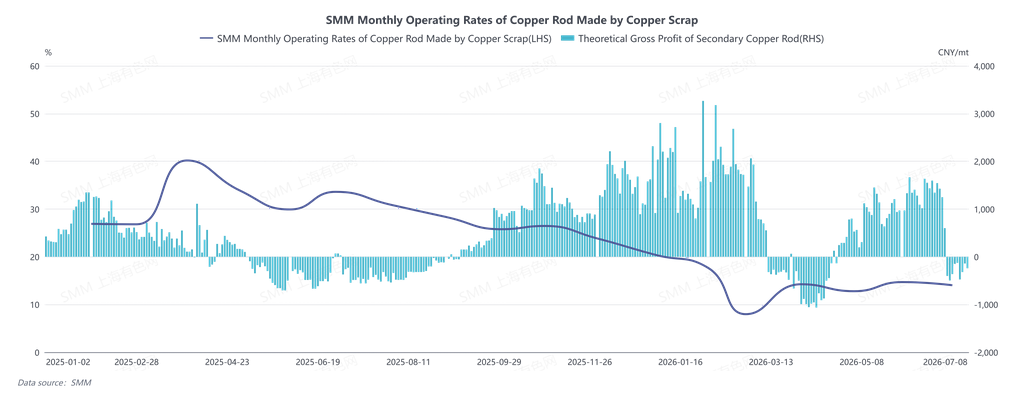

In June 2026, the operating rate of secondary copper rod was 14.04%, below expectations of 14.23%, down 0.66 percentage points MoM and down 19.57 percentage points YoY. In June, the secondary copper rod market operated under three main themes: the full-scale implementation of reverse invoicing compliance inspections, copper prices repeatedly testing the 100,000 mark, and the early timing of the Dragon Boat Festival holiday. The entire month exhibited a deadlock characterized by weak supply and demand, regional divergence, and thin trading, with the core contradiction shifting from copper price fluctuations to a structural supply-demand mismatch under compliance invoice constraints. The supply side was deeply suppressed by reverse invoicing compliance requirements. Weekly operating rates fluctuated between 13.05% and 20.55% throughout the month, still down 3.57-15.98 percentage points YoY. Enterprises in areas such as southern Jiangxi (Ji'an and Fengcheng) and Hubei suspended production on a large scale due to compliance inspections, while Shuyang in Jiangsu began restricting reverse invoicing quotas from June. Many enterprises cut output due to insufficient invoices. Compliant tax-included copper scrap that could be invoiced remained persistently tight. Regional divergence was pronounced: supply was relatively ample in the north, while spot availability was tight in the south, giving rise to a structural tight balance where shaft furnace rod was in undersupply. Supported by resilient raw material prices, secondary copper rod shifted from a discount to a premium against copper futures throughout the month. The average price difference between copper cathode rod and secondary copper rod narrowed continuously from 1,372 yuan/mt at the beginning of June to 563 yuan/mt at month-end. The discount of secondary copper rod in Jiangxi against futures shrank from 973 yuan/mt to 13 yuan/mt. Weekly gross profit from sales fluctuated between 1,178 yuan/mt and 1,512 yuan/mt, but stability was extremely poor. Enterprises mostly scheduled production based on their compliance capabilities and cash flow, not daring to increase output. On the demand side, it was suppressed by three factors: copper prices defending the 100,000 mark, premiums on secondary copper rod, and the early arrival of the high-temperature off-season.

End-user wire and cable enterprises generally held a wait-and-see expectation of waiting for copper prices to fall below 100,000 yuan/mt before purchasing, with procurement dominated by rigid demand in pulses. When the price difference between copper cathode rod and secondary copper rod narrowed to an extremely low 340-660 yuan/mt, they almost stopped procurement, mostly switching to shaft furnace rod to maintain production. Before the Dragon Boat Festival, they only made small-scale rigid-demand stockpiling and showed no willingness to stockpile. Throughout the month, apart from sporadic rigid demand when copper prices fluctuated, transactions were almost flat with no highlights.

Looking ahead to July, whether the market stalemate can be broken depends on two key points: first, the smoothness of implementation after the new reverse invoicing regulations take effect—if compliance standards are clear and input invoices and tax-inclusive raw material supply recover marginally, the tight supply of billable goods on the supply side is expected to ease; second, whether copper prices can break below the 100,000 yuan/mt level, releasing pent-up procurement demand from end-users. If both show positive signals, after the economic viability of secondary copper rod is restored, transactions may marginally improve. However, the high-temperature off-season officially starts in July, and end-user orders themselves are weak. If the policy is not straightened out in a timely manner and copper prices continue to hold above 100,000 yuan/mt, the supply-demand weak pattern will persist, and secondary copper rod may remain at a premium to copper futures, with thin trading.

![End-use consumption struggles to improve, and secondary copper rod enterprises mainly rely on just-in-time procurement [SMM Secondary Copper Daily Review]](https://imgqn.smm.cn/usercenter/FERSF20251217171712.jpg)