In H1 2026, the aluminum scrap market faced the dual pressures of tightening policies and weak demand, which weighed on production growth. Coupled with falling primary aluminum prices, an early indicator of a "high opening, low ending" pattern for the year had already emerged.

1. Price Difference Between Primary Aluminum and Scrap

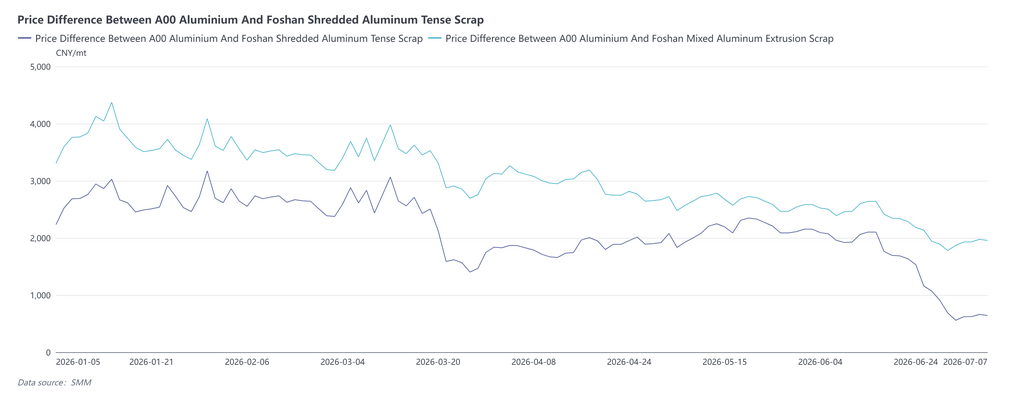

In H1 2026, the primary-scrap price difference went through four phases: starting at lows, rapidly widening, consolidating at highs, and then sharply narrowing, falling to a multi-year low by end-June.

Phase 1: The price difference was at a relatively low level at the start of the year, with the Shanghai machinery aluminum tense scrap spread ranging between 2,267 and 2,690 yuan/mt. Before Chinese New Year, downstream enterprises gradually entered their holiday break, terminal restocking willingness was low, and the market was marked by "prices without substantial trading."

Phase 2: After the holiday, scrap yards gradually resumed operations. Coupled with the US-Iran geopolitical conflict driving up primary aluminum prices sharply, A00 aluminum prices surged from around 23,100 yuan/mt to 25,590 yuan/mt. Aluminum scrap followed the uptrend but at a slower pace, causing the primary-scrap price difference to widen passively. On March 12, the Shanghai machinery aluminum tense scrap spread hit its H1 peak of 3,848 yuan/mt, while the aluminum extrusion scrap spread reached 3,338 yuan/mt.

Phase 3: Primary aluminum prices pulled back from highs. Scrap aluminum, affected by policy compliance requirements, saw tighter supply of invoiced material and thus declined by a smaller margin, allowing the price difference to gradually narrow from elevated levels. Moreover, during the "Golden March and Silver April" peak season, demand fell short of expectations, and downstream scrap utilization enterprises mainly purchased as needed.

Phase 4: In late June, A00 aluminum prices accelerated their decline, but scrap aluminum showed resilience due to cost support from the reverse invoicing policy, resulting in a rapid narrowing of the price difference. As of July 7, the Shanghai machinery aluminum tense scrap spread stood at 2,080 yuan/mt, and the aluminum extrusion scrap spread had narrowed to 1,588 yuan/mt. Some cast aluminum alloy producers had already begun to consider substituting A00 aluminum ingots for scrap.

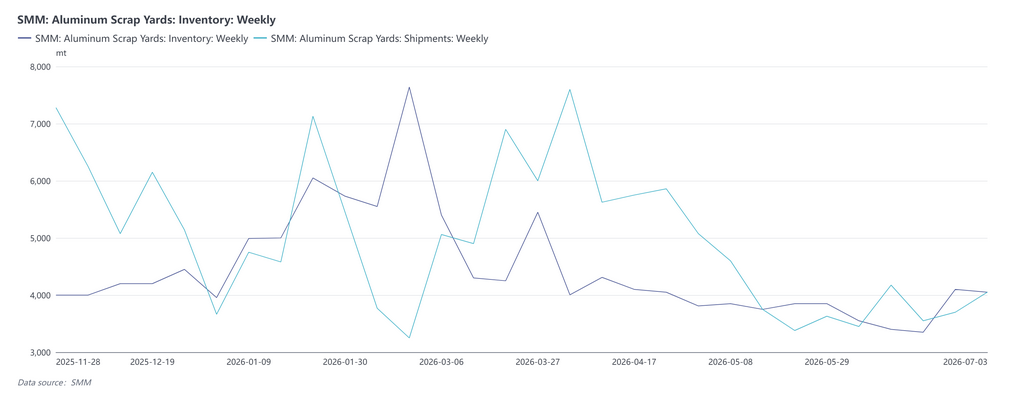

2. Scrap Yard Inventories and Warehouse Withdrawals

At the start of the year, after environmental protection-driven production restrictions were lifted in central China, inventories of wrought aluminum scrap approached saturation. However, downstream enterprises had extremely low willingness to stockpile due to high aluminum prices, and some planned to shut down early. The overall domestic scrap market showed resistance to high prices and a "price without market" situation, with scrap yard withdrawals continuing to decline alongside downstream production cuts. Around the Chinese New Year period, scrap yards and scrap utilization enterprises gradually closed for the holiday. Outbound shipments were completely suspended, with only a small amount of delayed arrivals contributing minor inbound volumes, and market trading activity was nearly frozen.

After the holiday, as scrap yards fully resumed operations, the release of supply increased somewhat. Downstream restarts accelerated, and restocking demand was slowly released. However, constrained by the reverse invoicing policy, overall trading remained relatively sluggish, with withdrawals dominated by small, need-based orders. Meanwhile, at high aluminum prices, scrap yards held back from selling, and warehouse inflows rose with climbing scrap production, causing social inventories to shift from destocking to accumulation. Following the crackdown on invoice-related irregularities and the tightening of the reverse invoicing policy, YoY inflows at mainstream yards in some regions declined, and inventories showed a mild buildup trend. In contrast, inventories of aluminum tense scrap actually decreased. Over the same period, downstream sectors entered the traditional consumption off-season. Operating rates at scrap utilization enterprises stayed low, end-user orders lacked momentum, and the procurement pace turned more conservative.

3. Policy

Since the "reverse invoicing" policy was rolled out in 2025, its enforcement was continuously tightened in H1 2026, but local implementation standards diverged significantly — regulatory oversight was relatively stringent in Anhui, Jiangxi, Hubei, and other regions. Some provinces saw the cancellation of tax refunds and intensified tax audits. Shandong also saw reports that reverse invoicing would be suspended from July, with the overall tax burden reaching up to 10.5%. This policy environment has directly led to persistently high tax compliance costs in the aluminum scrap recycling segment. Moreover, under the invoice-based economy norms, traders' invoicing quotas generally declined, causing a structural shortage of compliant invoiced scrap cargoes and notably tightening aluminum scrap liquidity. For scrap utilization enterprises, the impact has propagated along a chain of "tighter raw materials/rising costs — production cuts/suspensions — substitution risks": first, rising prices of invoiced raw materials directly pushed up procurement costs; subsequently, many small and medium-sized scrap utilization enterprises in regions such as Anhui, Jiangxi, and Hubei suffered losses and cut or suspended production; ultimately, the price difference between primary metal and scrap narrowed rapidly to historical lows as aluminum scrap held firm while primary aluminum fell, sharply eroding the cost advantage of scrap over primary aluminum. Some cast aluminum alloy enterprises are already considering using A00 aluminum ingots to replace aluminum scrap in production, posing a risk that the market demand base for aluminum scrap could be eroded.

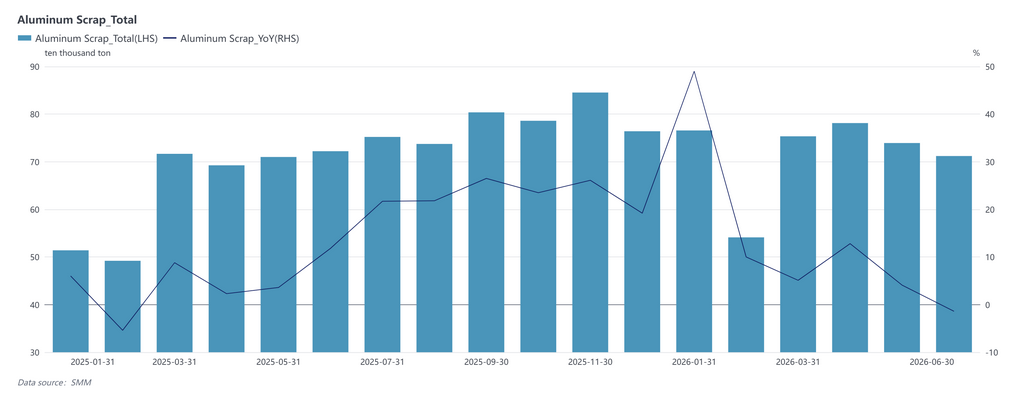

4. Aluminum Scrap Production

In terms of total volume, China's cumulative aluminum scrap production in January-June 2026 was 4.2928 million mt, up approximately 11.58% YoY from 3.8472 million mt in the same period of 2025. January production stood at 765,700 mt, surging 48.97% YoY, primarily due to the later Chinese New Year, leading to far more effective production days than the same period last year, coupled with front-load orders caused by the phase-out of auto industry policies. Affected by the Chinese New Year break, February production seasonally pulled back to 541,200 mt, but still grew by 10% YoY. March-April entered the traditional peak season, with production rebounding to 753,400 mt and 781,200 mt, posting YoY growth of 5.14% and 12.81%, respectively. The peak of the season was in April, and capacity release and the pace of work resumption remained normal. However, May production pulled back to 739,300 mt, with YoY growth narrowing to only 4.13%, indicating that the squeeze from the reverse invoicing policy on small and medium-sized scrap utilization enterprises began spreading from isolated cases to a broader scale. This trend accelerated in June, as production further dropped to 712,000 mt, turning negative YoY at -1.4% and down 3.69% MoM from May, making it the only month in H1 with negative YoY growth. The key reasons for the June decline were: the rising compliance costs caused by the reverse invoicing policy had already driven many small and medium-sized scrap utilization enterprises in Anhui, Jiangxi, Hubei, and other areas into losses and production cutbacks, while the price spread between primary metal and scrap narrowed to historical lows, sharply diminishing the cost advantage of aluminum scrap. This dampened collection enthusiasm and caused a supply contraction at the source. Therefore, beneath the surface of "total volume growth but a front-loaded, then decelerating pace" in H1 aluminum scrap production, the reality is that the policy shock is rapidly transmitting from the cost side to the supply side, and the downward pressure on H2 production cannot be underestimated.

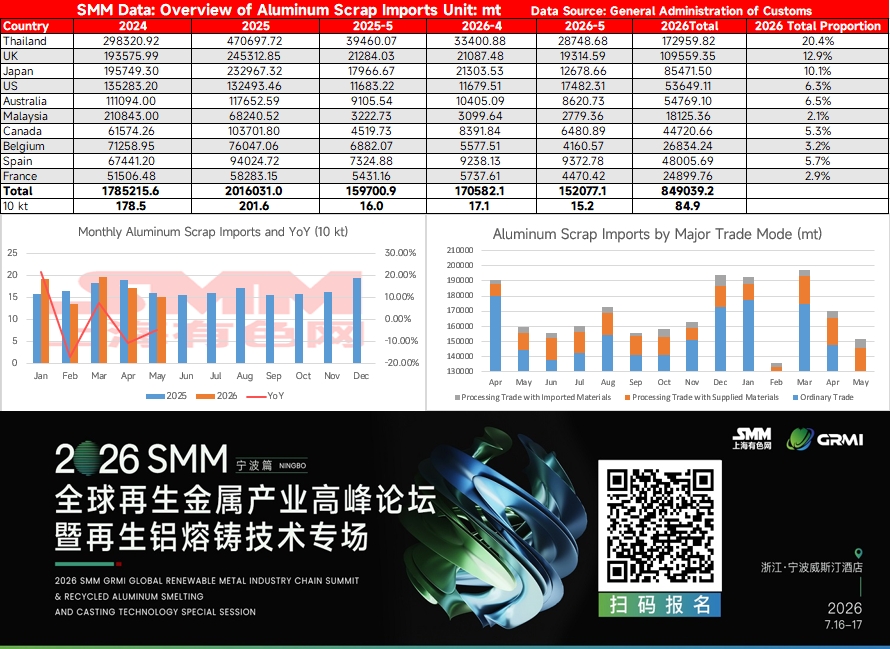

5. Aluminum Scrap Imports

China’s cumulative aluminum scrap imports from January to May 2026 stood at approximately 849,300 mt, edging down 0.84% YoY from 856,500 mt in the same period of 2025. On the surface, the total volume was almost flat, but the monthly trend showed a pronounced “high-then-low” pattern, and the driving force shifted from ample overseas supply in Q1 to a combination of multiple bearish factors in Q2. Q1 cumulative imports grew 3.9% YoY, with Thailand as the largest source country maintaining steady shipments. At the beginning of the year, relatively ample overseas aluminum scrap supply and active stockpiling by domestic secondary aluminum enterprises together supported the high imports. Entering Q2, the situation took a sharp turn for the worse: April imports were 171,000 mt, down 10.4% YoY, and May imports further dropped to 152,000 mt, down 4.8% YoY and 10.9% MoM, forming a contraction pattern of declining volumes and prices. The bearish factors behind this were multidimensional and mutually reinforcing. First, the US-Iran geopolitical conflict drove LME aluminum prices sharply higher, and overseas spot aluminum scrap prices rose accordingly. The overall landed cost for domestic import traders was significantly higher than domestic aluminum scrap prices, and the persistent inversion of the price spread between Chinese and overseas markets directly dampened procurement enthusiasm. Second, high energy prices in Europe intensified competition among local secondary aluminum enterprises for aluminum scrap raw materials, and shipments to China from traditional source countries such as the UK, Spain, Belgium, and France all pulled back to varying degrees. A more far-reaching impact came from policy tightening in exporting countries: the UAE imposed a four-month temporary ban on aluminum scrap exports starting June 3, and the EU also plans to impose an additional 15% tariff starting September. Both factors tightened the availability of high-quality scrap in the Asian region from both immediate and expected aspects. In addition, aluminum scrap imports typically have a shipping lead time of 1-3 months. The significant reduction in purchases by traders in Q2 will be reflected in landing data in Q3, creating a “lagged impact.” Overall, although the total imports from January to May only edged down slightly, the driving structure has reversed from “stable volumes and rising prices” in Q1 to “declining volumes and prices” in Q2. Moreover, the contraction in overseas supply has only just begun to materialize, and the import outlook for H2 faces greater downward pressure.

6. H2 Outlook

The aluminum scrap market is expected to continue consolidating on a subdued note in H2, but with significant bottom support. The price difference between primary metal and scrap has narrowed to a historic low, and the reverse invoicing policy constraint continues to establish a floor for aluminum scrap prices. If primary aluminum prices stabilize and rebound, there is room for a slight recovery in the spread, but the extent is limited; if primary aluminum continues to decline, the substitution effect of aluminum scrap will materialize at a faster pace, putting further pressure on the spread, and an extreme scenario of price inversion between scrap and primary aluminum may even emerge. The reverse invoicing policy is unlikely to see substantive easing in the near term, and the tightness of compliant, invoiced supply is expected to persist. Close attention should be paid to the policy implementation standards in newly joined provinces such as Shandong, changes in local tax inspection intensity, and whether there will be a window for optimizing and adjusting policy details. Overall, the core tension in the aluminum scrap market in H2 remains the tug-of-war between "supply contraction driven by policy tightening" and "consumption weakness caused by sluggish demand." Close attention also needs to be paid to progress in US-Iran negotiations and navigation conditions in the Strait of Hormuz, the pace of aluminum scrap arrivals from outside China and enforcement of the UAE ban, the compliance progress pace of the reverse invoicing policy and differences in local implementation, changes in aluminum ingot inventories, and when the inflection point for secondary aluminum alloy ingot inventory will appear.

[Data source statement: Data other than public information is derived from public information, market communication, and SMM's internal database models, processed by SMM for reference only and does not constitute decision-making advice.]

![East China purchasing sentiment strengthens, central China futures and spot traders' purchasing demand rises [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/SUuNM20251217171651.jpg)