Futures market: In June, the most-traded cast aluminum alloy contract initially fell before rebounding overall. At the start of the month, it moved sideways around the 23,300 yuan/mt level, briefly rebounding to 23,705 yuan/mt in mid-month, before quickly pulling back under the weight of bearish sentiment in the nonferrous metals sector, falling to a low of 22,315 yuan/mt at month-end. Entering July, the earlier decline gradually recovered, and with cost support emerging, futures prices rebounded consecutively, reclaiming the 23,000 yuan/mt level and approaching the 60-day moving average.

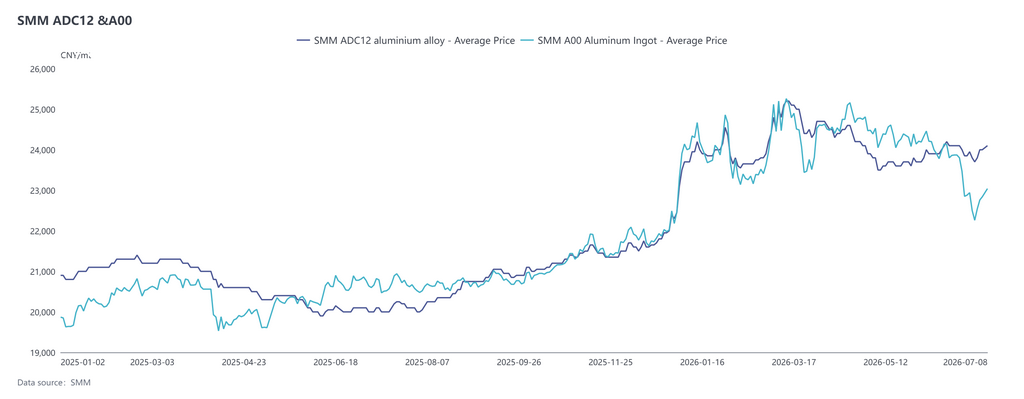

Spot market: In June, ADC12 generally strengthened initially before stabilizing, then pulled back slightly at month-end, with its price center higher than in May. After rising consecutively to 24,200 yuan/mt in early June, it moved sideways in a narrow high range; in late June, prices weakened but the decline was significantly smaller than that of primary aluminum, with the price spread against A00 rapidly widening to over 1,000 yuan/mt, a record high for the same period in history. Entering July, prices remained resilient. As of July 8, SMM ADC12 was quoted at 24,100 yuan/mt, up a cumulative 400 yuan/mt from early June. In June, ADC12 generally strengthened initially before stabilizing, then pulled back slightly at month-end, with its price center higher than in May. After rising consecutively to 24,200 yuan/mt in early June, it moved sideways in a narrow high range; in late June, prices weakened but the decline was significantly smaller than that of primary aluminum, with the price spread against A00 rapidly widening to over 1,000 yuan/mt, a record high for the same period in history. Entering July, prices remained resilient. As of July 8, SMM ADC12 was quoted at 24,100 yuan/mt, up a cumulative 400 yuan/mt from early June.

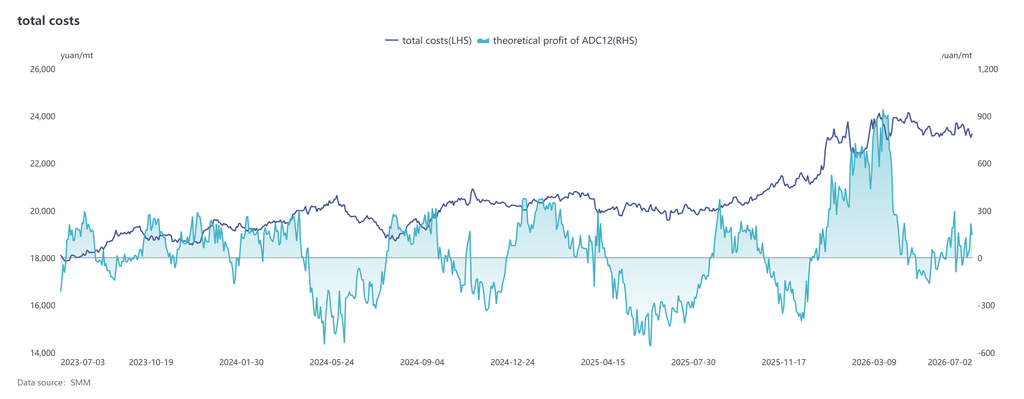

Cost side, according to the latest SMM data, the theoretical total cost for the ADC12 industry in June 2026 rose 0.5 percentage points MoM to 23,419 yuan/mt. From January to June, the theoretical total cost increased 14.1 percentage points YoY to 23,326 yuan/mt, with the industry's theoretical profit per metric ton at around 285 yuan. Breaking down the costs, aluminum scrap costs were approximately 21,086 yuan/mt, accounting for 90.4%; copper costs were 851 yuan/mt, accounting for 3.6%; and silicon costs were 485 yuan/mt, accounting for 2.1%. Among these, the cost shares of aluminum scrap and copper continued to rise, while silicon costs kept pulling back.

Since entering July, the price difference between A00 aluminum and aluminum scrap narrowed to a new low in recent years. Some enterprises have begun trying to purchase primary aluminum to ease the pressure of aluminum scrap procurement, but this has not yet formed an industry-wide substitution trend. This move is essentially a passive response to the shortage of compliant aluminum scrap, rather than A00 aluminum already offering clear cost advantages. If aluminum scrap remains tight and aluminum prices fall further, it is not ruled out that enterprises will continue to increase the blending ratio of primary aluminum.

Demand side, the traditional off-season characteristics became more evident in June: the automotive industry saw a slowdown in production and sales, die-casting companies faced order pressure, and secondary aluminum demand remained persistently weak. In sectors such as motorcycles, demand was relatively stable, and some export orders saw slight incremental growth due to improved price spreads between Chinese and overseas markets; however, overall gains were limited, and orders continued to contract. Entering July, the off-season combined with end-user high-temperature holidays left the demand side still sluggish, continuing to cap price upside room.

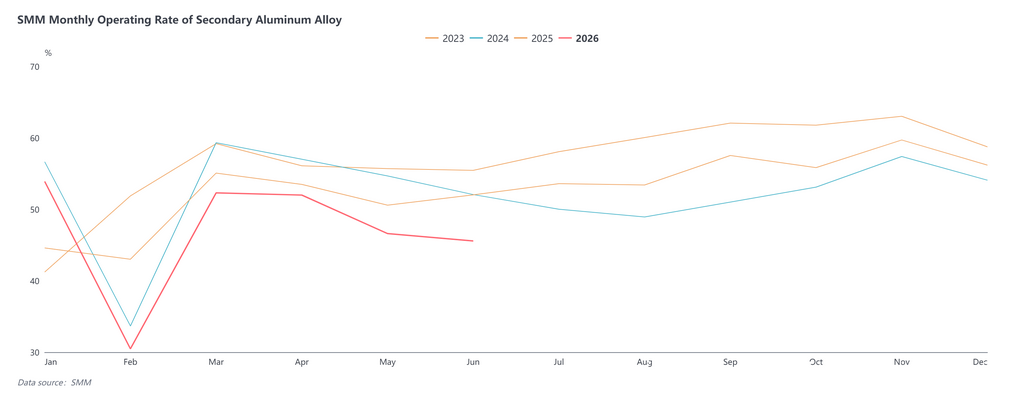

Supply side, the operating rate of the secondary aluminum alloy industry was 45.6% in June, down 1.0 percentage point MoM and 6.5 percentage points YoY, with production falling to the lowest level of the year excluding the Chinese New Year month. The decline in the operating rate continued in June, mainly due to raw material shortages and insufficient demand. Given that production had already dropped significantly in May, the room for further decline in June was limited, and the MoM decline narrowed somewhat. Meanwhile, the YoY drop was relatively large, mainly because in the same period last year, cast aluminum alloy futures were newly listed, prompting futures and spot traders to enter the market in a concentrated manner to purchase aluminum alloy ingots at low prices during the off-season, which inflated the production base of secondary aluminum plants. Entering July, although off-season demand persists and policy constraints remain, the industry's production has already contracted sharply, leaving limited room for further decline. At the same time, the price spread between A00 and ADC12 has widened significantly, and an increasing number of enterprises are considering increasing primary aluminum purchases to address issues such as invoice shortages and difficulty in purchasing aluminum scrap, in order to secure supply. Although the overall scale of substitution is limited, it is expected to provide some support for producers' operations, and the operating rate has the potential for a modest rebound.

Looking ahead to July, the secondary aluminum alloy market is expected to continue the pattern of “cost support but demand suppression.” ADC12 prices will likely stay in a narrow sideways range, with the estimated trading band at 23,500-24,500 yuan/mt. Downside support comes from three factors: First, tax policy is unlikely to loosen in the short term, so aluminum scrap raw materials remain highly resistant to declines and compliance costs stay high, providing a solid cost-side floor. Second, industry operating rates and social inventory have both dropped to year-to-date lows, keeping spot circulation tight. Third, the import window remains closed, limiting supplementary supply from outside China. Resistance on the upside mainly comes from the demand side — July is still in the traditional consumption off-season, with slow order recovery for automotive and other end-users, and a lack of downstream momentum to chase prices higher or restock, making it hard to form an effective uptrend driver. In sum, ADC12 prices have limited downside room and also lack demand cooperation to break higher, so the overall movement will still be dominated by sideways consolidation.

In terms of price spread, the current spread between ADC12 and A00 has widened to above 1,000 yuan/mt. Considering that the logic of aluminum scrap cost support will hardly change in the short term while primary aluminum is more disturbed by the macro front, ADC12’s relative resistance to declines versus A00 will persist, and the spread between the two is expected to stay high. Going forward, focus on three key variables: first, the recovery pace of aluminum scrap supply and the marginal impact of tax policy changes on the cost side; second, whether downstream orders can show substantial improvement signals before the peak season starts in H2; and third, the transmission of SHFE aluminum directional fluctuations to market sentiment.

![East China purchasing sentiment strengthens, central China futures and spot traders' purchasing demand rises [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/SUuNM20251217171651.jpg)