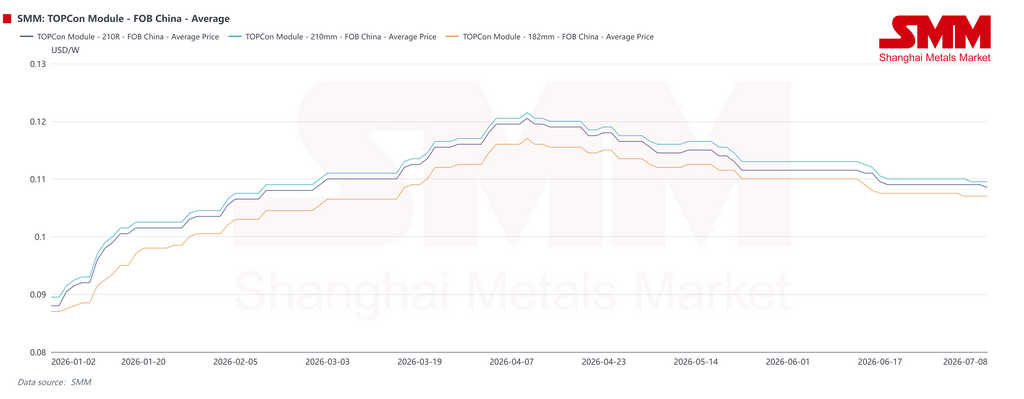

Overseas PV Markets Enter a Policy-Driven Reset After H1 Demand Pull-Forward. Export tax changes, freight volatility, raw material costs, and policy deadlines lifted China TOPCon FOB prices in Q1 before weaker demand pulled them back to $0.108-0.112/W by late June.

SMM H1 2026 Overseas PV Market Review

Overseas photovoltaic markets in the first half of 2026 were defined by demand pull-forward, prices that rose before falling, and increasingly strict policy barriers. China TOPCon module FOB export prices strengthened in Q1, supported by the export tax rebate transition, higher silver and raw material costs, and overseas inventory-building by manufacturers.

In Q2, that momentum faded. As policy disruption eased and overseas buyers became less willing to accept high-priced modules, the price center moved lower. By the end of June, mainstream FOB prices had largely stabilized at $0.108-0.112/W.

Regional performance diverged sharply. India saw a record installation rush before the ALMM cell list took effect. Europe moved through a full cycle from export rush and warehouse restocking to visible inventory pressure. Southeast Asian demand recovered gradually as module prices fell, while Pakistan entered a structural adjustment phase after changes to its net metering regime. In the Middle East and Africa, geopolitical disruption weighed on deliveries, but sovereign project pipelines continued to support medium-term demand.

SMM expects overseas new PV installations to fall temporarily to around 224 GW in 2026, down about 4% year on year. The long-term growth base remains intact, but the market is moving into a more selective and policy-driven phase.

Europe: Restocking Supported Q1, But Compliance Checks And Negative Prices Weighed On Q2

Europe shifted from active order intake to inventory digestion in the first half. At the start of the year, traditional holidays slowed Chinese module exports. After the holiday period, supply chains resumed, the export tax rebate window narrowed, and manufacturers concentrated shipments, creating a clear export rush.

Order intake and inventory-building in Europe were relatively strong in Q1. Some suppliers increased European warehouse stocks at the same time, pushing channel inventories higher.

Demand remained resilient in March and April. Some utility-scale projects reached grid-connection deadlines in March, while commercial operation date requirements and pre-summer grid-connection schedules supported orders in April. However, new procurement was increasingly focused on rigid restocking and project delivery rather than broad new demand.

By late Q2, the inventory pressure built up in Q1 became more visible. Buyers turned more cautious, and frequent negative power prices in parts of Europe disrupted return expectations for utility-scale projects. Module prices corrected from previous highs.

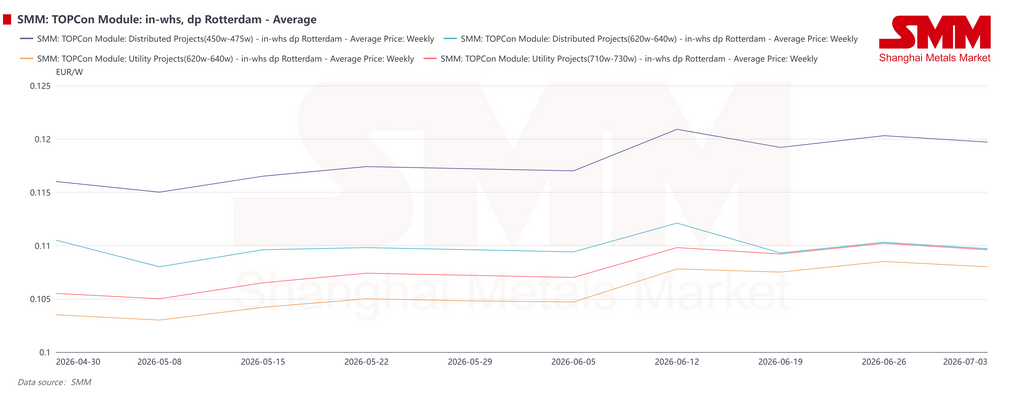

Distributed generation and commercial and industrial projects performed better and provided some support to demand. In application terms, distributed TOPCon modules saw larger price cuts because of pressure from BC module pricing. Products in the 450-475 W range, which mainly serve specific distributed demand, maintained relatively higher prices.

After May, module price declines in Europe were relatively limited. Earlier prices had already corrected, and manufacturers were less willing to make further large concessions. At the same time, a weaker euro against the renminbi and higher freight rates on Europe-bound routes in late May raised landed costs and provided new price support.

In mid-June, warehouse turnover pressure increased at major distribution hubs such as Rotterdam, and duty-paid warehouse pickup prices rose temporarily in some areas. By the end of the month, however, limited new utility-scale demand led module producers to cut offers again to compete for orders.

Europe Enters A Plateau After Years Of Rapid Expansion

Europe's PV market has moved from rapid expansion into a plateau and structural adjustment phase. New installations have grown strongly in recent years, and the overall market size is now high. The growth model is shifting from fast volume expansion to structural optimization.

In the short term, Europe may face adjustment pressure from slower residential demand, grid-connection bottlenecks, more frequent negative power prices, and policy changes. Installation growth could slow as a result.

In the medium and long term, Europe still has growth potential. Energy transition targets, rising building-integrated PV penetration, and improving storage deployment should support demand. SMM expects Europe's annual new installations to recover to around 70 GW by 2030.

Policy became the most important variable in H1. EU restrictions on inverters linked to "high-risk countries" expanded further toward battery energy storage systems and core power conversion systems. Projects already notified and sufficiently mature must enter formal decision, approval, or approvable status before November 2026 to qualify for transitional treatment.

Q4 will become a key window for determining mature project status. In the strictest scenario, some projects may face supplier replacement, contract renegotiation, financing adjustments, or even investment failure. In the short term, the policy may instead encourage some project owners to lock in equipment contracts early in order to qualify as mature projects, creating temporary rush demand.

In March 2026, the EU released an industrial acceleration proposal that would introduce local manufacturing requirements for publicly funded PV and energy storage products. Within three years of implementation, projects participating in public procurement or tenders would need to use EU-made inverters and cells. If a single third country accounts for more than 40% of global capacity for a relevant product, that product would face stricter market access restrictions.

France's CRE published rules in May for the ninth round of ground-mounted PV and agrivoltaic tenders, with a total scale of around 925 MW. The tender introduced supply-chain resilience requirements aligned with the Net-Zero Industry Act for the first time, showing that French PV tenders are moving away from pure price competition toward a framework that weighs price, supply-chain security, and local compliance.

The EU Energy Performance of Buildings Directive also requires member states to complete transposition before May 29, 2026, laying a policy foundation for building PV demand from 2027. But if the range of eligible equipment suppliers narrows and project costs rise, building PV growth could face implementation conflicts with equipment restrictions.

On the financing side, Italy's FER X renewable energy support mechanism, worth about $26.3 billion (EUR 23 billion), was approved, including around 10 GW of PV tenders. The European Investment Bank also approved a new round of clean energy financing to support project development and grid upgrades.

India: ALMM Triggered A Record Rush Before The Market Entered An Adjustment Period

India was the biggest upside surprise in overseas demand in H1 2026. The June 1 implementation of ALMM List-II for cells, fiscal-year-end grid-connection assessments, PM Surya Ghar, agrivoltaic project development, and the rush to connect before transmission charge waivers were reduced all supported installations.

India added 14.4 GW of PV capacity in Q1, almost double the same period last year and a single-quarter record. By the end of March 2026, cumulative PV installations had reached around 152 GW. Utility-scale projects accounted for 85%, while rooftop PV accounted for 15%.

Gujarat and Rajasthan together contributed around 80% of Q1 utility-scale additions. Since its launch in 2024, PM Surya Ghar has driven nearly 10 GW of rooftop PV installations. Together with PM-KUSUM, it forms the policy foundation for India's distributed PV demand.

On policy implementation, India's Ministry of New and Renewable Energy made clear that there would be no blanket extension for ALMM List-II. Exemptions would be granted only through case-by-case review for projects that had already made substantive investment. The extension application window closed on June 30.

As the ban formally entered implementation, the demand pulled forward by early procurement and early grid connection began to show. H2 installation momentum is expected to slow significantly from H1. However, year-end grid-connection demand may still support a gradual monthly recovery.

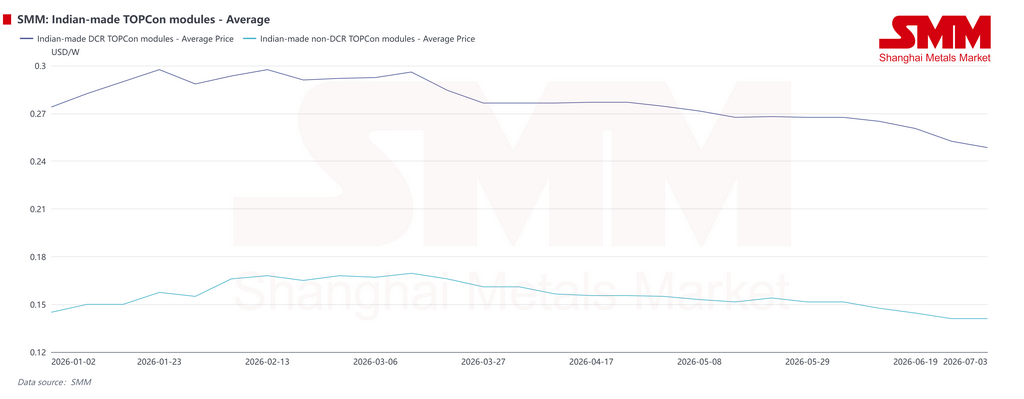

India's local module market is becoming more structurally divided. Non-DCR modules have seen their domestic application scenarios narrow, pushing prices down to around $0.14/W. Remaining projects that can still use ALMM List-I modules are estimated at only around 30 GW, and most must be connected by the end of 2027. More of these products are likely to be absorbed through exports later.

DCR modules still benefit from policy and targeted government project demand. However, limited domestic cell capacity keeps module costs high, raises project LCOE, and compresses power station investment returns. Under the combined pressure of weaker demand and high costs, DCR module prices also moved lower.

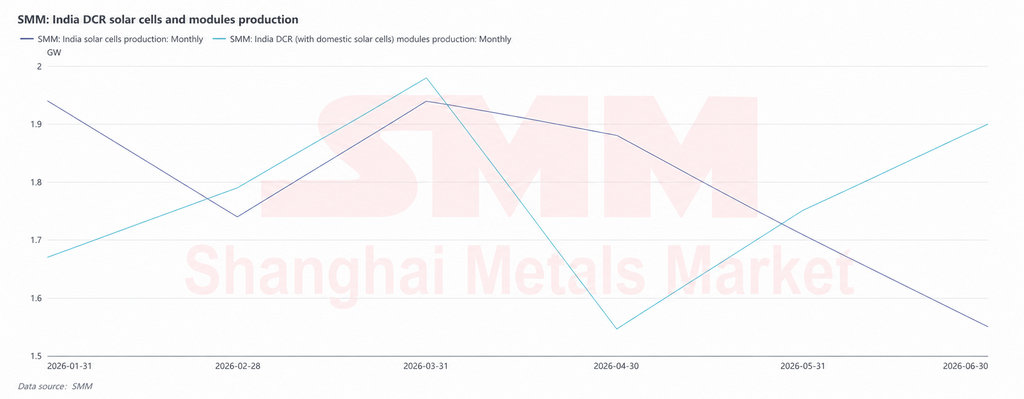

SMM data show that India's DCR module output, including locally made cells, reached around 10.64 GW in H1. Indian cell output totaled around 10.76 GW, broadly matching module output in scale, though monthly production diverged.

In Q1, India's local manufacturing chain maintained high scheduling because of early procurement before ALMM List-II, fiscal-year-end grid-connection assessments, and government-backed projects. DCR module output rose to 1.98 GW in March, the H1 monthly peak.

In Q2, high local cell costs and the price premium of DCR modules over non-DCR products weakened end-project acceptance. Module shipment pace slowed and fed back into upstream cell scheduling. Cell output remained at 1.88 GW in April before falling to 1.71 GW in May and 1.55 GW in June, indicating inventory digestion and order adjustment after earlier high production.

Overall, India's production side in H1 reflected a temporary release driven by policy deadlines rather than sustained demand expansion. After ALMM List-II formally took effect on June 1, the linkage between local cell supply stability, DCR module costs, and project returns will become stronger. H2 module scheduling is expected to adjust dynamically around local cell supply, project exemption progress, government tender timing, and year-end grid-connection demand.

In the medium and long term, India's localization requirements will continue moving upstream. ALMM List-III for wafers is scheduled to take effect on June 1, 2028. Covered projects will then need to meet full-chain localization requirements for both cells and wafers. Given that India started planning wafer capacity relatively early, SMM expects the actual disruption to be limited.

India's medium-term installation outlook remains supported by its 2030 target of around 300 GW and continued local manufacturing policies.

Asia-Pacific: Imports Overtook Europe In March As Demand Drivers Split

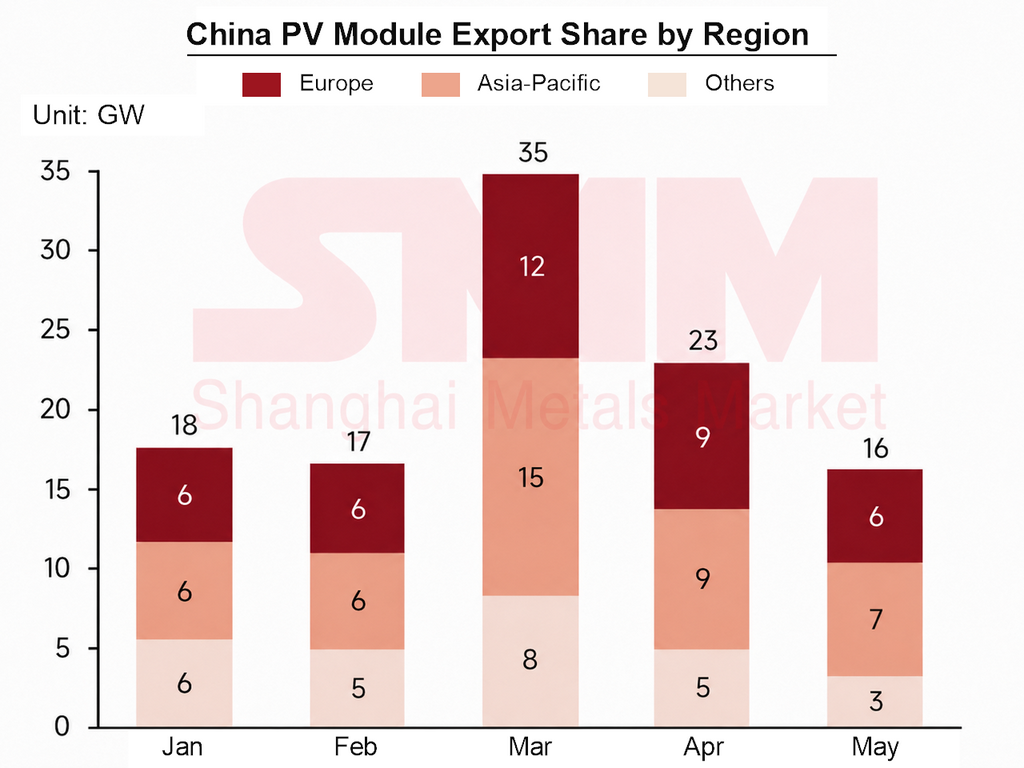

Asia-Pacific's position in China's module export map rose sharply in H1 2026. In March, China's module exports reached a monthly high of 35 GW as shipments were concentrated around the tax rebate window. Asia-Pacific imports overtook Europe for the first time, making the region China's largest module export destination that month.

This structural shift reflected high European channel inventories and a move toward rigid restocking, while many Asia-Pacific markets continued to import on the back of energy transition pressure and high end-user power prices. Asia-Pacific is no longer merely a re-export channel. It is becoming an important end-demand market.

Within the region, Southeast Asia and Pakistan followed different demand logic. Southeast Asia was mainly driven by tenders, quota timing, and policy arrangements. Pakistan was driven more by distributed PV economics and changes to the electricity pricing mechanism.

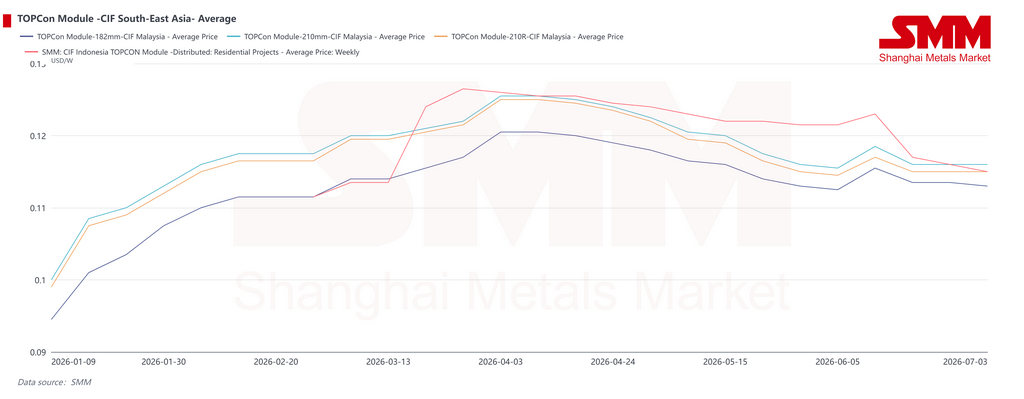

In Southeast Asia, module CIF prices rose early, came under pressure at high levels in the middle of the period, and then eased, allowing some procurement to resume. Q1 price increases were mainly cost-driven. Freight costs rose around the Chinese New Year period, while concentrated shipments during the export tax rebate window tightened shipping capacity and supported higher delivery prices to Malaysia and Indonesia.

In Q2, as CIF prices fell, some demand that had been delayed by high prices began to return. In mid-June, higher shipping costs provided temporary support to CIF prices, but weak overseas end demand limited upside. Second-tier manufacturers cut prices first to secure deals, and leading producers later followed passively, pulling prices lower again in mid-to-late June.

By market, Malaysia saw more active inquiries late in Q2 as some utility-scale projects started, supporting relatively firm prices. Indonesia had already released part of its installation demand in H1, leaving weaker short-term procurement momentum and a larger price decline. Whether Indonesian demand can increase later will depend on the latest July quota arrangements from the power authorities and progress in government-backed project tenders.

Regional policies also advanced in H1. Malaysia's Solar ATAP mechanism officially started on January 1, shifting rooftop PV from net metering to a model based mainly on self-consumption. The corporate installation cap was raised to 100% of maximum power demand. Malaysia also launched a residential PV subsidy plan in May and announced in early June that the sixth round of its large-scale solar program would open within the year. Future projects will be required to include battery storage, showing that utility-scale PV development is shifting from standalone solar plants to solar-plus-storage.

Vietnam's new decree took effect on June 26 and eased surplus power sales restrictions for self-consumption rooftop PV. In some cases, the surplus sales ratio increased from 20% to 50%, improving cash-flow expectations for commercial and industrial rooftop projects.

Indonesia's sovereign investment institution plans to invest in module manufacturing so local capacity can support the country's 50 GW solar target. It is also promoting village PV financing. Cambodia formally removed import tariffs on PV products, while the Philippines accelerated around 1.2 GW of PV projects.

The trade environment became more difficult. US AD/CVD investigations into crystalline silicon PV cells and modules from India, Indonesia, and Laos issued preliminary countervailing duty and anti-dumping determinations in H1. Combined with an anti-circumvention petition involving exports through Ethiopia, trade risks continued to accumulate for Southeast Asia as an export transit and manufacturing base. Overseas application scenarios for regional module capacity are gradually narrowing.

Pakistan: Net Billing Pushes The Market Toward Self-Consumption

Pakistan's core H1 variable was a fundamental adjustment to distributed power pricing. In February, NEPRA issued the 2026 prosumer rules, replacing the decade-old net metering framework with net billing. The grid now buys surplus power at the national average power purchase cost and sells electricity at the retail tariff, ending the one-for-one offset mechanism.

For new users, the surplus power purchase tariff fell from about $0.09/kWh (Rs25/kWh) to around $0.029/kWh (Rs8/kWh), a decline of more than two-thirds. Contract duration was also shortened from seven years to five years. In April, the regulator further amended the rules, confirming that existing users would keep their original billing arrangements during the valid contract period, but system expansion would no longer enjoy the original tariff benefits.

The mechanism change has not altered the market's underlying drivers. By early 2026, Pakistan had imported more than 51 GW of PV modules from China, compared with less than 1 GW in 2018. This represents one of the fastest recorded consumer-led energy transitions.

Imports reached 18 GW in the latest fiscal year alone, and market institutions estimate that actual installed capacity may already be around 33 GW nationwide. Under official figures, grid-connected net-metered capacity is about 7,000 MW, with around 466,000 registered users. Another 13,000-14,000 MW of off-grid systems operate independently.

High power prices and frequent outages remain the fundamental support for Pakistan's PV demand. In H1, the US-Iran conflict increased risks around the Strait of Hormuz and pressured regional energy supply, further highlighting the value of distributed PV as a hedge for Pakistan's energy security.

For module exporters, Pakistan remains a highly price-sensitive market. Low offers were frequent in H1, and the country was one of the main regions where second-tier module manufacturers cut prices early to compete for orders.

Looking ahead, under net billing, surplus power export revenue will shrink sharply. The market focus will shift from export-oriented systems to maximizing self-consumption. Commercial and industrial daytime load scenarios and solar-plus-storage systems should have stronger economics, and storage demand could become a new growth point. However, the impact of the new policy on residential installation willingness, and the possible shift of some demand toward off-grid systems, still need to be monitored in H2.

Overall, Asia-Pacific installation growth is supported by policy targets, green power demand, and distributed PV economics. But Southeast Asian projects still face constraints from financing conditions, power purchase agreement signing, grid access, and approval efficiency. Aging grid infrastructure and capacity saturation in countries such as Vietnam, as well as Indonesia's strict installation quota system, will continue to limit short-term growth. Pakistan still needs to digest the structural demand shift caused by electricity pricing reform.

Whether Asia-Pacific imports can continue to exceed Europe's will depend on Southeast Asian tender delivery in H2 and the resilience of Pakistan's self-consumption demand.

Middle East And Africa: Geopolitical Disruption Weighs On Delivery, But Sovereign Projects Support Longer-Term Growth

In H1 2026, the Middle East and Africa were shaped by both geopolitical disruption and energy transition demand. The US-Iran conflict and periodic risks around the Strait of Hormuz disrupted regional module supply, shipping logistics, and project delivery schedules.

In mid-June, freight costs briefly rose to two to three times previous levels. Shipping costs for PV products headed to Europe and the Middle East increased by about $2,000-3,000 per high-cube container from earlier levels. Some Middle Eastern projects originally scheduled for completion before summer were forced to delay.

As the situation eased at the margin, delayed supply-chain demand may be released if the Strait of Hormuz and surrounding shipping lanes remain open. Chinese module shipments to the Middle East could then recover quickly.

Project pipelines remain supported by sovereign energy strategies. Saudi Arabia announced the qualified bidder list in January for the seventh round of its National Renewable Energy Program, covering four PV projects totaling around 3.1 GW and 2.2 GW of wind projects. In April, Saudi Arabia launched prequalification for a second batch of independent energy storage projects totaling 3 GW/12 GWh.

The previous six tender rounds had awarded more than 12.6 GW of renewable energy capacity. Of Saudi Arabia's 58.7 GW renewable energy target for 2030, 40 GW is PV.

Oman issued prequalification for a 1.5 GW solar IPP at the end of June, with some projects including storage. This shows that large-scale solar-plus-storage projects in the Middle East are accelerating.

In Africa, the World Bank approved $250 million in May to support energy projects in Madagascar. International development finance continues to improve conditions for grids, off-grid power supply, and renewable energy integration across Africa.

In installation structure, the Middle East is dominated by large ground-mounted power plants and solar-plus-storage projects, with Saudi Arabia and the UAE contributing the main increments. Africa combines distributed systems, off-grid systems, and selected utility-scale projects. Markets with stronger grid foundations, such as Egypt, South Africa, and Morocco, are better positioned to advance large projects.

Large power plants that were tendered or signed PPAs earlier are expected to enter concentrated construction and grid-connection phases from 2027 onward. The region's installation center could rise significantly. PV will also increasingly serve green hydrogen, seawater desalination, and the decarbonization of large power loads.

Short-term project delivery remains constrained by multiple factors, including geopolitical risk, shipping lane stability, financing costs, exchange-rate volatility, sovereign credit, and the payment capacity of power utilities. The medium- and long-term growth certainty of the Middle East and Africa remains strong, but short-term installation release still carries high uncertainty.

Outlook: H2 Demand May Recover, But Price Pressure Remains

Overall, H1 2026 overseas PV prices and demand were driven more by policy windows, cost disruption, and regional project deadlines than by a comprehensive improvement in end demand. Q1 module price increases were supported by the export tax rebate transition, export rush and inventory-building, higher freight costs, and manufacturers' price support strategies.

In Q2, as policy disruption faded, the market returned to demand-led pricing. Manufacturers cut prices gradually to secure orders under half-year shipment pressure, and the module price center moved lower.

Regional divergence was the clearest structural feature of H1. India's policy-driven installation rush pulled forward part of H2 demand. Europe faced both inventory digestion and compliance review, with utility-scale projects still affected by negative power prices and grid-connection constraints. Southeast Asia is still waiting for tenders, quota arrangements, and government-backed projects to materialize. Pakistan has entered a demand structure adjustment phase after electricity pricing reform. The Middle East and Africa face short-term delivery disruption from geopolitics and shipping schedules, but medium-term sovereign project pipelines remain supportive.

In H2, overseas PV grid connections may fall temporarily in July and August because of summer holidays, high temperatures, and slower project construction in some regions. From September, demand is expected to recover as holidays end, project execution resumes, and tender results, quota arrangements, and policy exemptions are gradually implemented. Q4 demand should improve under year-end grid-connection assessments and policy deadlines.

However, overall order intake is still likely to remain under pressure. Some demand was already pulled forward in H1. Overseas inventories still need to be digested. India is entering a policy adaptation period. Some emerging-market projects are still moving slowly from planning to execution.

Key variables to track include EU mature project recognition before the November inverter-related deadline, the direction of related cybersecurity rule revisions, India's ALMM implementation and domestic cell capacity release, Indonesia's Q3 quota arrangements and government project tenders, the Middle East situation and the stability of Strait of Hormuz traffic, and the pass-through of freight and exchange-rate changes into landed costs.

On prices, China export module prices are expected to remain under pressure as module cost pressure eases, overseas end-demand recovery remains limited, and manufacturers continue to face shipment pressure. At the same time, the stronger renminbi against the US dollar and euro in H1 compressed exporters' foreign-exchange gains and profit margins. Some manufacturers have limited willingness to make further large price concessions, which should provide partial support to export offers. SMM expects China export module prices in H2 2026 to fluctuate narrowly under pressure, with the price center still facing downside risk.

Written by:

Ryan Tey Tze Yang | SMM PV Analyst

+60 127179370 | ryan.tey@metal.com

![PV frame demand underpins steady operations; short-term aluminum prices consolidate on a strong note [SMM Analysis]](https://imgqn.smm.cn/usercenter/DCwfK20251217171737.jpg)

![Silver Consolidated in an N-Shape and Closed Flat This Week, as Geopolitics and Rate Hike Expectations Waged a Tug-of-War [SMM Silver Weekly Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)

![[Solar: LONGi partners with DHL to develop global solar and storage projects]](https://imgqn.smm.cn/usercenter/FqtWa20251217171742.jpg)