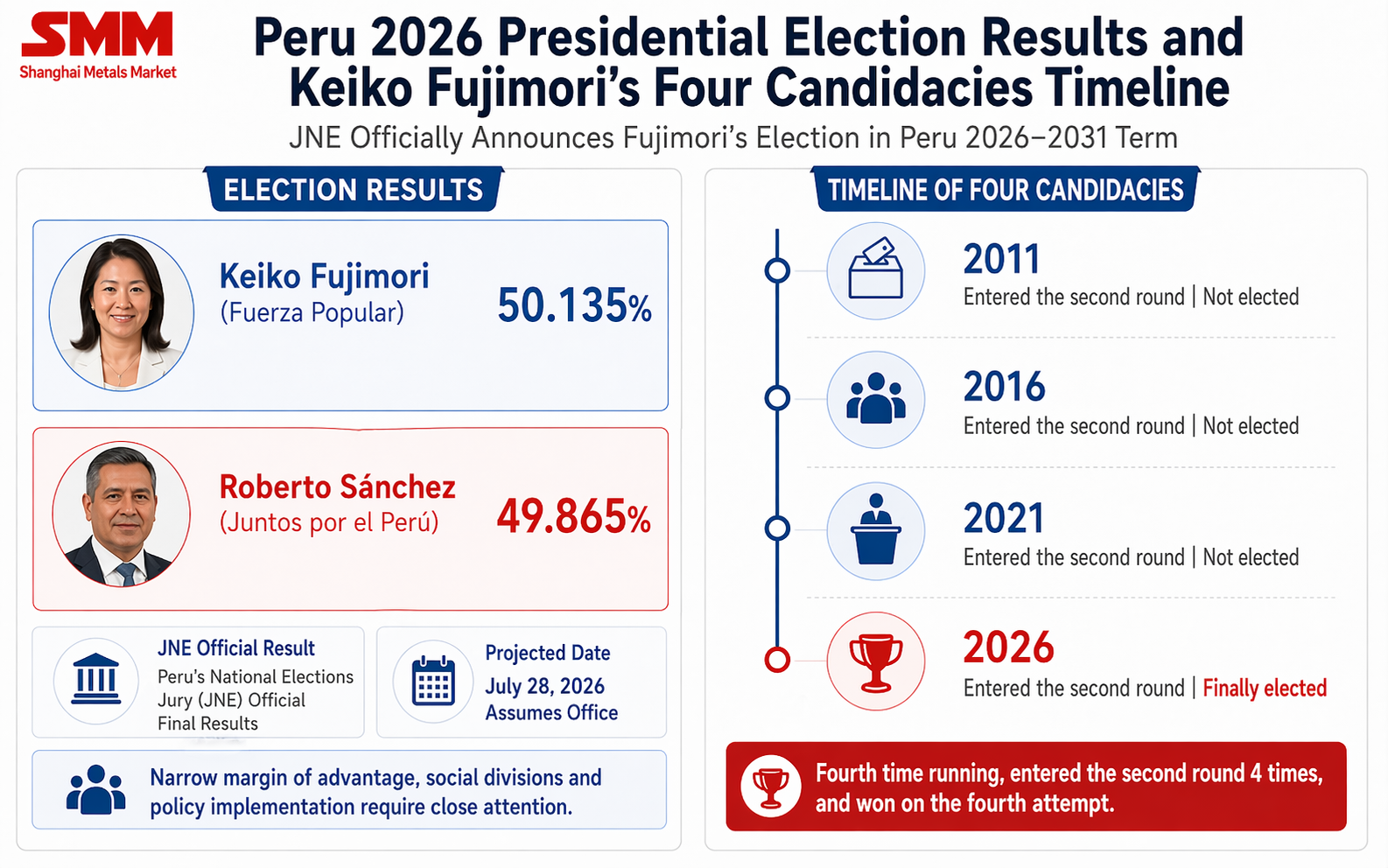

I. Fujimori's Victory and Policy Background

Peru's National Jury of Elections (JNE) has officially announced that Keiko Fujimori, candidate of the People's Force Party (Fuerza Popular), has been elected President of Peru for the 2026–2031 term and will be sworn in on July 28. According to foreign media reports, Fujimori defeated left-wing candidate Roberto Sánchez in the second round with 50.135% to 49.865% of the vote, a margin of approximately 50,000 votes.

Keiko Fujimori is the eldest daughter of former Peruvian President Alberto Fujimori and the leader of the right-wing People's Force Party. She previously ran for president in 2011, 2016, and 2021, reaching the second round each time but failing to win; the 2026 election marks her fourth candidacy and first victory. Her father's administration gained support from some for combating insurgent groups and stabilizing the economy, yet it has long been controversial due to human rights and corruption issues, making Keiko Fujimori a highly influential yet deeply polarizing political figure in Peru.

For the copper industry, the focus of this change in government is not short-term mine production changes, but whether the new administration can improve Peru's long-standing problems in project execution. Peru does not lack copper resources or project pipelines; what truly hinders supply release is the permitting cycle, infrastructure, community relations, illegal mining governance, and local execution capacity.

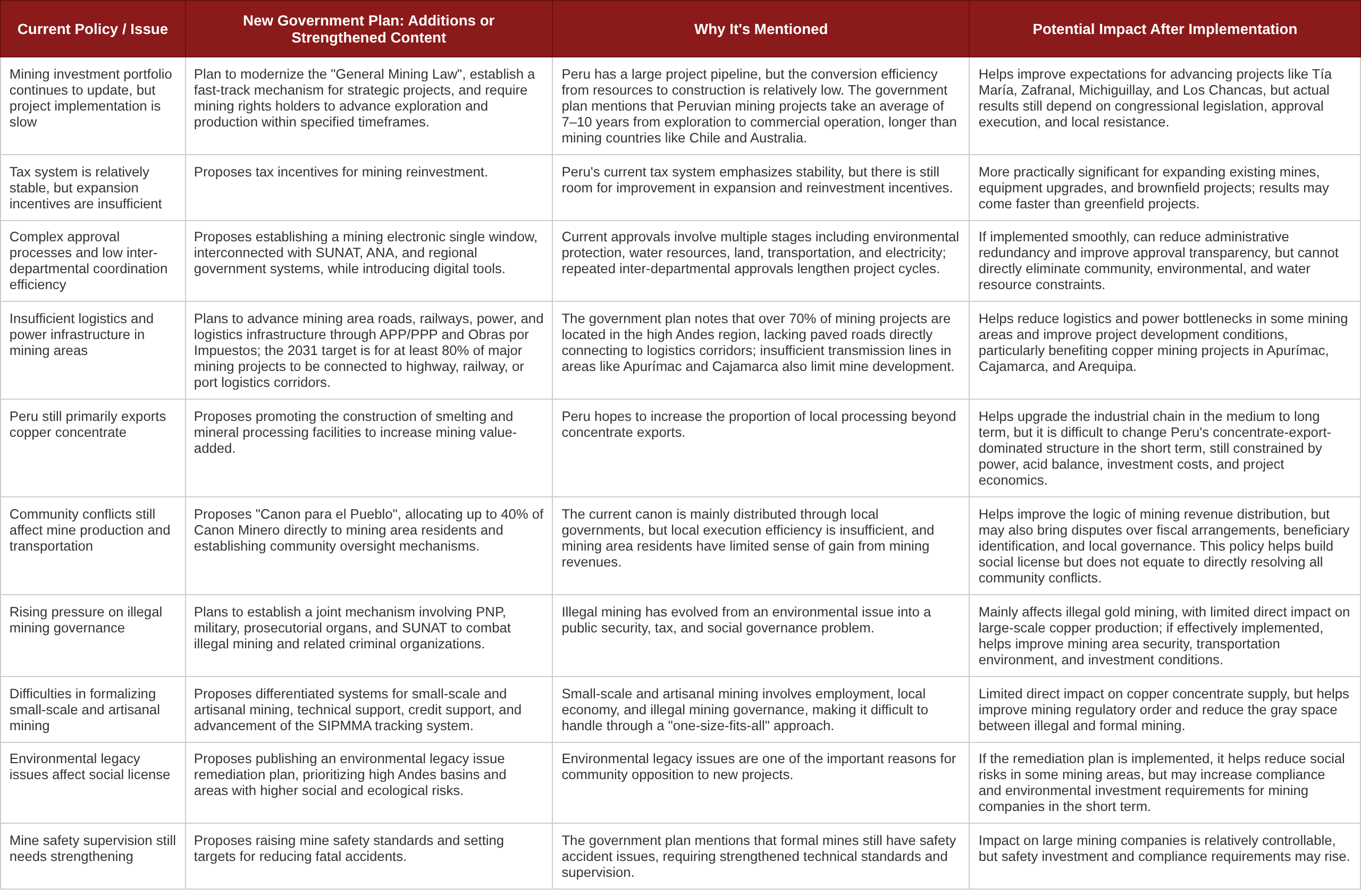

According to the "Plan de Gobierno 2026–2031: Perú con Orden" released by Fuerza Popular, its mining policy priorities include modernizing the General Mining Law, establishing a fast-track mechanism for strategic projects, introducing tax incentives for mining reinvestment, improving mining area infrastructure through APP/PPP and Obras por Impuestos, promoting the construction of smelting and processing facilities, establishing a single electronic window for mining, strengthening illegal mining governance, advancing MAPE formalization, remediating environmental legacy issues, and proposing that up to 40% of the Canon Minero be directly distributed to residents in mining areas. These items remain government plans for now, and their subsequent implementation will depend on legislation, administrative execution, and local governance coordination.

II. Core Differences Between Current Policy and the New Government's Plan

Compared to current mining policies, the Fujimori government's plan does not alter Peru's fundamental direction of relying on mining investment to drive economic growth, but rather shifts the emphasis from "project pipelines" to "project execution." Previously, Peru's policy focus already included attracting investment, maintaining tax stability, updating the mining investment portfolio, and promoting the development of large projects; the new government's plan places greater emphasis on accelerating approvals, mining area infrastructure, reinvestment incentives, illegal mining governance, and revenue redistribution.

Therefore, the new policy is not about redesigning Peru’s mining system, but about addressing the insufficient implementation efficiency of the existing system.

Source: Fuerza Popular’s “Plan de Gobierno 2026–2031: Perú con Orden” mining chapter; compiled by SMM.

III. Short-Term Production Recovery, but Project Delivery Remains Key

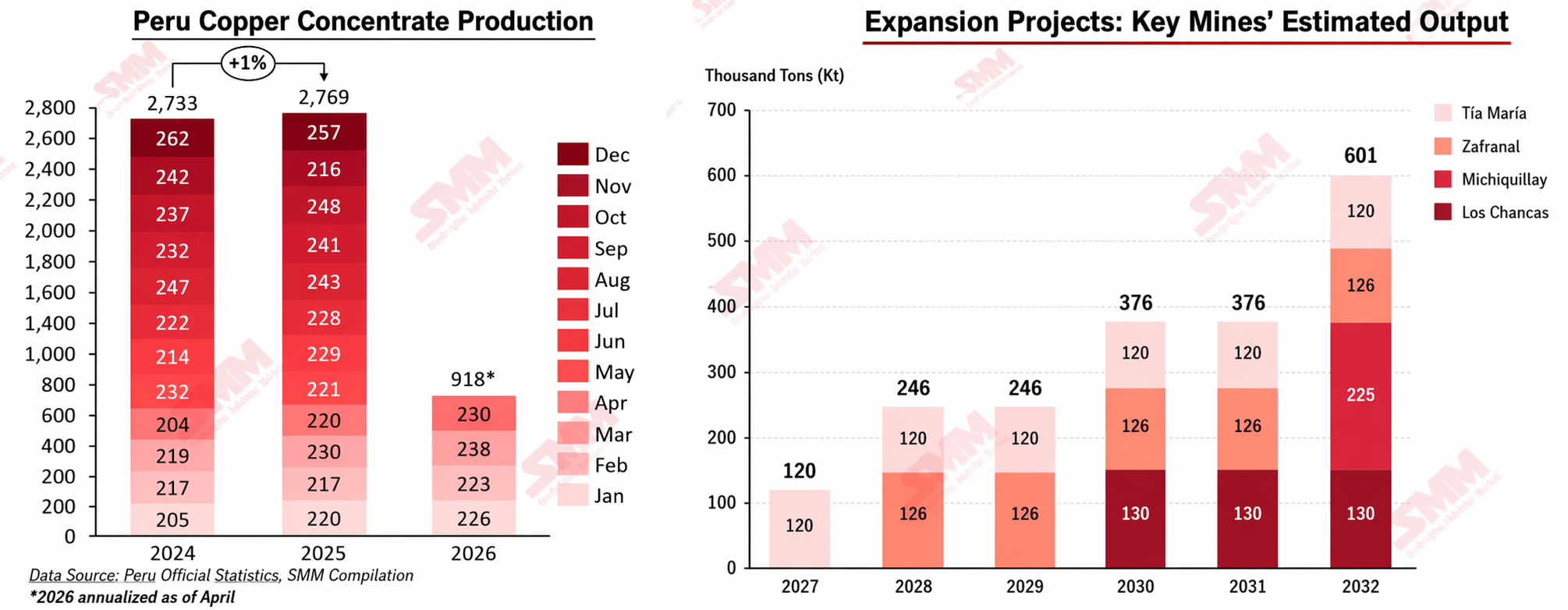

Peru’s copper mine output has stayed high overall in recent years but with limited growth elasticity. Peru’s copper concentrate production was approximately 2.733 million mt in 2024, rising to 2.769 million mt in 2025, a YoY increase of only about 1.3%. From a monthly production perspective, Peru’s copper concentrate output in the first four months of 2024–2026 showed a gradual rise. Output in the first four months was about 845,000 mt in 2024, increased to 887,000 mt in the same period of 2025, and further rose to 918,000 mt in the first four months of 2026, up approximately 3.5% YoY from the 2025 period and about 8.6% from the 2024 period. This indicates that Peru’s near-term copper ore supply still possesses certain recovery and growth capacity. However, from an annual and medium-to-long-term perspective, the first-four-month production improvement does not mean that project reserves have already been converted into stable new supply. Existing mine production schedules, grade changes, maintenance pace, transportation conditions, and the ramp-up of some projects can all affect monthly output performance.

From a project perspective, the new government’s mining plan has a certain relevance to projects such as Tía María, Zafranal, Michiquillay, Los Chancas, La Granja, and the Antamina expansion, but the impact pathways differ. The core issues for Tía María remain community relations and project execution. Policy support for mining investment helps improve the project advancement environment, but its construction pace still depends on local acceptance, construction arrangements, and regulatory enforcement. Projects such as Zafranal, Michiquillay, Los Chancas, and La Granja rely more on approvals, financing, engineering progress, and infrastructure support. If the fast track mechanism, mining electronic single window, and mine infrastructure plans can be implemented, it will help improve the development conditions for these projects. The Antamina expansion is more in line with the logic of extending life and expanding production at existing mines. Compared to greenfield projects, reinvestment tax incentives, improved approval efficiency, and infrastructure upgrades may have a more effective impact on such brownfield projects. Overall, the new government’s plan does not directly bring additional copper output, but rather improves the transformation conditions for projects to move from “planned capacity” to “actual production.” If the policies are implemented smoothly, they will first influence project expectations and corporate investment decisions, and then gradually ripple through to construction progress and actual supply release. The pace of production delivery for different projects will still depend on their respective development stages and the specific constraints they face.

IV. The Core Constraints on Copper Ore Supply Remain Unchanged

Although the new government plans to propose multiple measures centered on approval efficiency, infrastructure, and the investment environment, the release of copper ore supply in Peru still faces multiple practical constraints. First, community relations remain a critical variable for advancing large projects. Road blockades, benefit distribution, water resources, and employment demands could still affect mine construction, operations, and the transport of copper concentrates. Second, policy implementation requires legislative, administrative, and local execution. Even with clear direction from the central government, measures such as mining law amendments, fast-track mechanisms, and Canon redistribution still require specific institutional arrangements and local cooperation. Third, environmental approvals, water resource management, and infrastructure construction remain practical bottlenecks for developing large copper mine projects. Approval processes can be optimized, but projects must still meet requirements for environment, water use, land, and social licenses. Additionally, the natural decline of mines will continue to constrain production growth. Some of Peru's main copper mines have entered a more mature stage of extraction, where declining ore grades, increasing stripping difficulties, and diminishing marginal output at aging mines will make it harder to sustain or increase production. This means that even if the policy environment improves, Peru will still need to rely on new project commissioning and existing mine expansions to offset the pressure from aging mine declines.

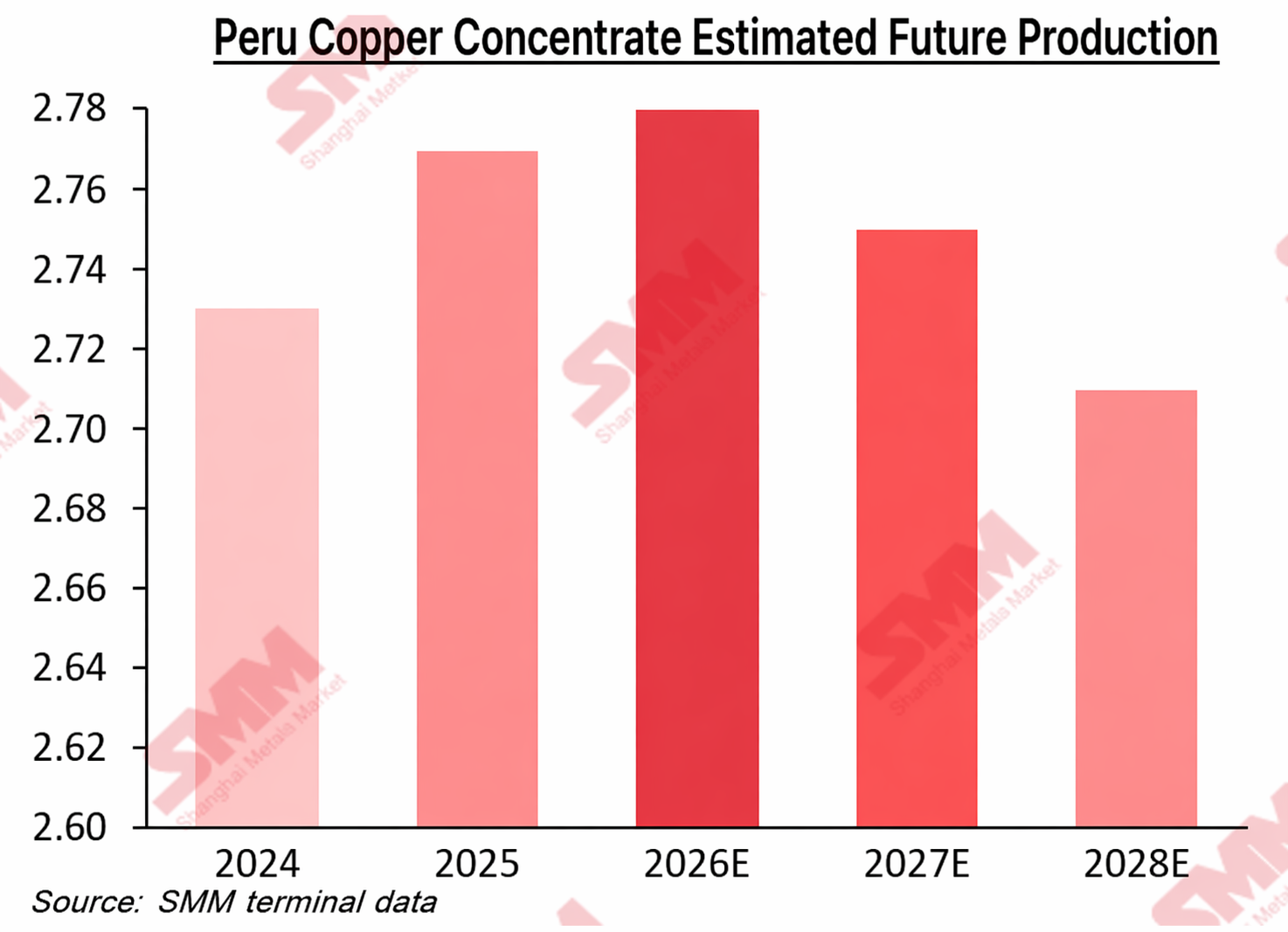

From SMM production forecasts, Peru's total copper concentrate production is expected to reach a phased peak in 2026 and then gradually decline. While projects such as Tía María, Zafranal, Michiquillay, and Los Chancas represent potential future incremental supply, a project pipeline does not equate to actual supply release. New project commissioning first needs to offset the production pressure from declining grades at existing mines and the decline of aging mines before net incremental supply can emerge. Corporate capital expenditure arrangements are equally important. Copper prices, financing costs, project IRR, and parent company investment priorities will all influence whether a project moves into the actual development phase. Therefore, an improvement in policy direction does not equate to a rapid release of copper ore supply. Peru's future copper ore supply growth will still depend on the balance between new project implementation, existing mine expansions, and aging mine declines, with the overall trend more likely to feature gradual release rather than a concentrated short-term increase.

V. Conclusion

Judging from the government plans announced so far, the focus of the Fujimori administration's mining policy is not on raising mining taxes or promoting resource nationalism. Instead, it centers on project development efficiency, infrastructure construction, reinvestment incentives, illegal mining governance, and mining area revenue distribution. Compared with current policies, the change in the new government's plan lies not in altering Peru's mining development direction, but in strengthening execution tools. Peru does not lack copper resources and project pipeline; the key lies in whether projects can move from investment portfolios to construction and production more quickly. For the copper market, this round of political transition is more likely to first affect the risk premium and investment expectations for medium and long-term projects, rather than the actual supply of copper concentrates in 2026. Going forward, close attention still needs to be paid to the appointment of the mining minister, mining law revisions, implementation of the fast track mechanism, detailed implementation rules for Canon para el Pueblo, and the progress of approvals and construction for key projects such as Tía María, Zafranal, Michiquillay, La Granja, and Los Chancas. Overall, if relevant policies advance smoothly, development conditions for Peru's medium and long-term copper mine projects are expected to improve; however, before substantial breakthroughs are made in key constraints such as community issues, approvals, and infrastructure, Peru's copper ore supply will still be hard to increase significantly in the short term.

![Copper social inventory consolidated during the week, with total inventory lower YoY [SMM weekly data]](https://imgqn.smm.cn/usercenter/XBbTq20251217171709.jpg)

![Low Inventory Support Remains, Shanghai Spot Copper Premiums Consolidate and Pull Back [SMM Shanghai Spot Copper Weekly Review]](https://imgqn.smm.cn/usercenter/SiNDH20251217171711.jpg)