In H1 2026, the copper rod industry experienced significant divergence amid high copper price fluctuations and limited secondary supply: periodic corrections in copper prices drove a notable YoY rise in copper cathode rod operating rates, while secondary copper output remained constrained by compliance policies, pushing industry operating rates and processing fees into a high-then-low trend. Downstream wire & cable and enamelled wire operating rates were mixed, reflecting differing demand across subsectors. Meanwhile, overseas power infrastructure and the energy transition generated substantial rigid procurement demand, and China’s copper wire rod exports surged, nearly doubling. Looking to H2, high copper prices and overcapacity are expected to persist, widening the gap between copper cathode rod and secondary copper rod.

(I) Copper Price Fluctuations and Secondary Supply Shortage Lead to Significant YoY Increase in Copper Cathode Rod Operating Rate in March

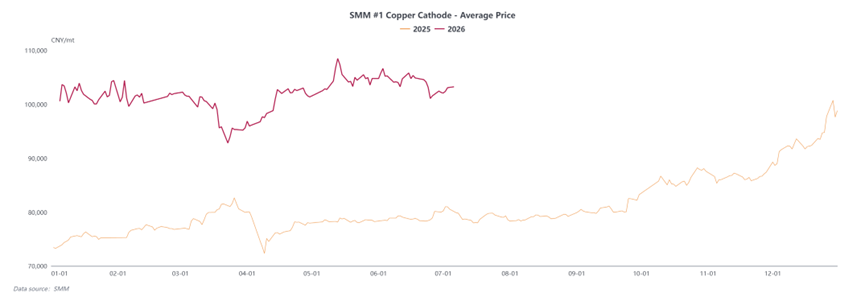

From the H1 copper cathode price trend, it is clear that the full-year average copper price in 2026 was significantly higher than that in the same period of 2025. Since last year, copper prices have generally drifted higher, and downstream wire and cable enterprises have gradually adapted to high raw material costs, with price acceptance continually increasing. In March this year, copper prices underwent a notable correction. Combined with the prolonged low operating rate of secondary copper rod, market demand was concentrated on copper cathode rod, leading to a concentrated release of purchasing demand that was previously suppressed by high prices. By contrast, in the same period of 2025, copper prices were in a continuous upward channel, and downstream stockpiling willingness was weak. These factors collectively drove the copper cathode rod operating rate in March up by 5.41 percentage points YoY.

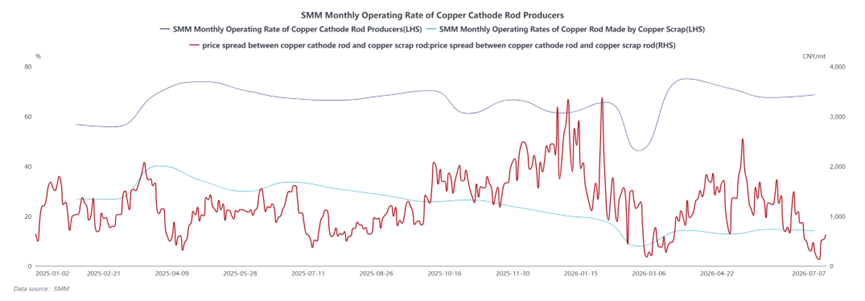

(II) Compliance constraints suppress secondary copper output, and copper cathode rod operating rate and processing fees rise then fall.

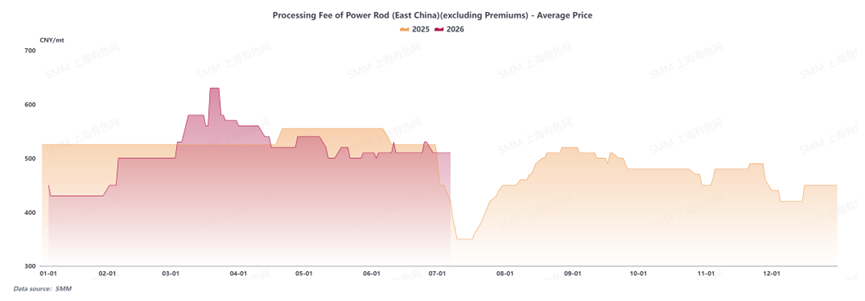

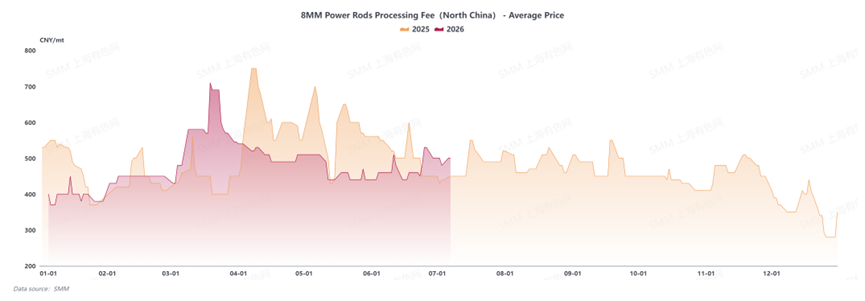

Compliance policies for the secondary copper industry continued to be implemented, restricting the circulation of tax-included copper scrap supplies. The price difference between copper cathode and copper scrap swung wildly, and the cost advantages of secondary copper rod disappeared intermittently. Secondary copper capacity could not be fully released; only top-tier compliant enterprises maintained stable production, and operating rates remained low for an extended period. Demand shifted towards copper cathode rod, driving copper rod enterprises’ operating rates to show a high-then-low pattern. From January to March, concentrated downstream stocking by cable and wire companies and the two major power grids kept operating rates above 75%, pushing copper rod processing fees higher YoY. From April to June, copper prices surged again, curbing downstream stocking interest. Copper rod processing fees gradually pulled back from high levels, and the industry average operating rate retreated to the 60%-65% range. Many small and medium-sized processing plants faced insufficient orders and experienced periodic production cuts.

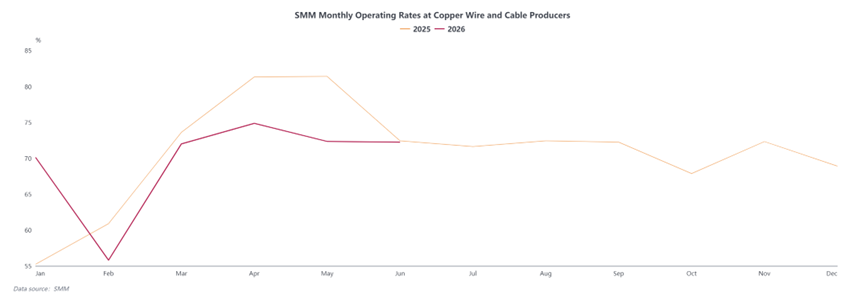

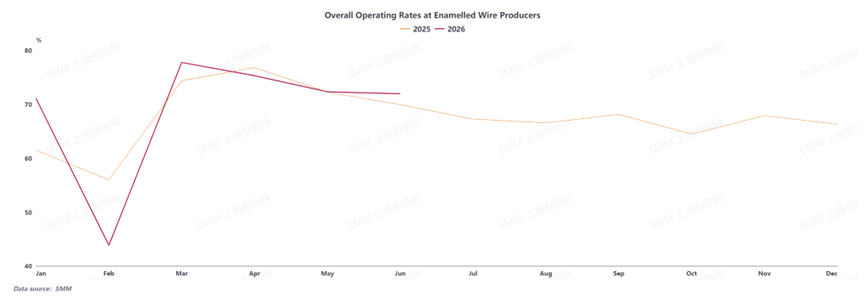

(III) Copper Wire and Cable and Enamelled Wire Exhibit Phase-Based Operating Trends, With Clear Divergence in Downstream Demand

In H1 2026, both the copper wire and cable and enamelled wire industries experienced an operating pattern of rapid post-Chinese New Year recovery, peaking in the high season, and then pulling back month by month. The monthly operating rate of copper wire and cable recovered from the weekly low during the Chinese New Year to a peak in April, then consolidated and stabilized in May and June, with investment at the start of the power grid’s 15th Five-Year Plan and exports providing core support, while orders from the construction and real estate sectors continued to be a drag. The monthly operating rate of enamelled wire hit its seasonal bottom after the Chinese New Year and surged to the annual high in March, but as home appliance demand weakened more than expected in Q2, the Q2 operating rate declined month by month, with the new energy, industrial motor, and export sectors acting as a floor. Both industries faced the challenges of high copper prices suppressing downstream purchase willingness and pulse-style demand releases causing frequent fluctuations in production schedule pace.

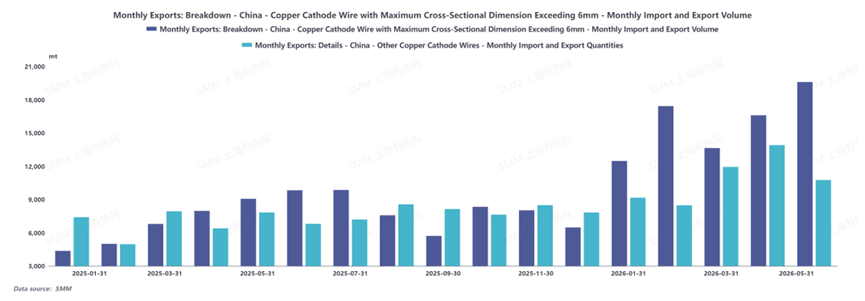

(4) Multiple Positive Factors Resonate, H1 2026 Copper Wire Rod Exports Experience Explosive Growth

In H1 2026, China’s copper wire rod exports continued their strong growth momentum, emerging as the most outstanding segment in the copper processing industry. In terms of export pace, the first half was characterized by a pattern of “month-on-month climb followed by stabilization at highs.” In Q1, despite the impact of the Chinese New Year holiday, exports maintained consecutive MoM growth. In Q2, driven by the concentrated release of backlog orders and sustained robust overseas demand, monthly exports continued to rise and stayed high. From January to May, China’s cumulative copper wire rod exports reached 134,000 mt, surging 97.93% YoY. Export markets were highly concentrated in Southeast Asia, the Middle East, and South Asia. Countries such as Thailand, Malaysia, Vietnam, and Saudi Arabia, with their power infrastructure upgrades, new energy project construction, and manufacturing relocation, generated rigid import demand for copper wire rod. In terms of trade structure, processing trade with imported materials was the mainstream export model, accounting for over 50%, supplemented by processing trade with supplied materials. Following adjustments to export tax rebate policies, China’s export enterprises have fully shifted to processing trade channels, with related business operating models reaching maturity.

(V) High Copper Prices Alongside Overcapacity, with the Landscape of Copper Cathode Rod and Secondary Copper Rod Continuing to Diverge

Looking ahead to H2 2026, the copper rod industry is expected to remain in a complex landscape of sustained high copper prices, deepening overcapacity, and continued strong export performance, with the divergence between copper cathode rod and secondary copper rod widening further. Copper cathode rod enterprises are under the dual pressures of elevated raw material costs and insufficient new orders. Prior backlog orders are gradually being delivered and fulfilled, and combined with overseas markets entering a seasonal off-season for consumption, the industry’s operating rate is likely to pull back MoM. However, the core contradiction of overcapacity persists, and overall copper rod processing fees will continue to be in the doldrums.The operating rate on the secondary copper rod side is unlikely to see a sustained uptrend, as the narrowing price difference between copper cathode rod and secondary copper rod has largely eliminated its substitution advantage, with market share continuing to concentrate toward copper cathode rod. Demand continues to shift to copper cathode rod. On the demand side, power grid, new energy, and computing power cables provide stable rigid demand, while demand from real estate and home appliances is weak, limiting overall incremental growth. On the export front, Chinese enterprises continue to develop markets in Southeast Asia and the Middle East, but overseas local capacity expansion and a high base will weigh on subsequent growth rates. Overall, the industry faces multiple contradictions, and the copper cathode rod segment must still rely on expanding both domestic and external demand channels.

![Both inventory and copper prices declined, and suppliers held prices firm to sell [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/Fxolk20251217171712.jpg)

![End-use demand shows no improvement yet, tight supply and holding prices firm push up spot copper discounts in North China [SMM North China Copper Spot]](https://imgqn.smm.cn/usercenter/tXxfd20251217171713.jpg)