In H1 2026, the overseas bauxite market was generally characterized by high shipment levels, growing imports, a year-on-year decline in prices but a recovery within the year, stronger policy disturbances, and rising energy and freight costs. In particular, escalating geopolitical tensions in the Middle East pushed up oil prices and dry bulk freight rates, becoming an important cost-side factor supporting Guinea bauxite CIF China prices. On the supply side, bauxite shipments from Guinea’s major ports maintained significant year-on-year growth, making Guinea the core source of overseas bauxite supply increments. Australian shipments were generally stable, although local weather disruptions in March caused a temporary decline in shipments from major ports. In terms of domestic import structure, as June customs import data by country has not yet been released, this article mainly observes import changes from January to May 2026. Data shows that domestic bauxite imports continued to grow year-on-year during January-May 2026, with the source structure becoming increasingly concentrated in Guinea.

On the price side, imported bauxite prices in H1 2026 were significantly lower than the same period in 2025, but prices did not continue to decline throughout the year. Since March, escalating geopolitical tensions in the Middle East have pushed up international oil prices and dry bulk freight costs, leading to a significant increase in Guinea bauxite CIF China prices. Around the Labour Day holiday and again in mid-to-late June, market rumours repeatedly suggested that the Guinean government might introduce bauxite export quota-related policies. Although no such policies were officially implemented within the expected timeframe, these rumours disrupted the transaction pace between buyers and sellers and provided support to forward price expectations. At the same time, after the Chinese New Year holiday, imported bauxite raw material inventories at domestic alumina refineries remained at elevated levels, while port inventories of imported bauxite continued to accumulate after March and throughout H1, limiting further upside in spot prices.

Overall, the overseas bauxite market in H1 2026 did not face an absolute shortage. Instead, it showed a pattern of relatively loose physical supply but tightening expectations from costs and policy risks. High Guinean shipments supported arrivals of imported bauxite in the domestic market, but the high concentration of domestic import sources in Guinea also made the market more sensitive to Guinean policy changes, rainy-season shipment disruptions, freight rate fluctuations, and changes in long-term contract prices.

Price: Still Low YoY, but CIF Prices Recovered in Stages During the Year

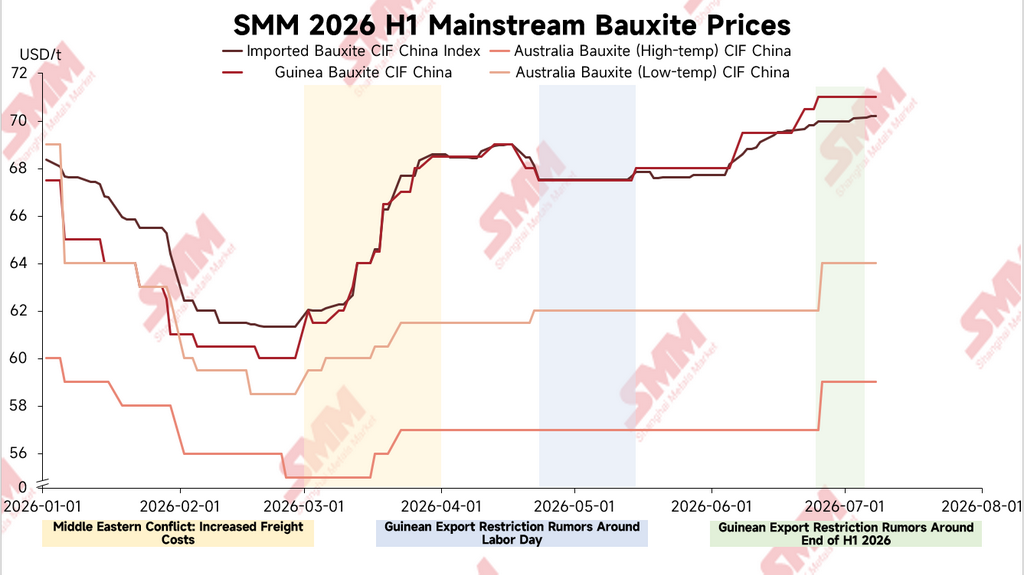

According to SMM data, in January-June 2026, the average SMM Imported Bauxite CIF Index stood at around $66.37/mt, down around 26.0% from the same period in 2025. The average Guinea bauxite CIF China price was around $65.88/mt, down around 25.8% year-on-year. The average Australia high-temperature bauxite CIF China price was around $56.93/mt, down around 23.0% year-on-year. The average Australia low-temperature bauxite CIF China price was around $61.63/mt, down around 24.1% year-on-year. From a year-on-year perspective, imported bauxite prices in H1 2026 remained significantly below the same period last year.

However, from an intra-year perspective, imported bauxite prices first declined and then recovered. In early January, the SMM Imported Bauxite CIF Index was around $68.35/mt, while Guinea bauxite CIF China was around $67.5/mt. By late February, Guinea bauxite CIF China had once fallen to around $60/mt. After entering March, rising oil prices and freight costs amid escalating geopolitical tensions in the Middle East pushed up the landed cost of Guinea bauxite delivered to China. On March 2, Guinea bauxite CIF China was around $62/mt; by March 20, it had risen to $66.5/mt, and by the end of March it further increased to $68.5/mt.

It is worth noting that in March, the increase in Guinea CIF prices was significantly greater than the change in FOB prices. SMM data shows that Guinea bauxite FOB was around $37.5/mt on March 2, rose to $38.5/mt on March 20, and remained near $38.5/mt at the end of March. Over the same period, the Guinea CIF-FOB spread widened from around $24.5/mt to around $30/mt. Overall, the March increase in Guinea CIF prices was not entirely driven by mine-side quotations. Freight rates, energy costs, trading premiums, and forward supply risk expectations all provided support to landed prices.

From late April to early May, the market heard rumours that the Guinean government might announce bauxite export quota-related policies during the Labour Day holiday. As a result, transaction activity between buyers and sellers slowed significantly, and the market turned cautious. In terms of price performance, Guinea bauxite CIF China remained largely stable at around $67.5/mt between April 24 and May 8, while the SMM Imported Bauxite CIF Index also stayed near $67.52/mt. Prices mainly moved sideways and did not break out significantly. As no related policy was officially introduced during the Labour Day period, market transactions gradually recovered in mid-May, and Guinea bauxite CIF China edged up to around $68/mt.

Entering June, Guinean policy expectations once again disturbed the market. Around the Dragon Boat Festival, market rumours again suggested that the Guinean government might introduce export quota-related policies between mid-June and early July. At the same time, market participants were waiting for the release of July long-term contract prices, causing buyers and sellers to turn cautious again. In terms of prices, Guinea bauxite CIF China rose from around $68/mt in early June to around $69.5/mt in mid-June, and further increased to around $71/mt by the end of June. For Guinea monthly long-term contract prices, the price stood at $67/mt in January 2026, fell to $62/mt in February, rebounded to $63/mt in March, remained at $70/mt from April to June, and further increased to $71/mt in July. The firm long-term contract price also provided certain support to the spot market.

Shipments: Guinea Maintained High Growth, while Australia Saw a Temporary Weather-Related Decline in March

Due to the limited disclosure frequency of overseas mine production data, this article uses weekly shipments from major ports as a reference indicator for observing overseas bauxite exportable supply trends. For monthly comparison, all monthly shipment data mentioned in this article is calculated by allocating weekly shipment data to corresponding months based on the proportion of calendar days.

According to SMM statistics, in January-June 2026, bauxite shipments from Guinea’s major ports totalled around 115.1357 million mt, up around 26.5% from the same period in 2025. By month, shipments from Guinea’s major ports increased by around 40.2% YoY in January, 35.1% YoY in February, 28.7% YoY in March, 31.5% YoY in April, 10.9% YoY in May, and 13.5% YoY in June. Overall, Guinean shipments remained high in H1 and continued to serve as the main source of overseas bauxite supply growth.

In terms of shipment structure, high Guinean shipments reflected continued release of mine and port export capacity, while also supporting high arrivals of imported bauxite in the domestic market. At the same time, Guinea’s rising share in the domestic import structure means that the market has become increasingly sensitive to local policy changes, weather conditions, port operations, and shipping conditions.

For Australia, bauxite shipments from major ports totalled around 21.6586 million mt in January-June 2026, down around 3.7% year-on-year. Overall performance was relatively stable, but its incremental supply elasticity was weaker than Guinea’s. Australia’s shipments fell notably in March, mainly due to local weather disruptions and related natural events. Weekly data shows that Australian bauxite shipments from major ports declined significantly during March, with shipments from Weipa falling to a low level in late March. After entering April, shipments from Australia’s major ports recovered quickly. This indicates that the weather disruption had more of a temporary impact on shipments rather than representing a sustained supply contraction.

Import Structure: Domestic Imports Grew YoY in January-May, with Guinea’s Dominance Further Strengthened

On the import side, as June customs import data by country has not yet been released, this article mainly observes domestic bauxite import changes in January-May 2026. According to customs data, domestic bauxite imports totalled around 100.7579 million mt in January-May 2026, up around 18.6% from 84.9571 million mt in the same period of 2025.

By country, domestic imports from Guinea reached around 82.5716 million mt in January-May 2026, up around 24.9% from 66.1231 million mt in the same period of 2025. Guinea accounted for around 82.0% of total domestic bauxite imports, up from around 77.8% in the same period last year. This shows that Guinea remained the largest source of domestic imported bauxite, while its dominance in the import structure further strengthened.

Australia remained the second-largest source of domestic bauxite imports. In January-May 2026, domestic imports from Australia stood at around 14.4914 million mt, up around 8.2% from 13.3929 million mt in the same period of 2025. However, Australia’s share of total domestic bauxite imports stood at around 14.4%, lower than around 15.8% in the same period last year. Overall, Australian supply remained stable, but its share in the domestic import structure was significantly lower than Guinea’s, and its short-term incremental supply elasticity was relatively limited.

Among non-mainstream sources, domestic imports from Sierra Leone reached around 1.0353 million mt in January-May 2026, marking a significant year-on-year increase. Imports from Guyana reached around 747,200 mt, up slightly year-on-year, while imports from Türkiye reached around 559,100 mt, down significantly year-on-year. Overall, non-mainstream sources provided supplementary supply in certain months, but in terms of supply scale, stability, quality compatibility, and logistics conditions, they remain unable to substantially replace Guinea in the short term.

From a monthly perspective, domestic bauxite imports remained high in January-May 2026. Imports stood at around 19.2528 million mt in January, 16.9530 million mt in February, 21.7789 million mt in March, 19.7433 million mt in April, and further increased to around 23.0298 million mt in May. May imports were at a high level, with imports from Guinea reaching around 19.6074 million mt and imports from Australia around 3.0259 million mt. High Guinean shipments in earlier periods and continued demand for imported ore from domestic coastal alumina refineries jointly supported import growth.

Inventory and Transactions: High Inventories Suppressed Spot Procurement, while Policy Expectations Disrupted Transaction Pace

In terms of inventories, according to SMM surveys, imported bauxite raw material inventories at domestic alumina refineries remained at elevated levels after the Chinese New Year holiday. Meanwhile, after geopolitical tensions in the Middle East escalated in March, domestic port inventories of imported bauxite continued to accumulate throughout H1. With relatively sufficient inventory buffers, downstream alumina refineries had limited acceptance of high-priced spot cargoes. Procurement was mainly conducted on a need-to basis, while some enterprises preferred to observe policy changes, freight rates, and long-term contract price movements before restocking.

High inventories also explain a key contradiction in price movements during H1. On the one hand, geopolitical tensions in the Middle East pushed up energy and freight costs, while repeated Guinean policy expectations disturbed market sentiment and supported imported bauxite prices. On the other hand, elevated inventories at alumina refineries and ports meant that spot procurement did not see sustained concentrated buying, and acceptance of high-priced cargoes remained limited, thereby restricting further price upside.

Around the Labour Day holiday, the market heard rumours that the Guinean government might announce bauxite export quota-related policies during the holiday period. Transactions between buyers and sellers weakened significantly, and the market entered a wait-and-see mode. As no related policy was officially introduced within the expected timeframe, market transactions gradually recovered after mid-May, but prices only saw a mild recovery. In mid-to-late June, the market again heard rumours that Guinea might introduce quota-related policies between mid-June and early July. Together with uncertainty around July long-term contract prices, transaction activity became cautious again. Therefore, the impact of Guinean policy expectations in H1 2026 was reflected more in transaction pace and price expectations, rather than simply driving a sustained rapid increase in spot prices.

Major Events: Cost Disturbances, Australian Weather, and Guinean Policy Expectations Ran Through H1

The major events in the overseas bauxite market in H1 2026 can be divided into three main lines.

First, escalating geopolitical tensions in the Middle East in March pushed up oil prices and dry bulk freight costs, driving a rapid recovery in Guinea bauxite CIF China prices. As the Guinea-China route is long, freight rate movements have a significant impact on landed costs. From March to June, Guinea-China bauxite freight rates remained high, once rising to around $36/mt, and fluctuated within a high range. At the same time, persistently high oil prices also pushed up transportation and export costs at Guinean mines. Some mines faced pressure on export margins, and market feedback suggested that some mines reduced shipments in stages or controlled shipment pace during May-June to ease cost pressure.

Second, Australia saw a temporary decline in shipments from major ports in March due to local weather disruptions. After allocating weekly shipment data to months based on calendar days, Australian bauxite shipments from major ports stood at around 2.5339 million mt in March, down around 38.8% year-on-year. Among them, shipments from Weipa fell notably in late March. Shipments recovered quickly after entering April, indicating that the disruption was more of a short-term event and had limited impact on the full-year supply structure.

Third, Guinean export quota policy expectations repeatedly disturbed the market. Around the Labour Day holiday, market rumours suggested that the Guinean government might announce export quota-related policies, leading to weaker transactions and sideways price movements. However, no such policy was eventually introduced, and market transactions gradually recovered after mid-May. In mid-to-late June, the market again heard rumours that the Guinean government might introduce quota-related policies between mid-June and early July. Together with the pending release of July long-term contract prices, prices again remained firm. Although the policy has not yet been officially implemented, the market has become significantly more sensitive to such news amid the high dependence of domestic imported bauxite on Guinea.

Full-Year Outlook: Guinean Policy Risk and Freight Cost Disturbances Continue to Support Forward Price Expectations

Looking ahead to H2 2026, the core contradiction in the overseas bauxite market is expected to continue revolving around Guinean policy changes, rainy-season shipments, and freight cost fluctuations. If shipments from Guinea’s major ports remain relatively stable as seen in early July, and Guinea-China freight rates continue to fall, imported bauxite supply is still expected to remain relatively sufficient. Domestic alumina refinery and port inventories may also remain elevated, limiting further upside in spot prices.

However, on the risk side, current market rumours still suggest that the Guinean government may introduce bauxite export quota-related policies in H2 2026. If such policies are officially implemented and impose substantial constraints on local mine shipment schedules, Guinean bauxite supply elasticity may be affected, thereby supporting imported bauxite prices. Meanwhile, as Guinea gradually enters its traditional rainy season, mining, inland transportation, and port loading may all face temporary disruptions. Based on historical rainy-season performance, Guinean shipments may decline in certain months, affecting domestic arrival schedules and port inventory digestion.

In terms of freight rates, Middle East developments still showed potential for volatility in early July, and the previous easing expectations still require further observation. If geopolitical risks rise again, oil prices and dry bulk freight costs may increase once more. Guinea-China bauxite freight rates may rebound from the current range of around $30-32/mt to $36/mt or even higher, pushing imported bauxite CIF prices higher again. Conversely, if the Middle East situation continues to ease and oil prices and freight rates decline further, Guinea-China freight rates may fall below $30/mt. In that case, some Guinean mines that previously reduced shipments or controlled shipment pace may resume shipments, and market transaction activity may recover.

On prices, overseas bauxite prices in H2 are expected to remain constrained on both the upside and downside. On the upside, elevated raw material inventories at domestic alumina refineries and port inventories will limit acceptance of high-priced spot cargoes. If actual supply does not shrink significantly, the momentum for a sustained sharp price increase may be limited. On the downside, Guinean policy expectations, rainy-season disruptions, freight volatility, long-term contract price support, and import source concentration risks all mean that imported bauxite prices lack the basis for a sharp decline.

In H2 2026, the market needs to closely monitor whether Guinean export policies are officially implemented, the actual impact of the rainy season on local mines and port shipments, Guinea-China freight rate movements, July and subsequent long-term contract price adjustments, and domestic port inventory digestion. If Guinean shipments remain high and port inventories continue to accumulate, the upside elasticity of imported bauxite prices may remain limited. However, if policy implementation tightens, rainy-season disruptions exceed expectations, or freight rates rise again, Guinea bauxite CIF China prices may still receive periodic support.

Conclusion

Overall, the overseas bauxite market in H1 2026 was characterized by high shipments, growing imports, a year-on-year price decline but intra-year recovery, and stronger policy disturbances. Guinean shipments increased significantly year-on-year, supporting high domestic bauxite import volumes. Australian shipments recovered after a temporary weather-related decline in March, and overall supply remained relatively stable. In terms of import structure, domestic bauxite imports increased by around 18.6% year-on-year in January-May 2026. Among them, imports from Guinea increased by around 24.9% year-on-year, with its share rising further to around 82.0%, indicating that domestic imported bauxite reliance on Guinea continued to increase.

On the price side, imported bauxite prices in H1 2026 were significantly lower than the same period in 2025. However, prices recovered during the year amid geopolitical tensions in the Middle East, rising oil and freight costs, Guinean export quota policy expectations, and long-term contract price support. At the same time, elevated raw material inventories at alumina refineries after the Chinese New Year holiday and continued port inventory accumulation after March limited further upside in spot prices.

Looking ahead, the overseas bauxite market does not lack absolute supply, but the supply structure is highly concentrated. Price volatility is increasingly driven by policy, logistics, freight, and risk premiums rather than a simple supply-demand gap. In H2, Guinean policy implementation, rainy-season shipments, freight rate movements, long-term contract price adjustments, and domestic port inventory digestion will be key factors affecting overseas bauxite prices and import structure changes.

![SHFE Aluminum Rises Amid Position Reductions, Short-Term Recovery; Alumina Rebound Limited [SMM Aluminum Briefing]](https://imgqn.smm.cn/usercenter/GEsWk20251217171650.jpg)

![East China purchasing sentiment strengthens, central China futures and spot traders' purchasing demand rises [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/SUuNM20251217171651.jpg)