Silver&Tin stated in its 2025 annual report: 2026 is the final year of the Company's "Second Three-Year" Plan. The Board of Directors will focus closely on the theme of high-quality development, fully implement established work targets, continue to deepen the concept of "Trust and Collaboration," and make every effort to achieve the final targets of the "Second Three-Year" Plan, with an emphasis on the following tasks: 1. Uphold the bottom line of safety and environmental protection. Using the 2026 "Year of Safety Management Implementation" initiative as a lever, comprehensively consolidate safety responsibilities, reinforce the achievements of the "Collective Calm Year in Safety," strengthen risk anticipation and process control, and resolutely prevent all types of safety and environmental incidents to achieve safe, steady, green, and low-carbon development. 2. Fully advance the construction of key projects, strengthen whole-process management of project budgets, schedules, and quality, and coordinate the implementation of the Yinman Mining 2.97 million mt expansion, the Yubang Mining 8.25 million mt expansion, the Morocco project, the Budong Yin’gen Mining (entrusted) project, and others, ensuring they are completed on schedule to reach full production and release capacity benefits. 3. Continuously strengthen exploration and reserve expansion, properly balance production operations with geological exploration, steadily advance exploration in existing mines and surrounding areas, accelerate the conversion and upgrading of resources into reserves, and constantly consolidate the resource base. 4. Deepen industrial synergy and resource integration, leverage the core regional advantages of Inner Mongolia, and steadily expand resource deployment outside China; adhere to the focus on silver and tin as the main business, enriching and optimizing resource varieties. Solidly promote the subsequent acquisition and integration of Weiling Co., actively track high-quality mineral project opportunities in and outside China, and enhance overall competitiveness through synergistic industrial M&A. 5. Further strengthen institutional enforcement and internal control management, drive the effective implementation of all systems, processes, and control requirements, and improve the company’s lean management; strengthen enforcement, ensuring production plans, comprehensive budgets, and all work deployments are fully executed, and promote the deep integration of corporate culture with business management. 6. Fully advance preparations for the Hong Kong stock listing, accelerate the establishment of dual capital market platforms at home and abroad, enhance cross-border capital operation capabilities, provide stronger financial support for the company’s resource integration and strategy execution, and push the company’s high-quality sustainable development to a new level.

Looking back at the price performance of tin in 2025 and Q1 this year, we can see: the average price of SMM 1# tin spot on December 31, 2025 was 326,450 yuan/mt, up 80,450 yuan/mt from the average of 246,000 yuan/mt on December 31, 2024, for a 32.7% increase in 2025. The SMM 1# tin spot price on March 31 this year was 371,550 yuan/mt, up 45,100 yuan/mt from the average of 326,450 yuan/mt on December 31, 2025, for a 13.82% increase in Q1 this year.

As for tin spot prices: SMM 1# tin spot was quoted at 408,500–411,000 yuan/mt, with an average price of 409,750 yuan/mt, up 0.11% from the previous trading day.

On July 9, tin market transactions displayed phased characteristics along with futures fluctuations. Throughout the day, futures maintained wild swings; when intraday prices dipped to near 400,000 yuan/mt, spot transactions recovered slightly from the previous trading day, with some enterprises showing tentative purchase willingness and making small-scale purchases. However, as futures prices rose and surged in the afternoon, the buyer’s chasing-high sentiment rapidly cooled. Overall, the current tin market trend remains closely tied to macro sentiment. From a fundamental perspective, however, the release of downstream rigid demand during the recent price correction consumed some spot cargo supply, resulting in a stalemate between low inventory and weak trading. In the near term, the most-traded SHFE tin contract is expected to maintain a fluctuating trend.

Looking back at the spot price performance of silver in 2025 and Q1 2026, the SMM 1# silver (Ag99.99%) average price on December 31, 2025 was 18,430 yuan/kg, and on December 31, 2024 was 7,440 yuan/kg, with the average price rising by 10,990 yuan/kg in 2025, a gain of 147.71%. The SMM 1# silver price on March 31 was 18,341 yuan/kg, which fell by 89 yuan/kg (down 0.48%) compared to the December 31, 2025 average of 18,430 yuan/kg.

In the silver spot market on July 9, some suppliers began offering at premiums. Overall demand was weak, resulting in sluggish trading, with downstream transactions mainly driven by negotiations. Morning quotes in Shanghai were concentrated around parity to a premium of 10 yuan/kg against the TD contract. Large producers’ delivery brand offers were firm, but actual transaction prices might dip toward the lower end. In Shenzhen, some nationally-standard sources were quoted around a small discount to a premium of 5 yuan/kg against the TD contract, with small premium quotes being cleared quickly. Premiums against the most-traded SHFE 2608 contract were quoted at a discount of 15 to 35 yuan/kg on the day. Overall, the precious metals macro trend was falling under pressure, weighed down by both heightened geopolitical risks and divergence among US Fed policy stances. Spot premiums weakened slightly, with transactions leaning toward parity. Demand was soft, reflecting a ‘rush to buy amid continuous price rise and hold back amid price downturn’ mentality in the market.

Recommended Reads:

![Platinum and Palladium Market Price Review and Expectations Brief Review (July 9, 2026) [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/gePcx20251217171735.jpg)

![Silver Falls Over 6% Weekly as Macro Pressure and Geopolitical Shocks Resonate [SMM Silver Weekly Review]](https://imgqn.smm.cn/usercenter/QnbfL20251217171735.jpeg)