Copper Price Trend in H1 2026

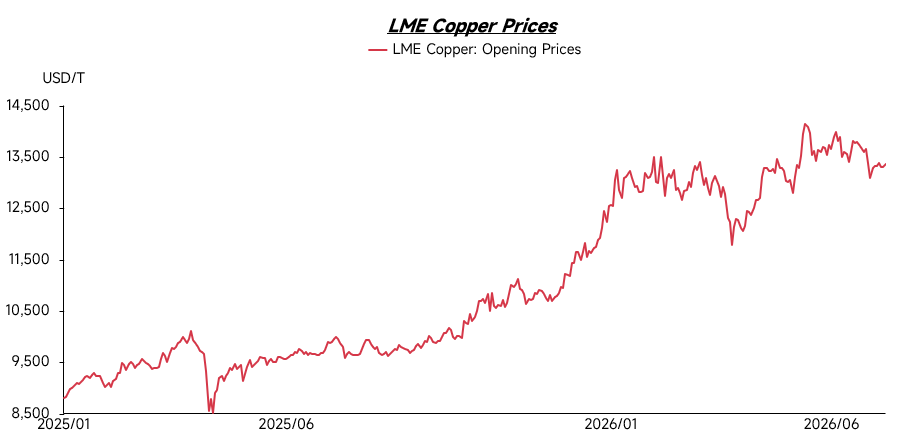

In the first quarter of 2026, copper prices generally remained at elevated levels, mainly fluctuating around $13,000/mt. It was not until the end of the first quarter that copper prices saw a brief correction. However, entering the second quarter, prices resumed their upward momentum and continued to set new historical highs. This was mainly supported by tight copper mine supply. Meanwhile, expectations of US tariff measures and the resulting global copper “siphon effect” further amplified market concerns over supply availability. At the same time, rapid growth in copper demand from emerging sectors such as new energy vehicles, renewable energy, power grid construction and data centres continued to strengthen medium- and long-term demand expectations. Against the backdrop of supply growth struggling to keep pace with demand expansion, copper prices remained strongly supported.

The tightening supply of copper also pushed companies to look beyond mine supply for supplementary sources, with the importance of copper scrap rising significantly. As copper prices continued to climb, copper scrap prices also moved higher. More importantly, the structural tightness in copper has begun to reshape the pricing logic of the copper scrap market, which had previously been driven more by downstream consumption and the spread between primary and secondary copper.

Supply Side

From the supply side, the overseas copper scrap market remains generally tight. Although high copper prices have to some extent stimulated recycling activity and selling interest from some suppliers, market inventories had already been continuously consumed from Q4 2025 to Q1 2026. As a result, overseas spot availability remains limited. According to feedback from some overseas scrap yards, delivery lead times after order placement have lengthened significantly, with some orders requiring three to four weeks before shipment can be arranged. This reflects that supply-side tightness has not yet been effectively eased.

At the same time, traditional copper scrap exporting regions such as Europe and the US are actively promoting the reshoring of manufacturing. Local demand for copper scrap processing and smelting has also increased, further weakening the supply elasticity of traditional export markets. Under the combined impact of declining exportable resources, stronger local consumption and intensified competition for high-quality materials, the tight supply pattern in the overseas copper scrap market is expected to persist.

Demand Side

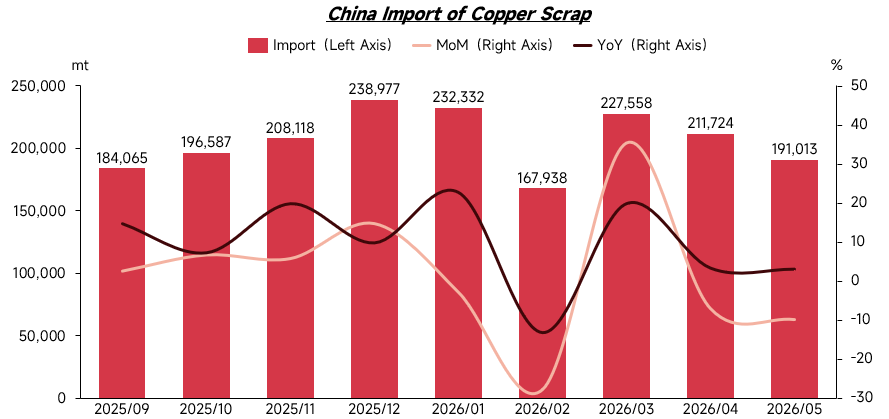

As the world’s largest consumer of copper scrap, China has long accounted for around one-third of global copper scrap trade. Since the beginning of 2026, affected by domestic policy and tax compliance requirements, the circulation and use of non-VAT-compliant copper scrap in the Chinese market have been restricted. This has encouraged domestic enterprises to further increase their demand for VAT-compliant imported copper scrap. In H1 2026, China’s copper scrap imports generally remained at high levels. Except for a temporary decline in February due to the Chinese New Year holiday and elevated copper prices, monthly imports in other months were higher than the same period in 2025, reflecting that China’s rigid demand for overseas copper scrap remains strong.

Outside of China market, the India, Southeast Asia and parts of Middle East are also increasing their capacity to absorb medium and low-grade copper scrap. Some low-grade materials enter these regions for dismantling, crushing, sorting or smelting before flowing into local consumption or regional markets. As a result, demand for overseas copper scrap is no longer determined solely by China’s imports. Instead, the market is gradually forming a multi-regional competition pattern involving China, India, Southeast Asia and local markets in traditional exporting regions.

Meanwhile, amid expectations of tighter copper supply in the future, competition for copper scrap is further intensifying globally. Smelters and related industry chain participants in various regions are actively expanding their access to copper scrap resources, while some countries have also started to strengthen the retention of domestic recycled metal resources. In addition, manufacturing reshoring in Europe and the US has supported the recovery of local copper scrap processing and smelting demand, weakening the outflow capacity of copper scrap from traditional export regions. Driven by China’s import demand, overseas local consumption demand and the trend of resource retention, global demand for copper scrap is generally on the rise.

Copper Scrap Prices

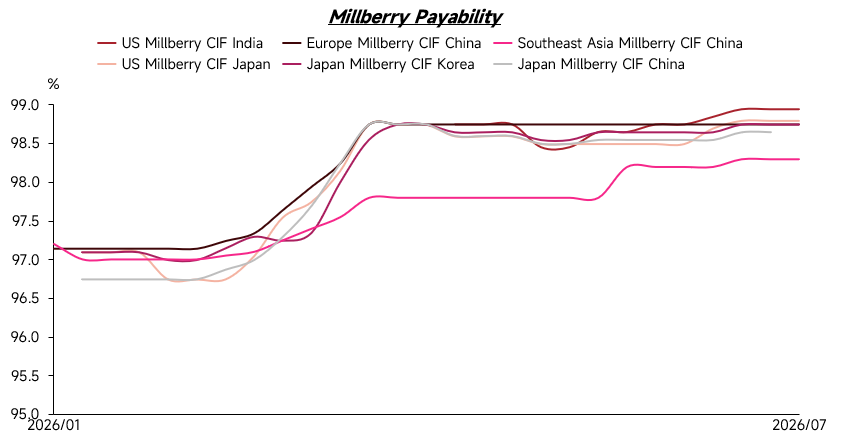

Against the backdrop of tight supply-demand conditions and stronger regional competition, overseas copper scrap payability has generally moved higher. Since the beginning of 2026, copper prices have remained at elevated levels, while millberry prices have also stayed relatively firm, with millberry payability mostly trading around 97.5%—98% of LME 3M. After copper prices saw a correction in March, copper scrap payability rose further, with millberry offers once moving up to 98.5%—99%. However, as copper prices ended their correction and returned to an upward trend in the second quarter, even breaking new historical highs, copper scrap payability did not fall significantly as it would have under the traditional pricing logic. Instead, it remained high. This change reflects that under tight raw material supply and rigid demand from buyers, overseas copper scrap payability remains resilient even when copper prices are high, leaving limited room for decline.

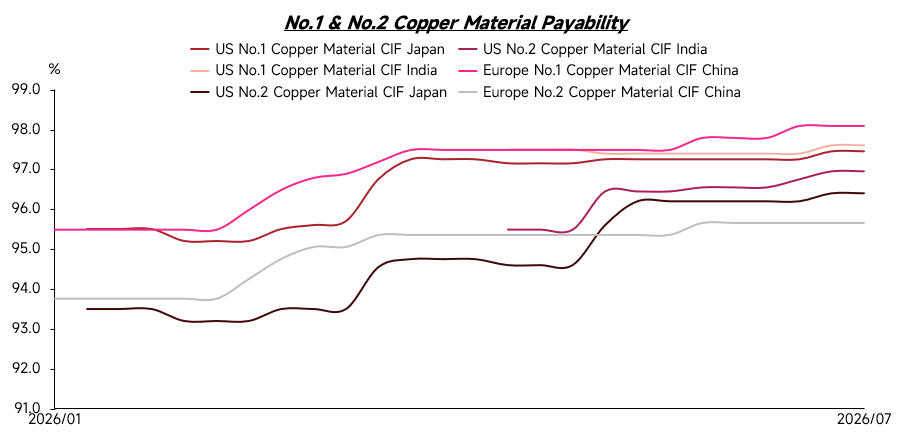

This trend can also be seen in No.1 copper scrap and No.2 copper scrap prices. Since the beginning of 2026, the payability of No.1 copper scrap has continued to rise, moving from around 95.5%—96% at the start of the year to the current range of 97%—98%. No.2 copper scrap prices have also increased significantly, while price differentiation has become more pronounced. Supported by persistently high precious metal prices, smelters have become more willing to accept higher prices for No.2 copper scrap with high gold and silver content. Some high-precious-metal-content materials can be quoted at 97.5%—98.5%, even exceeding the price of some No.1 copper scrap.

From the perspective of material structure, No.2 copper scrap with high gold and silver content is mainly sourced from the Americas. As a result, overall quotations for American No.2 copper scrap are significantly higher than those from other regions. In contrast, No.2 copper scrap from Japan, South Korea and Southeast Asia generally contains lower levels of gold and silver, so prices are relatively under pressure, with payability mostly concentrated around 95%—96%. This shows that the pricing logic of the copper scrap market has changed significantly. It no longer simply follows the traditional pattern of “rising copper prices leading to lower payability.” With tighter raw material supply, stronger resource competition and wider differences in material structure, copper scrap prices are now increasingly influenced by copper content, precious metal content, origin, smelting demand and purchasing power at the destination. Price differentiation is becoming more prominent.

Policy Side

Policy has always been an important variable affecting overseas copper scrap trade. In recent years, as expectations of tight copper supply and demand have continued to build, countries have placed increasing importance on copper scrap as a strategic secondary resource. Major economies have also strengthened regulation around scrap metal exports, imports and domestic recycling.

Taking the EU as an example, it is expected to formally implement new scrap metal export regulations from May 2027. At that time, copper scrap exports to non-OECD countries will need to meet two conditions: the destination country must be included on the EU’s approved list, and the destination processing facility must pass an independent third-party audit. The policy is intended to raise the threshold for scrap metal exports, restrict the outflow of insufficiently processed secondary metal resources and encourage more copper scrap resources to remain in Europe for local recycling and consumption. In the US, the copper industry has also pushed the proposal of including copper and recycled copper in the 45X tax credit to the legislative level in Congress. The aim is to enhance the competitiveness of domestic manufacturing and copper scrap processing through tax incentives, thereby further improving domestic resource retention.

In addition, as the world’s largest consumer of copper scrap, policy changes in China also have a significant impact on the global copper scrap trade landscape. The Chinese market is currently actively promoting the standardisation of the recycling industry. For a long time, some enterprises have faced difficulties in tax accounting and compliance when purchasing domestic copper scrap, as upstream recycling suppliers often lacked input invoices. In recent years, China has continued to promote the “reverse invoicing” mechanism, under which the buyer issues an invoice on behalf of a seller that does not have the ability to issue invoices, in order to improve the input invoice system. However, due to practical difficulties in implementation, some enterprises have further increased their purchases of VAT-compliant imported copper scrap to meet production and compliance requirements. This has also provided strong support for demand for overseas copper scrap.

In Southeast Asia, countries represented by Malaysia and Thailand have long served as transit and preliminary processing hubs for low-grade scrap metal materials. However, with rising environmental awareness and the need for industrial upgrading, these countries have tightened inspections and regulations on imports of low-end scrap materials, with some categories even facing stricter restrictions or bans. The purpose of these policies is to push domestic industries towards higher value-added activities while reducing environmental pollution and social issues caused by improper treatment of low-end scrap materials. As a result, more low-grade copper scrap may need to undergo more complete sorting, dismantling and pre-processing before export, or be redirected to new transit and processing regions. This will further increase the compliance and circulation costs of global copper scrap trade.

Overall, global copper scrap trade will no longer be determined simply by price. It will be increasingly affected by policy compliance, environmental requirements, resource retention and local processing capacity. For traders, the ability to provide stable supplies of high-quality, low-impurity copper scrap with complete compliance documents will become more competitive than simply offering lower prices.

Outlook for H2 2026

Looking ahead to H2 2026, exportable supply is unlikely to loosen significantly. After the continuous consumption of previous inventories, the release of new overseas scrap supply remains limited. Combined with stronger local copper scrap processing demand and resource retention intentions in traditional exporting regions such as Europe and the US, overseas exportable supply is unlikely to increase significantly. Mainstream categories such as millberry, No.1 copper scrap and No.2 copper scrap are expected to remain tight.

Second, multi-regional competition on the demand side will continue to support copper scrap prices. China’s import demand remains an important pillar of the overseas copper scrap market, while India, Southeast Asia, Japan, South Korea, Europe and the US are also increasing their absorption of copper scrap. Global demand for copper scrap is expected to show a pattern of multi-regional competition, and competition among regions for resources will support payability, making a sharp decline unlikely.

Against the backdrop of tight supply and stronger resource competition, overseas copper scrap payability is expected to remain high in H2 2026. Millberry and No.1 copper scrap payability will continue to have strong downside support, while No.2 copper scrap prices will remain clearly differentiated due to differences in gold and silver content, origin and smelting demand.

In addition, high copper prices will continue to raise trade risks. As copper prices stay elevated, the value of each cargo will also increase, pushing up traders’ capital occupation, exchange rate risks, logistics costs, warehousing costs, inspection costs and compliance costs. Therefore, even if rigid demand remains in the market, actual transactions may become more cautious. Buyers and sellers will pay greater attention to price locking, quality stability and delivery lead times.

Overall, the overseas copper scrap market in H2 2026 is expected to maintain the main trend of tight supply, high payability, price differentiation and rising trade costs.

![The SHFE/LME price ratio rises, premium offers continue to increase, while the market sees weak supply and demand, and actual trading is sluggish, [SMM Yangshan spot copper]](https://imgqn.smm.cn/usercenter/ULCXN20251217171714.jpeg)

![Impact of typhoon expectations persists, Shanghai spot copper premiums continue to rise [SMM Shanghai spot copper]](https://imgqn.smm.cn/usercenter/qcyEh20251217171709.jpg)

![Both inventory and copper prices declined, and suppliers held prices firm to sell [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/Fxolk20251217171712.jpg)