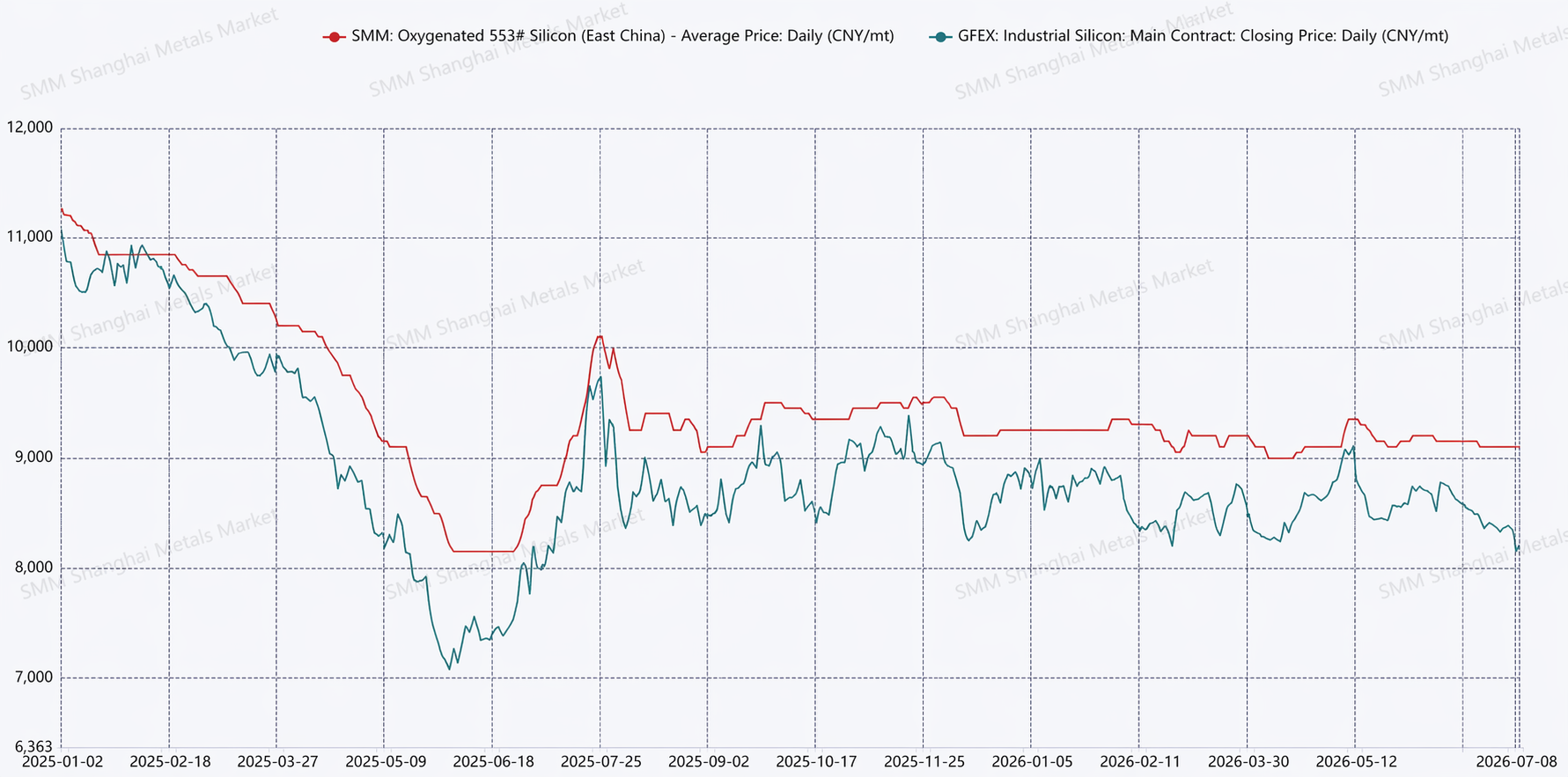

SMM, July 9: Price Side: Reviewing H1 2026, the fluctuation range of spot silicon metal prices was significantly narrowed, impacted by low capacity utilization rates for silicon metal, limited demand growth, and silicon metal prices already operating at relatively low levels, leaving them capped by cost support below and constrained demand above. According to SMM price data, the spot silicon metal price fluctuation range was 38% in 2025, while it was narrowed to within 5% in H1 2026. On the futures price side, the fluctuation range of the most-traded silicon metal futures contracts was 59% in 2025, narrowed to 14% in H1 2026.

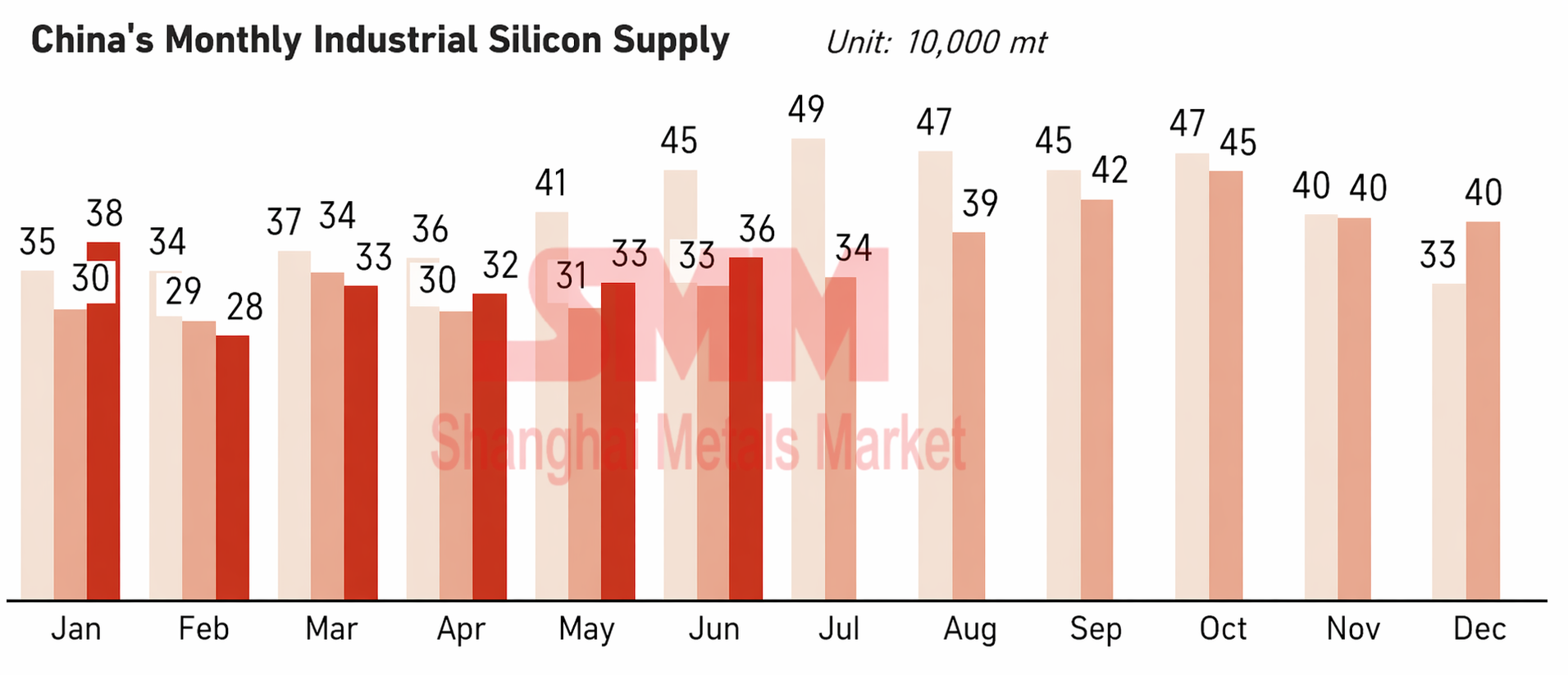

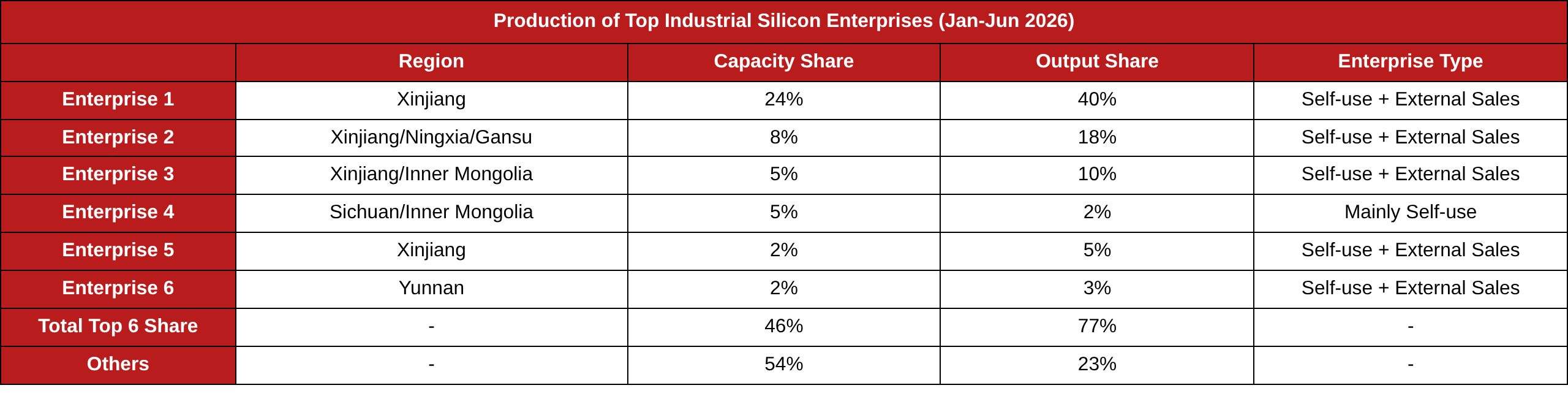

Supply Side: According to SMM data, silicon metal production in H1 2026 was 1.99 million mt, up 6% YoY. The supply of silicon metal was characterized by high regional concentration. From January to June, Xinjiang accounted for up to 65% of silicon metal supply, Inner Mongolia about 11%, Gansu about 9%, and Ningxia about 9%, while Sichuan and Yunnan had a small supply proportion due to the dry season. In June, the arrival of the rainy season in Sichuan and Yunnan drove some silicon enterprises to resume production, but total output from the two provinces was lower than the same period last year, with Sichuan's production down about 40% YoY. From the perspective of enterprise distribution, the number of enterprises in production has declined year by year. However, as the supply proportion of top-tier players increased, industry concentration effects were evident. In H1 2026, the top six companies accounted for 77% of production supply, while the market share and market competitiveness of small and medium-sized players declined, squeezing their survival space.

Demand Side: Overall end-use consumption of silicon metal in H1 was relatively weak. Breaking it down, in the polysilicon sector, polysilicon prices remained persistently low, with corporate profits under pressure and operating rates below 30%. Expectations for production resumptions by top-tier polysilicon enterprises in June and Q3 are expected to drive an increase in silicon metal consumption in H2. In the silicone sector, the industry continued its joint production reduction strategy in H1, with operating rates maintained at a low level of 60%-66%. During this period, DMC prices were in the range of 13,000-14,900 yuan/mt, and silicone monomer enterprises showed relatively good profitability. In the aluminum alloy sector, operating rates at primary aluminum alloy were basically stable. Starting in May, secondary aluminum alloy experienced significant production cuts due to the invoicing policy's impact, leading to a shortage of compliant aluminum scrap supply.

Inventory Side: According to SMM social inventory data, inventory levels were persistently in the range of 550,000-570,000 mt throughout H1 2026, indicating significant destocking pressure (incomplete statistics, and the data does not include upstream and downstream in-factory inventory). Looking at the inventory structure, in-factory inventory levels at silicon enterprises declined compared to last year, while intermediate links accounted for a relatively high proportion of inventory.

On the import and export front, from January to May 2026 cumulative silicon metal exports reached 325,600 mt, up 16% YoY, marking a strong performance.

Overall, in H1 this year, silicon metal prices moved sideways at persistently low levels. In H2, production resumptions in Sichuan and Yunnan during the rainy season are expected to add supply, with supply growth outpacing demand growth. The full-year silicon metal supply-demand balance is expected to remain relatively loose. In June, the silicon metal market was in a transition from both weak supply and demand to both strengthening, operating at low levels. The short-term tug-of-war between sellers and buyers centers on the balance between supply increments from Sichuan and Yunnan during the rainy season and demand growth from polysilicon production resumptions. Currently, silicon metal supply is concentrated among top-tier players and regions, with strong cost support from Xinjiang production areas where costs are lower. On the upside, prices depend on demand drivers and the hedging and selling positions of producers. Additionally, watch for disruptions from liquidity and macro sentiment.

![Silicone product prices remain firm, while market transactions are sluggish [SMM Silicone Weekly Review]](https://imgqn.smm.cn/usercenter/TdoSs20251217171724.jpeg)

![Demand for Silicon Metal Raw Materials Continues to Rise, Petroleum Coke Price Center Will Drift Lower [SMM Silicon Metal Raw Material Weekly Review]](https://imgqn.smm.cn/usercenter/gKDYO20251217171723.jpeg)

![[SMM Analysis] 2026 Ferrochrome Semi-Annual Review: Booming Supply & Demand Yet Oversupply Risks Loom](https://imgqn.smm.cn/usercenter/vbcyk20251217171723.jpeg)