Noticias de SMM del 7 de julio:

I. Revisión del mercado de China en el primer semestre

Importaciones: crecimiento de recuperación, con África impulsando el incremento

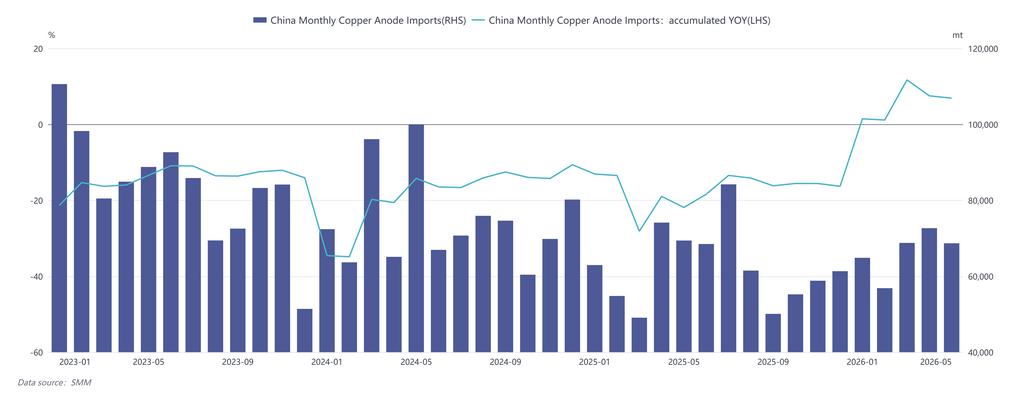

Las importaciones de ánodos de cobre de China totalizaron 331.900 t en enero-mayo de 2026, un aumento interanual del 6,92%, revirtiendo la tendencia débil de una caída interanual del 15,88% en todo el año 2025. En términos mensuales, las importaciones siguieron una tendencia de "bajo-alto-luego retroceso". La estructura de las fuentes de importación experimentó cambios significativos. Zambia siguió siendo la principal fuente, pero su participación se redujo gradualmente del 53% a principios del año a alrededor del 40% en mayo. La República Democrática del Congo (RDC) se convirtió en la mayor fuente de incremento, con su participación en las exportaciones a China aumentando rápidamente de menos del 10% en enero al 22,60% en mayo, respaldada por la continua puesta en marcha del proyecto de fundición de cobre Kamoa (con una capacidad anual de blister de 500.000 t), y su crecimiento interanual llegó a superar el 250%. En contraste, el material chileno siguió reduciéndose debido a las persistentes inversiones de precios de importación, y su participación cayó al 4,48% en mayo.

Oferta y demanda internas: rápida reversión de la relajación al endurecimiento

La evolución del patrón de oferta y demanda interno en el primer semestre puede dividirse en dos fases:

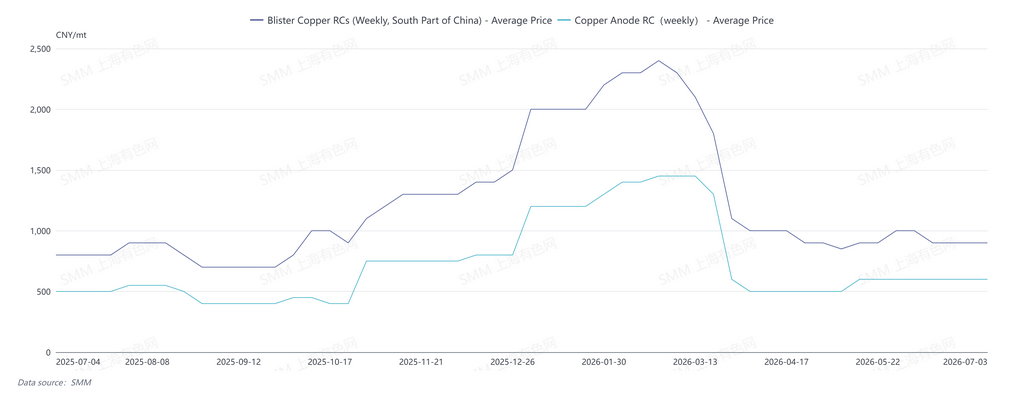

Fase de relajación en el T1: La oferta de blister de cobre y placas anódicas derivados de chatarra se mantuvo amplia, prolongando el estado de abundancia de finales de 2025. Las fundiciones mantuvieron altos inventarios de material frío, y los cargos de refinación (RC) spot de blister de cobre en el sur de China operaron en niveles altos de 1.800-2.000 yuan/t. Bajo el patrón holgado, la dependencia del mercado de ánodos de cobre importados disminuyó temporalmente.

Un punto de inflexión surgió a mediados o finales de marzo: cuando los precios del cobre cayeron por debajo de los 100.000 yuan/t, la diferencia de precios entre el metal primario y la chatarra se redujo rápidamente. Al mismo tiempo, las políticas industriales se endurecieron intensamente—inspecciones de cumplimiento más estrictas para el cobre secundario y la reducción del apoyo financiero presionaron a los productores de ánodos de cobre derivados de chatarra con altos costos de materia prima, erosionando rápidamente su disposición a producir y provocando que la oferta del mercado comenzara a contraerse.

Fase de endurecimiento en el T2: El desequilibrio entre oferta y demanda estalló intensamente en el segundo trimestre. La tasa operativa general de las empresas de ánodos de cobre de SMM cayó del 50,42% en marzo al 45,95% en junio, y el segmento derivado de chatarra disminuyó del 40,58% al 36,00%. Mientras tanto, el T2 coincidió con un mantenimiento concentrado de las fundiciones nacionales, lo que a su vez incrementó sus necesidades de compra externa de material frío. La contracción de la oferta y el impulso de la demanda se movieron en direcciones opuestas en la misma ventana, ampliando fuertemente la brecha entre oferta y demanda. El promedio mensual de los RC spot de blister de cobre en el sur de China se desplomó a 950 yuan/t en abril, una caída intermensual de 850 yuan/t, y disminuyó aún más a 900 yuan/t en mayo.

II. Análisis de los impulsores clave detrás de los cambios en la oferta y la demanda

(1) El endurecimiento de las políticas sobre el cobre secundario es la variable principal de la contracción de la oferta

El motor principal de la reversión del patrón de oferta y demanda en el primer semestre provino de los choques de políticas sobre la industria del cobre secundario. Las actividades de compra de las empresas de fundición secundaria se vieron obstaculizadas, acompañadas de una reducción simultánea de las políticas financieras de apoyo. Los mercados de materias primas con impuestos incluidos y sin impuestos incluidos se polarizaron notablemente, lo que se convirtió en la razón principal para que las empresas redujeran o detuvieran la producción.

(2) La reducción de la diferencia de precios entre el metal primario y la chatarra amplificó los desequilibrios de la oferta

A medida que los precios del cobre carecían de impulso alcista, la diferencia de precios entre el metal primario y la chatarra se redujo rápidamente. Los proveedores de chatarra de cobre retuvieron las ventas, dificultando el apoyo a una gran afluencia de cobre secundario al segmento de fundición, acelerando la reversión del patrón de oferta y demanda.

(3) Los cargos de tratamiento (TC) extremadamente bajos aumentaron la dependencia del material frío desde el lado de los costos

Los TC de concentrados de cobre continuaron deteriorándose en 2026. En este contexto, las fundiciones ajustaron proactivamente su mezcla de materias primas, aumentando la proporción de uso de materiales fríos como la chatarra de cobre y los ánodos de cobre. Esta lógica de sustitución proporcionó un soporte base rígido y en continua expansión para la demanda de ánodos de cobre.

III. Perspectivas para el segundo semestre

Se espera que las importaciones del segundo semestre enfrenten presión: el mantenimiento programado de la capacidad de fundición de crudo de Zambia se extenderá hasta el T3, mientras que el aumento de la demanda de países como India intensifica la competencia por el suministro de ánodos de cobre.

Oferta de China: Las variables centrales del lado de la oferta interna siguen siendo la dirección de las políticas sobre el cobre secundario y la diferencia de precios entre el metal primario y la chatarra. La escasez estructural de chatarra de cobre con impuestos incluidos es difícil de mejorar antes de una relajación sustancial de las políticas, lo que mantiene limitada la elasticidad de la oferta de ánodos de cobre derivados de chatarra; bajo esta condición, los RC también enfrentan dificultades para repuntar significativamente. Si en el segundo semestre surge una relajación marginal de las políticas, se espera que la oferta del segmento derivado de chatarra se recupere; de lo contrario, persistirá el patrón de oferta ajustada.

Demanda de China: El lado de la demanda sigue respaldado: los bajos niveles de TC siguen impulsando la demanda de sustitución por materiales fríos; la tendencia a medio y largo plazo de expansión de la capacidad de cobre refinado se mantiene sin cambios, y el déficit de materias primas persiste.

IV. Resumen

En el primer semestre de 2026, la lógica operativa central del mercado de ánodos de cobre de China puede resumirse de la siguiente manera: los inicios de proyectos en el extranjero impulsaron una recuperación de las importaciones, pero el endurecimiento de las políticas nacionales sobre el cobre secundario desplazó rápidamente el patrón de oferta y demanda de un superávit en el T1 al endurecimiento en el T2. En el segundo semestre, salvo estímulos políticos, la elasticidad de la oferta interna sigue siendo limitada, mientras que la demanda de sustitución de las fundiciones por materiales fríos se mantiene fuerte, manteniendo el mercado general en un equilibrio ajustado.

A largo plazo, persiste la contradicción estructural de que el crecimiento de la capacidad de cobre refinado supera persistentemente al crecimiento de la capacidad de fundición de crudo, y la posición de mercado del ánodo de cobre como materia prima suplementaria clave seguirá fortaleciéndose. La creciente participación del ánodo de cobre derivado de chatarra, la diversificación de las fuentes de importación y la evolución del sistema de suministro caracterizado por "complementar los minerales con chatarra" y "complementar las fuentes externas con fuentes internas" representan las direcciones centrales del desarrollo del mercado de ánodos de cobre.

![Las transacciones de fin de mes fueron tranquilas, las primas del cobre al contado en Shanghái cayeron bajo presión [SMM cobre al contado en Shanghái]](https://imgqn.smm.cn/usercenter/OsOmo20251217171709.jpg)

![La relación de precios SHFE/LME se debilita, la estructura de backwardation se amplía, la prima spot retrocede ligeramente [Cobre spot de Yangshan, SMM]](https://imgqn.smm.cn/usercenter/NUcrH20251217171713.jpeg)

![Débil impulso en la recuperación de la demanda aguas abajo, las primas del norte de China se recuperan ligeramente [SMM Cobre Spot del Norte de China]](https://imgqn.smm.cn/usercenter/HeIuV20251217171708.jpg)