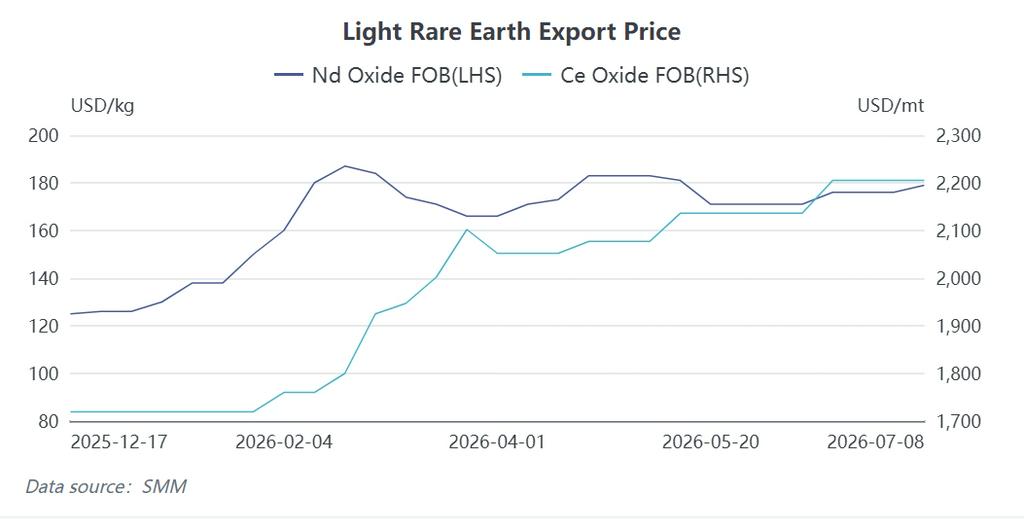

1.. Light Rare Earths: Stable Supply and Volume Growth

Light rare earths faced minimal export friction, with approvals averaging 30 days. This allowed consistent supply to meet global demand from EVs, wind energy, and catalysts.

-

Cerium Oxide: Prices rose 28% to $2,205/ton. Volumes surged 67% YoY as overseas polishing and automotive demand remained firm.

-

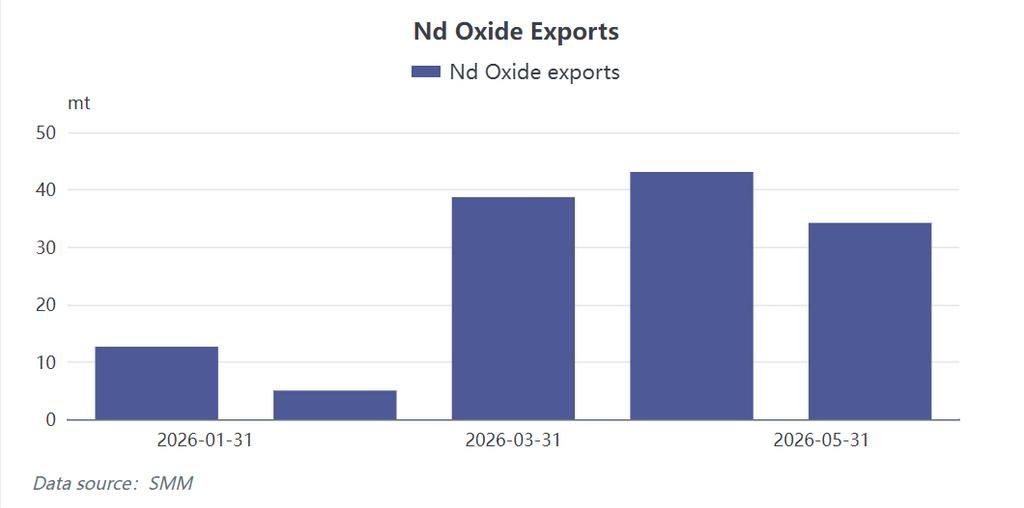

Neodymium Oxide: Prices stabilized near $183/kg. After a February dip due to holidays, exports normalized above 35 tons/month, up 26% YoY.

-

Driver: Fast approvals ensured overseas essential demand was met without significant price distortion.

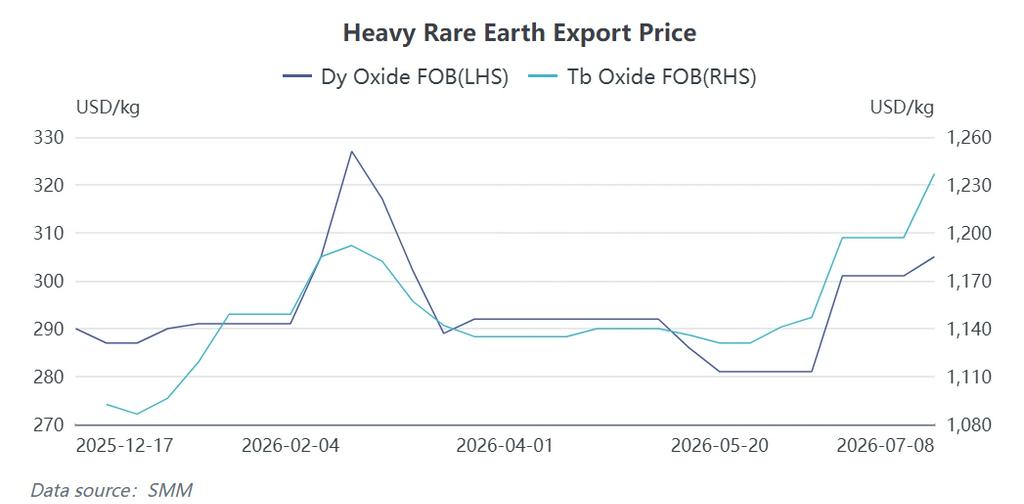

2. Heavy Rare Earths: Policy-Driven Premiums

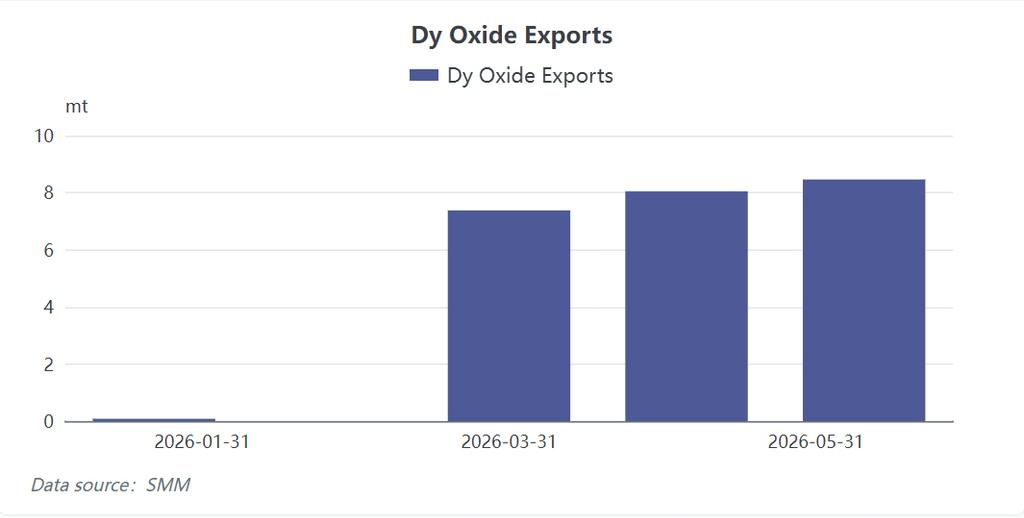

Heavy rare earths faced strict licensing, resulting in a 30–40% price premium over domestic Chinese levels. Export volumes fell sharply (Dy/Tb down ~60% YoY).

-

Pricing: Dysprosium Oxide averaged $312/kg (+34% YoY); Terbium Oxide averaged $1,120/kg (+41% YoY).

-

Geopolitical Split: Licenses for high-performance magnets to Japan remained nearly closed. Only the US, EU, and Southeast Asia saw limited approvals.

-

Outlook: The current high prices reflect regulatory scarcity, not physical shortages. If controls tighten post-November, premiums may exceed 50%.

3. Offshore Supply Chain Development

To mitigate reliance on China, Western nations advanced domestic projects, though progress is currently limited to light rare earths.

-

US: Allocated $1.2B in subsidies and completed the acquisition of Vacuumschmelze to secure a domestic magnet supply chain.

-

ASEAN: Lynas and JS Link initiated a 3,000-ton/year magnet plant in Malaysia, utilizing Australian ore and securing feedstock until 2038.

-

OEM Shift: Automakers like Toyota are increasingly importing finished motors from China rather than raw magnets, altering traditional trade flows.

H2 2026 Outlook

Two factors will dictate market direction:

-

Demand Validation: Monitoring if Q3 production schedules for EVs and appliances converts into sustained magnet demand, rather than just preemptive restocking.

-

Policy Expiry: The November 10 deadline. An extension maintains the status quo; a tightening risks severe supply shocks, particularly for Japanese manufacturers.

![Semiconductor market bucks the trend! Minor metals sector up nearly 3%, with Yunnan Tin and Yunnan Germanium leading the gains [SMM Flash]](https://imgqn.smm.cn/usercenter/xLlnY20251217171724.jpeg)