News Release, July 9, 2026

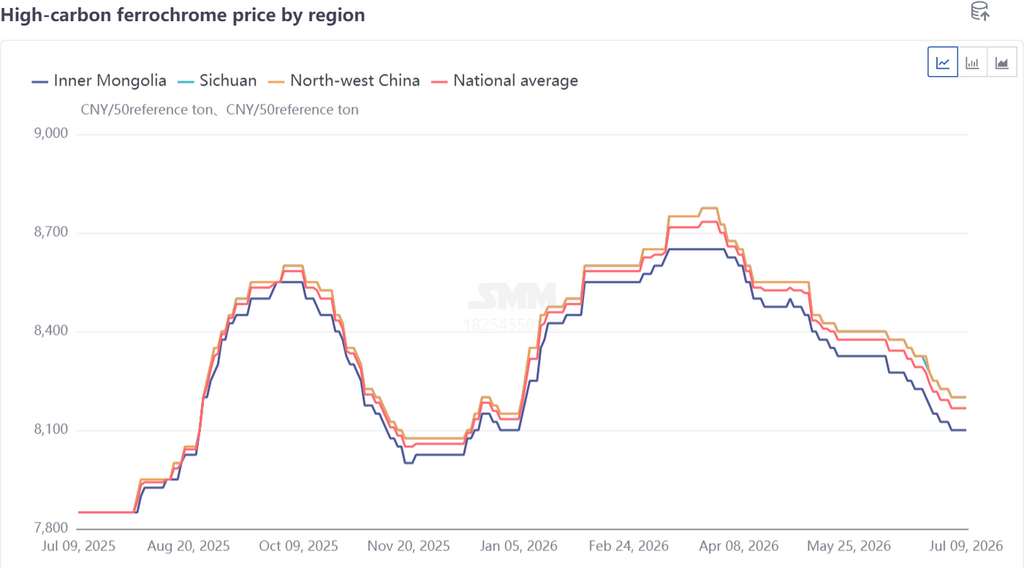

China's high-carbon ferrochrome prices saw distinct phased volatility in H1 2026. After surging to a high of RMB 8,650 per 50-base-tonne in Q1, prices gradually retreated to RMB 8,100 per 50-base-tonne in Q2, driven primarily by supply-demand mismatch.

Price Review: Rising in Early Stage Then Sustained Downward Drift

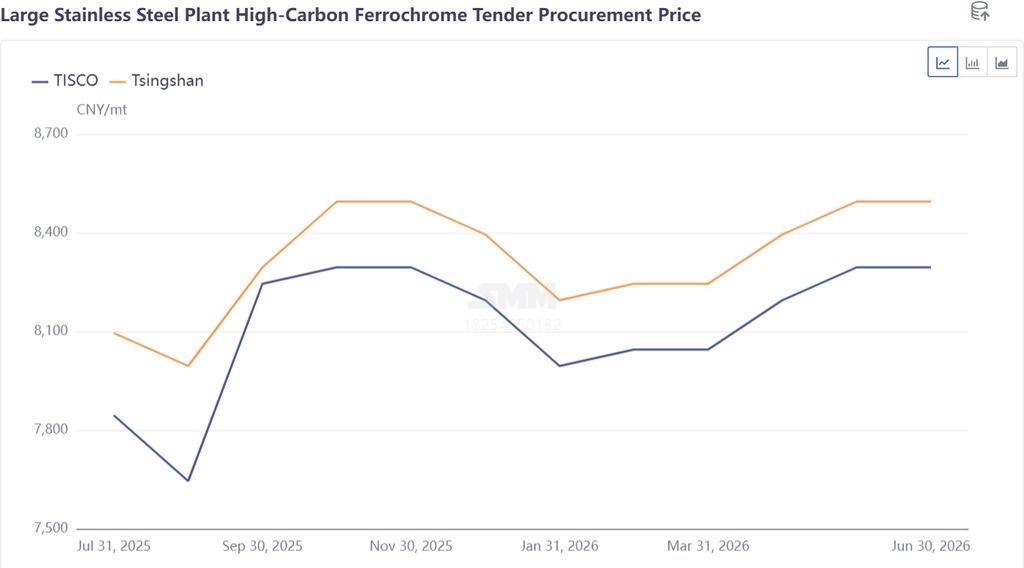

The sharp Q1 rally in ferrochrome prices was largely fueled by downstream stainless steel demand. Early in the year, news emerged of tightened Indonesian nickel ore quotas, pushing up both futures and spot prices of stainless steel simultaneously. Stainless steel mills maintained high production schedules, and robust procurement demand for ferrochrome emerged amid pre-Spring Festival inventory restocking and upbeat expectations for the subsequent consumption peak, lifting ferrochrome prices. Tender prices at major steelmakers climbed to RMB 8,495 per 50-base-tonne.

On the cost side, positive market sentiment plus rising ocean freight rates following the outbreak of Middle East conflicts kept offshore chrome ore prices climbing, hitting USD 318 per tonne at end-March. Domestic chrome ore prices rose to RMB 60.5 per metal unit, pushing up ferrochrome production costs and forming strong bottom-line price support.

In Q2, ferrochrome prices edged down from highs amid a weak supply-demand balance. Southern smelters ramped up output as the wet season arrived, driving ferrochrome production to repeated all-time highs and creating ample supply. Downstream stainless steel output stayed elevated yet posted a smaller growth rate than ferrochrome supply. Supported by firm prices of alternative raw materials including ferronickel and stainless steel scrap, steel mills sought to suppress ferrochrome prices to safeguard margins, with major tender prices falling to RMB 8,295 per 50-base-tonne.

Additionally, steel mills had mostly completed raw material stockpiling in the prior quarter, and procurement demand softened amid the off-season. Slow inquiry and transaction activity kept ferrochrome prices under persistent downward pressure with steady corrections.

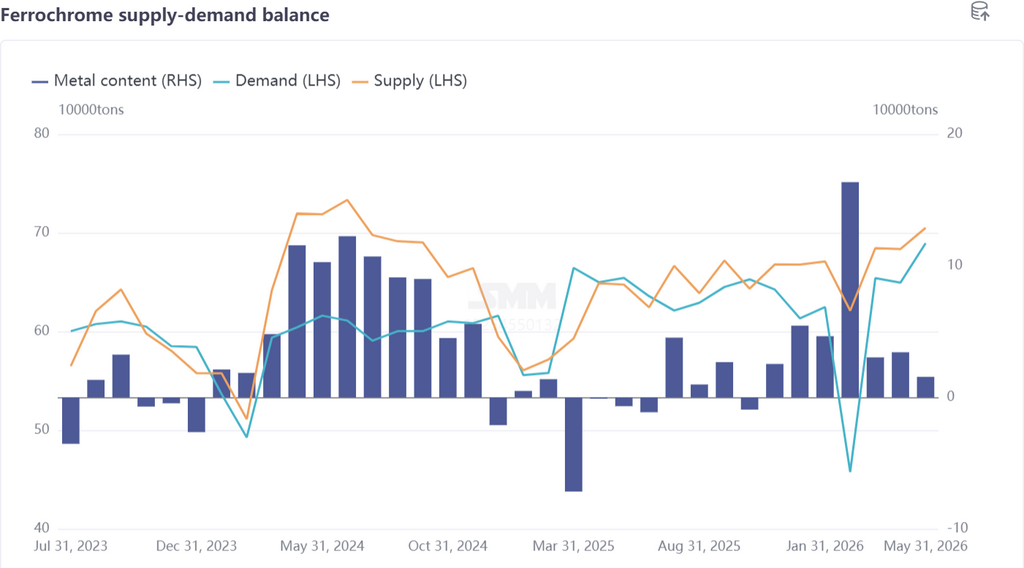

Supply Landscape: Domestic Output Dominates with Rising Share; Import Volumes Remain Low with Limited Market Impact

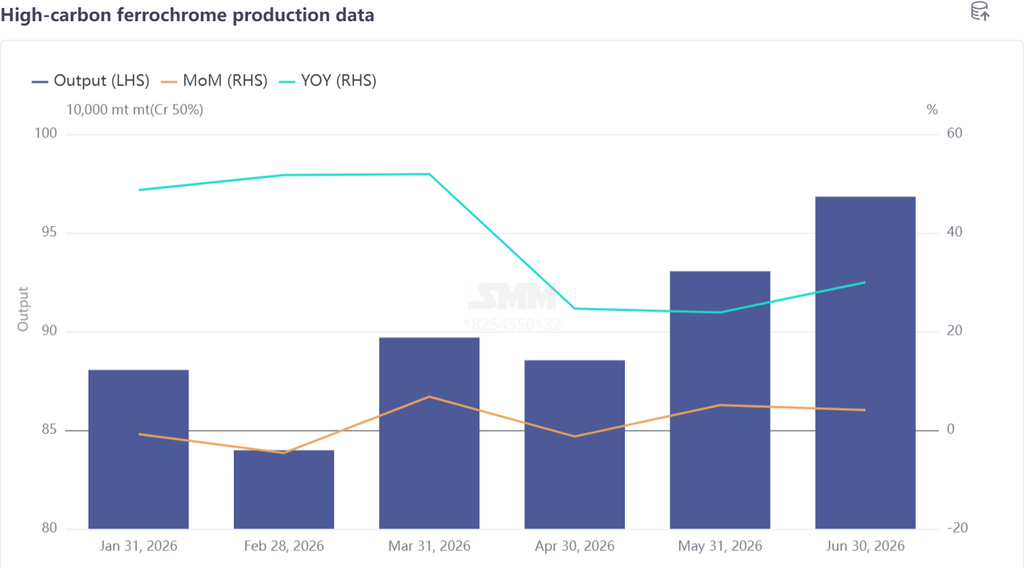

China's total high-carbon ferrochrome output reached 5.4014 million tonnes in H1 2026, averaging 900,200 tonnes monthly — a 36.79% jump from the 658,100-tonne monthly average recorded in H1 2025, with a marked production uptick in Q2.

Sustained decent profitability throughout most of 2025, compounded by the Q1 ferrochrome price rally, boosted production enthusiasm among smelters. Northern Inner Mongolia, the country's top producing region, maintained near-normal operations even during the January–March winter period, alongside new capacity commissioning.

Entering Q2, the wet season brought a 36% electricity tariff cut in southern regions, particularly Sichuan, delivering prominent low-cost production advantages. Smelters resumed and ramped up operations one after another, lifting national ferrochrome output to an all-time peak of 968,300 tonnes in June.

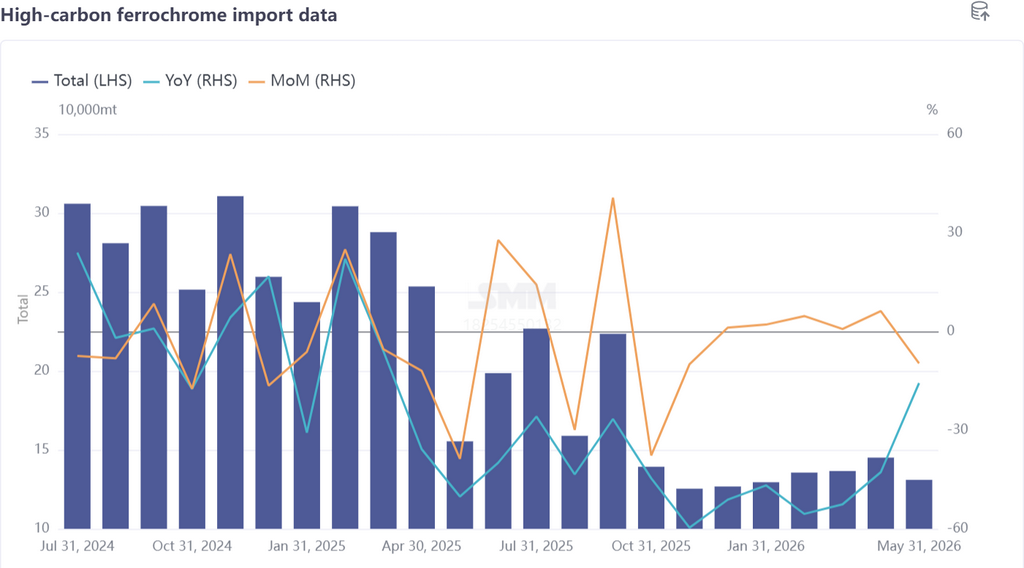

For imported ferrochrome: over 85% of South Africa's ferrochrome capacity suspended production starting May 2025, slashing China's average monthly ferrochrome imports by 43.62% from 240,500 tonnes to 135,600 tonnes. Per SMM statistics, China’s total ferrochrome imports totalled 677,900 tonnes in Jan–May 2026, accounting for a narrowed 11.14% of the country's overall ferrochrome supply. Imports are projected to stay muted in H2 2026.

While the South African government approved a preferential power tariff of 0.62 Rand per kWh for ferrochrome smelting in May, major producers Glencore and Samancor are still in the planning phase for full resumption. The slow recovery of South Africa's ferrochrome sector means export volumes to China will see only minor short-term fluctuations.

Demand Landscape: Overall Solid Performance with Obvious Seasonal Swings

Stainless steel, the primary downstream sector of ferrochrome, trended upward with volatility across H1 2026, with macro headlines dictating price movements while output stayed high. SMM data shows China's total stainless steel output hit 20.08 million tonnes in H1 2026, translating to chrome demand of roughly 3.4457 million metal tonnes, a year-on-year rise of 2.3% — far lower than the 12.94% growth in ferrochrome supply, tipping the ferrochrome market into an oversupply cycle.

In February, Spring Festival holidays triggered extensive maintenance and production cuts at stainless steel mills, pushing ferrochrome surplus to a peak of 170,000 metal tonnes (equivalent to around 340,000 physical tonnes). However, market trading activity was largely dormant during the holiday period with sparse spot inquiries, so ferrochrome prices avoided drastic declines.

Cost Side: Adjusted Power Policies Widen North-South Cost Gap

Ferrochrome production costs fluctuated higher before drifting downward in H1 2026, with a peak-to-trough price swing of 4.24%. Chrome ore price shifts served as the core driver, alongside adjustments to electricity pricing policies.

Q1 saw consistent upward pressure on high-carbon ferrochrome production costs. Driven by Indonesia's nickel ore policies, stainless steel futures and spot prices rose, passing positive sentiment upstream and lifting offshore chrome ore prices sharply in the short run, which in turn buoyed domestic spot ore quotations.

Furthermore, power policy revisions in southern provinces including Guangxi and Guizhou eliminated fixed time-of-use electricity tariffs, lifting power costs for ferrochrome production. In contrast, Inner Mongolia maintained stable power rates, steadily widening the production cost gap between northern and southern smelters.

Q2 brought gradual cost declines for high-carbon ferrochrome. South Africa’s slow ferrochrome restart kept chrome ore export-focused, with global monthly shipments holding steady at a high of 2.9 million tonnes and arriving at Chinese ports in batches through Q2. Domestic chrome ore inventories accumulated to an all-time high of 4.9 million tonnes amid surplus pressure. Ore traders were forced to offer discounts to clear stock, with spot prices drifting lower and eroding cost support for ferrochrome.

Market Outlook

The ferrochrome market is expected to trade sideways centred on the core theme of supply oversupply. Domestically, new high-carbon ferrochrome capacity will come online sequentially to sustain elevated output. China's stainless steel sector faces dual headwinds: domestic anti-cutthroat competition policies curb capacity expansion, while external trade protectionism imposes export restrictions. Capacity growth will mainly rely on replacement rather than greenfield expansion, significantly slowing output expansion. The prominent supply-demand mismatch will inevitably keep prices under sustained pressure.

Overseas, South Africa's preferential power tariffs pave the way for full-scale ferrochrome restarts. Zimbabwe is expanding local capacity leveraging abundant chrome ore resources and foreign investment. India, Indonesia and other nations have rolled out production expansion plans to support their domestic stainless steel industries. A concentrated surge in global ferrochrome capacity is projected within two years, which will inevitably exacerbate worldwide oversupply.

![Silicone product prices remain firm, while market transactions are sluggish [SMM Silicone Weekly Review]](https://imgqn.smm.cn/usercenter/TdoSs20251217171724.jpeg)

![Demand for Silicon Metal Raw Materials Continues to Rise, Petroleum Coke Price Center Will Drift Lower [SMM Silicon Metal Raw Material Weekly Review]](https://imgqn.smm.cn/usercenter/gKDYO20251217171723.jpeg)

![Tug-of-War between Longs and Shorts Intensifies, Silicon Metal Price Fluctuation Range Widens [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/YhgvU20251217171725.jpg)