SMM, July 7:

I. H1 Market Review

Imports: Recovery growth, Africa becomes the main incremental source

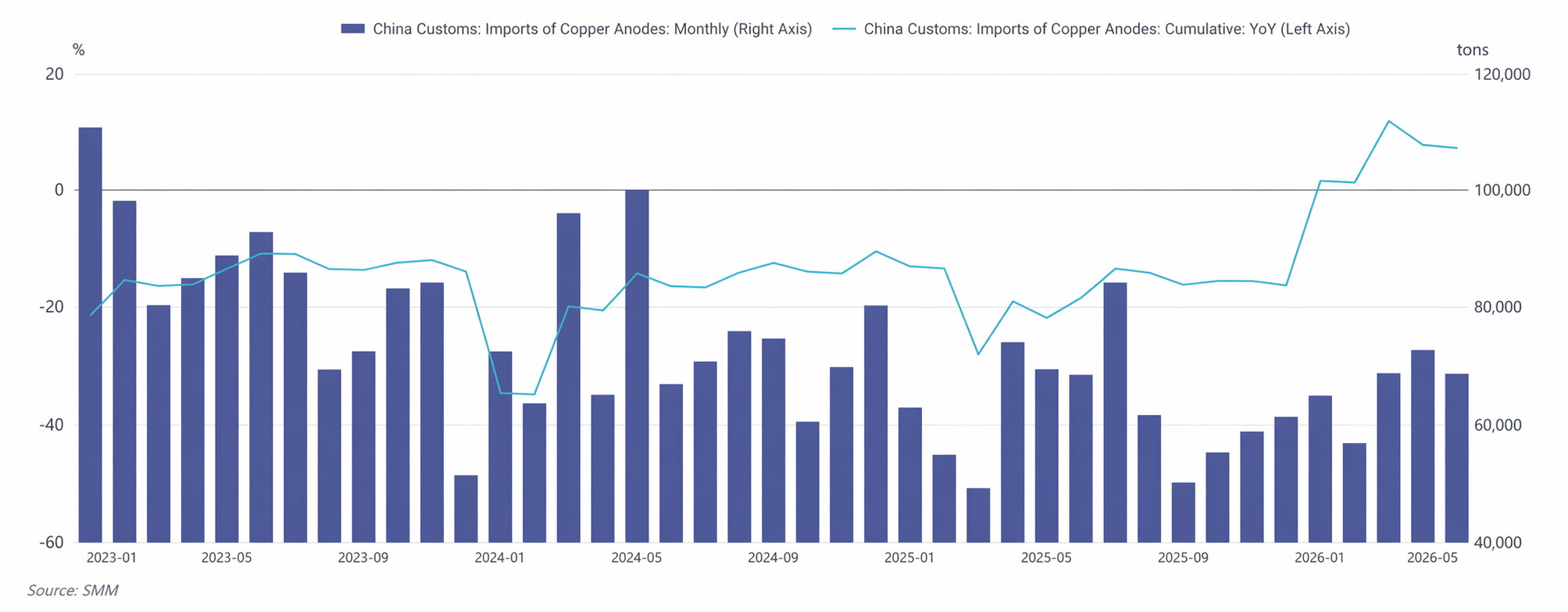

From January to May 2026, China’s cumulative copper anode imports reached 331,900 mt, up 6.92% YoY , reversing the sluggish trend of a 15.88% YoY decline for the full year of 2025. On a monthly basis, imports showed a "low, then high, then pullback" trajectory. The import source structure underwent significant changes. While Zambia remained the top source, its share gradually pulled back from 53% at the beginning of the year to around 40% by May. The DRC emerged as the largest source of incremental volume. Supported by the continued ramp-up of the Kamoa copper smelting project (smelting capacity of 500,000 mt/year) after commissioning, its share of exports to China climbed rapidly from less than 10% in January to 22.60% in May, with YoY growth exceeding 250% at one point. In contrast, Chilean cargoes continued to shrink due to an unfavorable SHFE/LME price ratio, with its share falling to 4.48% by May.

Domestic Supply and Demand: Rapid Reversal from Easing to Tightening

The evolution of China's domestic supply-demand pattern in H1 can be divided into two phases:

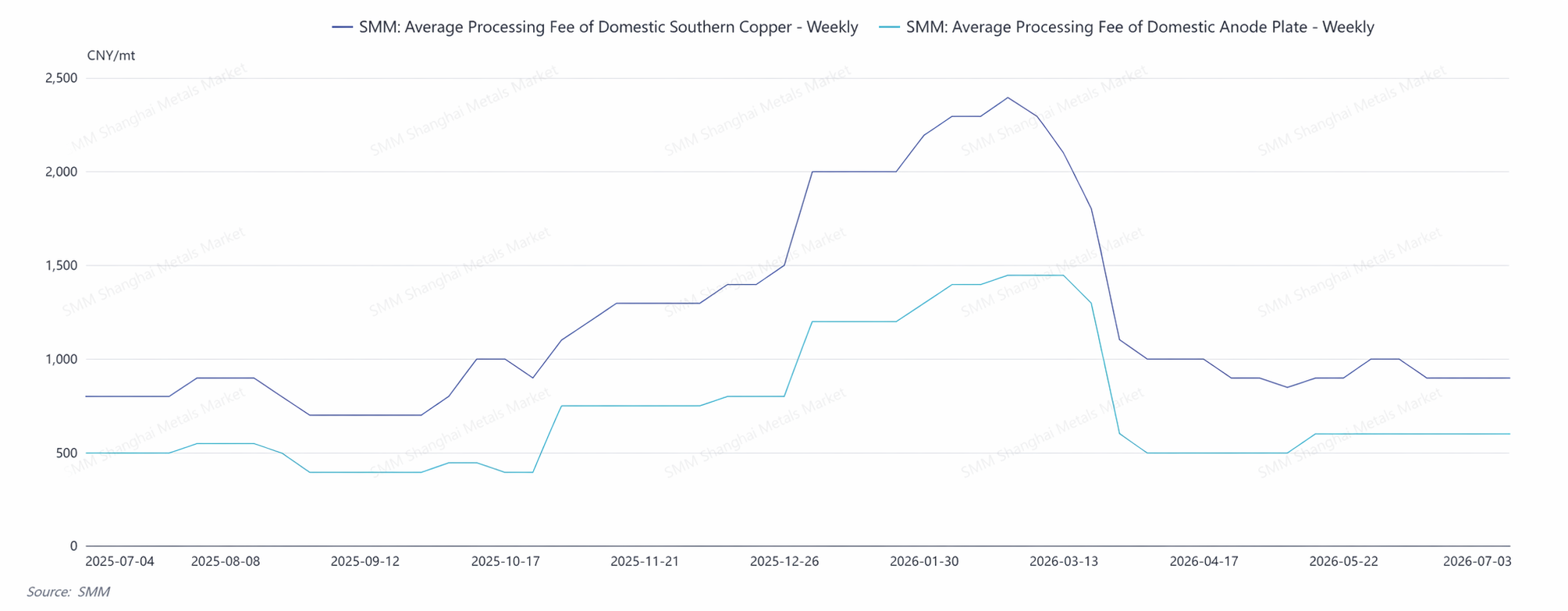

Easing Phase in Q1: Supply of scrap-derived blister copper and copper anode remained abundant, continuing the state from the end of 2025. Smelters held high inventories of blister copper and copper anode. Blister copper RCs in south China operated at high levels of 1,800-2,000 yuan/mt. Under this loose pattern, the market's reliance on imported copper anode declined temporarily.

Inflection Point Out in Mid-to-Late March: As copper prices fell below the 100,000 yuan/mt mark, the price difference between copper cathode and copper scrap narrowed rapidly. Meanwhile, industry policies tightened intensively—stricter compliance reviews for copper scrap and reductions in financial support—causing scrap-derived copper anode producers to face the squeeze of high raw material costs. Their production enthusiasm fell rapidly, and market supply began to contract.

Tightening Phase in Q2: The supply-demand imbalance erupted intensely in Q2. The overall operating rate of SMM-covered copper anode enterprises fell from 50.42% in March to 45.95% in June, with the scrap-derived segment declining from 40.58% to 36.00%. Meanwhile, Q2 coincided with the concentrated maintenance season for domestic smelters. Smelters under maintenance saw their demand for externally purchased blister copper and copper anode increase instead. Supply contraction and demand surges moved in opposite directions within the same window, drastically widening the supply-demand gap. In April, the average monthly blister copper RCs in south China plummeted to 950 yuan/mt, down 850 yuan/mt MoM, and fell further to 900 yuan/mt in May.

II. Analysis of Core Reasons for Supply-Demand Changes

(I) Tighter Policies for Copper Scrap Were the Primary Variable Behind the Supply Contraction

The core driver behind the reversal of the supply-demand pattern in H1 was the policy shock in the copper scrap industry. Obstructions in the purchasing processes of secondary smelting enterprises, accompanied by a simultaneous cut in supporting financial assistance, led to a clear polarization between the markets for tax-included and tax-excluded raw materials. This became the primary reason forcing enterprises to cut or halt production.

2. Narrowing copper cathode-scrap price difference amplifies supply contradictions

As copper prices lacked upward momentum, the price difference between copper cathode and copper scrap narrowed rapidly. Copper scrap suppliers held back from selling, and this also failed to support a large inflow of copper scrap into the smelting segment, accelerating the reversal of the supply-demand pattern.

3. Extremely low TC drives up dependence on blister copper and copper anode from the cost side

Copper concentrate TC continued to deteriorate in 2026. Against this backdrop, smelters proactively adjusted their raw material mix, increasing the use of copper scrap, copper anode, and other blister copper and copper anode. This substitution logic provided rigid and steadily expanding floor support for copper anode demand.

III. H2 Outlook

H2 imports face pressure: concentrated maintenance of Zambia’s smelting capacity will last into Q3, while growing demand from countries and regions such as India intensifies competition for copper anode supply.

China supply: The core variable on China’s supply side remains the direction of recycled copper policy and changes in the cathode-scrap price difference. The structural shortage of tax-included copper scrap is hard to improve before a substantial policy easing, and the supply elasticity of scrap-derived copper anode will remain constrained; under this premise, RC will also struggle to rebound markedly. If policy sees marginal loosening in H2, supply from scrap-derived production could recover; otherwise, the tight pattern will persist.

China demand: The demand side retains support: persistently low TC continues to push up substitution demand for blister copper and copper anode; the medium and long-term trend of refining capacity expansion remains intact, and the raw material gap persists.

IV. Summary

In H1 2026, the core operating logic of the Chinese copper anode market can be summarized as: overseas project commissioning drove import recovery and growth, but the tightening of China’s recycled copper policy rapidly reversed the supply-demand pattern from a loose Q1 to a tight Q2. In H2, in the absence of favorable policies, China’s supply elasticity will be limited, while smelters’ substitution demand for blister copper and copper anode remains strong; the market overall will maintain a “tight balance” pattern.

In the medium and long term, the structural contradiction of refining capacity growth consistently outpacing smelting capacity growth persists, and copper anode’s market position as a critical supplementary raw material will continue to strengthen. The rising share of scrap-derived copper anode, diversification of import sources, and the evolution of a supply system that “supplements ore with scrap and supplements external supply with domestic supply” represent the core direction of the copper anode market’s evolution.