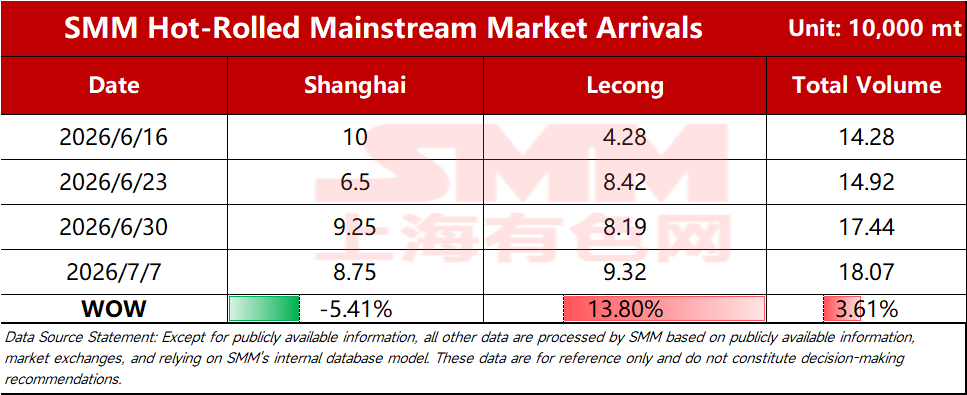

SMM Steel, July 7 – According to SMM statistics, this week’s estimated total shipments of resources to the mainstream markets were 180,700 mt, up 3.61% WoW. By market:

Table 1: Comparison of Arrivals in Mainstream Markets

Source: SMM Steel

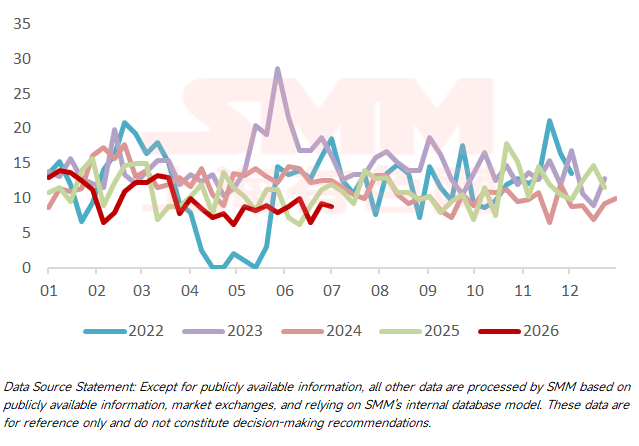

Shanghai Market: Hot-rolled coil shipments into the Shanghai market moved sideways WoW. Specifically, the decline mainly came from mainstream South China resources, while shipments from other steel mills saw relatively small changes. Looking ahead, against the backdrop of the off-season, market transactions were average, and steel mill shipments remained stable. Short-term arrivals in the Shanghai market are expected to fluctuate at low levels.

Chart-1: Arrivals in the Shanghai Market

Source: SMM Steel

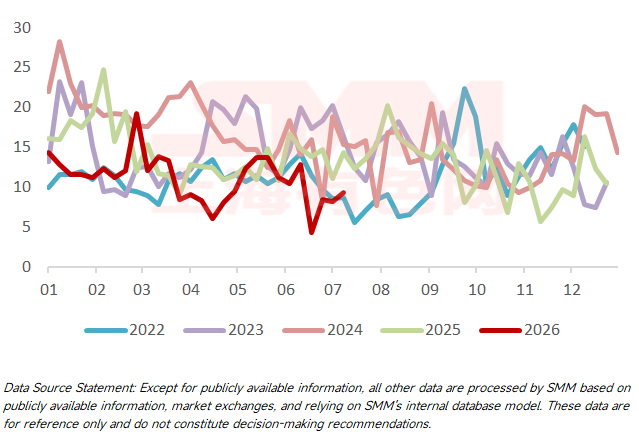

Lecong Market: Shipments to the Lecong destination increased this week. Specifically, resources from North China remained stable, while the two major mainstream sources showed mixed increases and decreases, though overall volumes remained at a relatively low level. Looking ahead, short-term southbound resources will remain relatively small. For mainstream sources, one steel mill has resumed production and near-term export orders are few, but recent typhoons in South and East China may affect the arrival of some resources, making it difficult for arrivals to increase significantly in the near term.

Chart-2: Arrivals in the Lecong Market

Source: SMM Steel

SMM releases mainstream market hot-rolled shipment data by destination every Tuesday. To subscribe or follow more data, please scan the QR code below.

![[SMM Steel] 7.7 SMM Global Steel Daily Report](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)

![[China Iron Ore Brief] Iron ore concentrates prices in west Liaoning may consolidate](https://imgqn.smm.cn/usercenter/ocJKj20251217171717.jpg)