Full-Scale Review of the Copper Billet Industry in H1 2026

A. Policy Side: Stricter Reverse Invoicing Enforcement, Long-Term Constraints on Recycled Raw Material Circulation

In H1, fiscal and tax regulation became the core underlying constraint suppressing the copper billet industry. The reverse invoicing policy for recycled resources entered a phase of normalized high-pressure implementation. Individual small traders have an annual invoicing quota of RMB 5 million, leading to sharply narrowed circulation channels for domestically unticketed brass scrap. Grassroots recyclers’ willingness to sell remained low, and the supply of domestically produced compliant secondary brass remained persistently tight.

During the policy transition period, corporate compliance costs rose significantly. Small and medium-sized processing plants lacked stable channels for invoiced raw materials and were forced to voluntarily reduce output and conduct maintenance to mitigate risks. Leading large enterprises leveraged their international trade qualifications and steady import sources to buffer the raw material shortage, accelerating the concentration of industry capacity toward compliant large companies.

Policy No. 770 on secondary copper tax refunds continued to tighten, thoroughly squeezing gray circulation channels in the industry. The contradiction of raw materials being "available but without invoices, or invoiced but at high prices" persisted throughout the entire H1 period.

B. Raw Materials and Imports & Exports: Domestic Secondary Supply Contraction, Rising Import Secondary Brass Premiums

1. Domestic Raw Material Bottlenecks Intensified

The compliant circulation volume of domestically produced brass scrap dropped sharply YoY. The cost advantage of secondary brass over copper cathode weakened, and most brass billet plants were trapped in difficulties of raw material procurement and high deductible costs. Moreover, the quota ceiling for individual traders made it difficult for supply to return to prior-year levels. At the same time, speculation in the brass scrap market further pushed up prices, and copper-zinc separation operations raised overall raw material costs.

2. Imports Became the Main Supplement, but Costs Continued to Rise

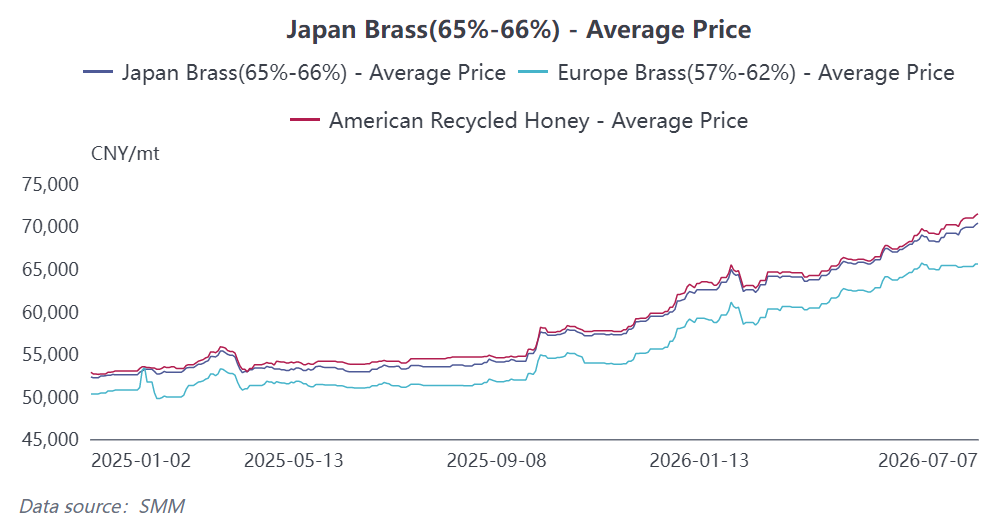

Chinese enterprises shifted to bulk purchases of invoiced imported secondary brass. H1 imports of secondary brass maintained YoY growth, but overseas copper scrap export policy disruptions and rising international copper prices pushed up procurement premiums. Available overseas brass scrap supply tightened, and the import purchase coefficient kept rising, further increasing raw material costs for brass billets.

From January to May, China's cumulative imports of brass billets were approximately 11,400 mt, down 1.23% YoY, while cumulative import value reached $105.7079 million, up 23.42% YoY, highlighting a clear pattern of lower volumes and higher prices. In terms of import sources, in May, South Korea held firm as the top source (about 40% share), Japan ranked second (about 16%), and early signs of regional diversification emerged.

(3) Costs and Prices: Copper prices swing wildly at highs, while industry processing fees continue to decline

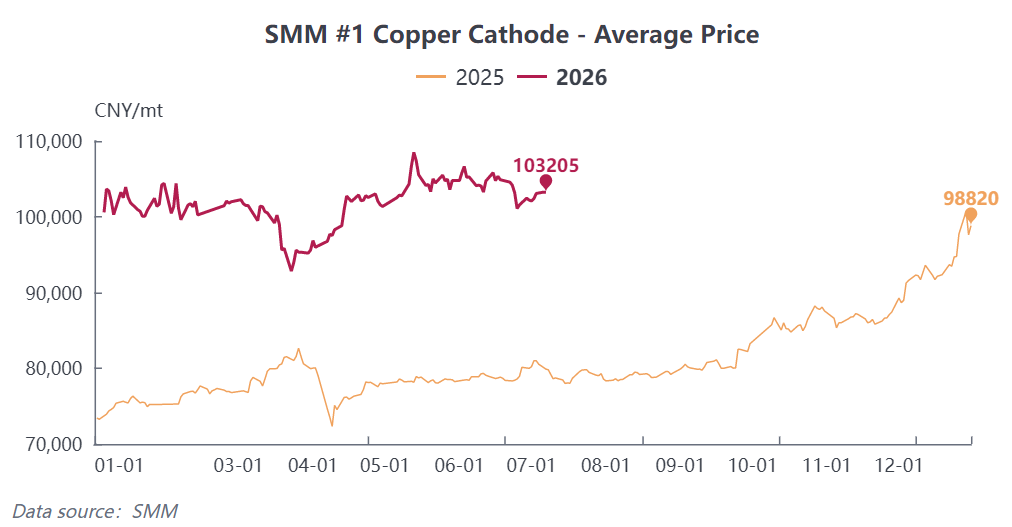

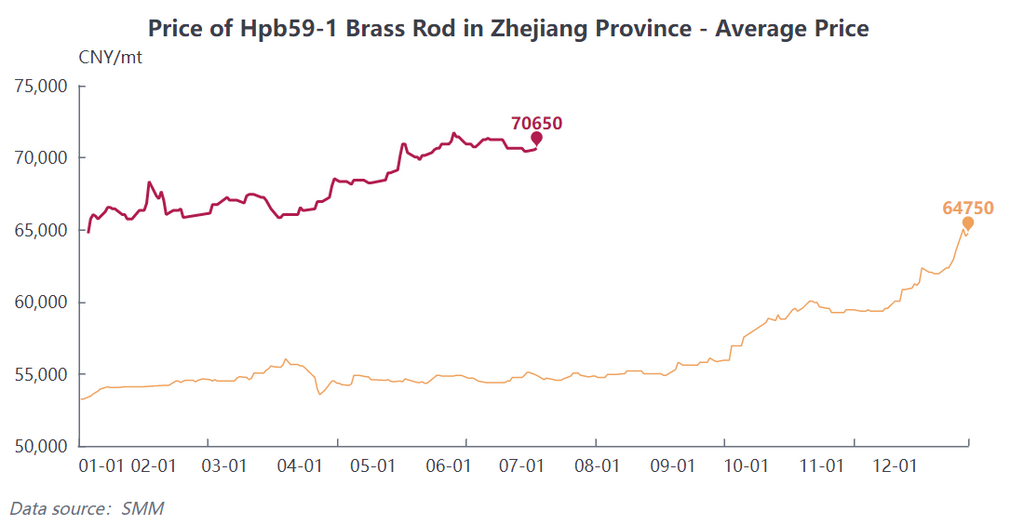

In H1 2026, copper cathode prices exhibited a "retreat after rapid rise and consolidate at highs" pattern, hitting the year's high in January and a phase low in March. In Q2, the price center stabilized above 100,000 yuan/mt. The full-year average price rose sharply YoY, directly boosting raw material costs for copper billet. As of end-June, the average spot price of Hpb59-1 brass billet in Zhejiang area briefly climbed to a historical high of 70,650 yuan/mt.

Price transmission faced significant obstacles: traditional brass downstream demand was weak, end-users had strong bargaining power, raw material price increases could not be smoothly passed downstream, and the industry exhibited a typical "price up, volume weak" pattern under pressure. From April to May, the industry's overall profit pressure climbed to the worst level in nearly two to three years.

New energy and AI-related high-precision copper billets, due to technical barriers and stable rigid demand, showed stronger processing fee resilience, becoming the only sub-category with relatively stable profits in H1. Coupled with rising logistics, tax, and capital occupation costs, most small and medium-sized brass billet enterprises remained in a state of marginal profits or even losses for a long time.

(4) Supply and Demand: Demand severely polarized, operating rates persistently low

1. Supply side: operating rates weakened month by month, with significant divergence among enterprises

In H1, the comprehensive operating rate of copper billet production drifted lower overall, declining from 50.86% in January to 46.09% in June, falling both YoY and MoM. The capacity stratification gap continued to widen: large enterprises had stable raw material channels, with an operating rate of 52.6% in June; medium-sized enterprises were squeezed by both raw material and order pressures, operating at only 38.76%; small processing plants faced raw material shortages and lack of orders, with operating rates falling to 23.44%, intensifying industry polarization.

Raw material constraints were the core supply-side suppressing factor, and coupled with losses forcing enterprises to control production, the industry's overall capacity utilization rate remained in a historically low range in H1.

2. Demand side: traditional sectors weakened deeply, while emerging sectors strengthened independently

Traditional brass demand (air conditioning, plumbing, valves, general hardware) remained persistently weak in H1. The property market remained sluggish in the late cycle, coupled with an early off-season for home appliances; downstream purchases were made as needed, with no concentrated restocking activity. Meanwhile, the penetration rate of stainless steel substitution for air conditioning parts continued to rise, steadily diverting rigid demand for brass, causing brass billet orders to shrink month by month.

Structural demand support was concentrated in the copper billet segment: NEV three electric systems (power battery, drive motor and electronic control system), large power charging piles, energy storage PCS, AI server GPU cooling, and precision optical module pins continued to release stable rigid demand. High-purity oxygen-free copper billet orders were full, offsetting the overall decline in industry demand. However, copper billet capacity accounted for a limited share, making it difficult to boost the brass segment's recovery.

II. 2026 H2 Copper Billet Industry Outlook

In Q3, the industry will be under pressure and hit bottom. The traditional off-season, combined with high temperatures suppressing end-user procurement, and stainless steel substitution continuing to erode brass demand, SMM expects the comprehensive copper billet operating rate to fall further to 43.65% in July, with industry operation hitting the year's low point. On the policy front, reverse invoicing regulation is unlikely to ease, the compliant supply ceiling for domestic secondary brass is constrained, and overseas copper scrap export controls continue to tighten. The high premium pattern for imported secondary brass will persist, with raw material bottlenecks running through the off-season.

Brass billet is dragged down by the off-season, substitution, and low processing fees, with profits remaining under pressure in Q3; only the continued production ramp-up of NEV and AI computing infrastructure brings rigid demand orders for copper billet, providing the sole demand support. Q4 business conditions are expected to recover QoQ. Home appliance and plumbing sectors will enter their traditional stockpiling peak season, and brass billet orders are expected to rebound QoQ. Coupled with the year-end push for annual targets in PV, energy storage, and new energy vehicles, copper billet demand will strengthen further, lifting the industry’s operating rate and transactions in tandem. However, copper cathode prices are highly likely to continue to consolidate at highs, keeping raw material costs elevated. Cost pressure will persist throughout the year for processing enterprises.

In the medium to long term, the demand center for traditional brass has been declining year by year, while AI computing power, new energy, and energy storage have become the core growth poles for the copper billet industry. Lower-tier and outdated capacity continues to exit the market. Top-tier players are simultaneously deploying high-end copper billet capacity. The three barriers of raw materials, orders, and compliance are steadily widening the gap among enterprises. The industry’s transformation toward scale, compliance, and high-end production is an irreversible trend.

In H1 2026, the core challenge for the copper billet industry was a supply shortage caused by tighter recycled raw material policies, weakening traditional end-use demand, and high copper prices squeezing processing profits. The industry relied on structural support from copper billet used in new energy and AI applications, and overall remained weak. In H2, the market is expected to show a low-then-high pattern: Q3 will see a confluence of three headwinds—the off-season, raw material issues, and substitution—keeping operating rates and profits under continuous pressure; in Q4, the traditional end-use peak season combined with continued volume growth in emerging sectors will drive a QoQ recovery in business conditions. In the medium to long term, the reverse-charging invoice policy will reshape the secondary copper circulation system, accelerating industry consolidation, and high-precision copper billet for new energy and AI computing power will become the core growth driver for the copper billet industry in the future.

![The SHFE/LME price ratio rises, premium offers continue to increase, while the market sees weak supply and demand, and actual trading is sluggish, [SMM Yangshan spot copper]](https://imgqn.smm.cn/usercenter/ULCXN20251217171714.jpeg)

![Impact of typhoon expectations persists, Shanghai spot copper premiums continue to rise [SMM Shanghai spot copper]](https://imgqn.smm.cn/usercenter/qcyEh20251217171709.jpg)

![Both inventory and copper prices declined, and suppliers held prices firm to sell [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/Fxolk20251217171712.jpg)