Copper Price Trends in H1 2026

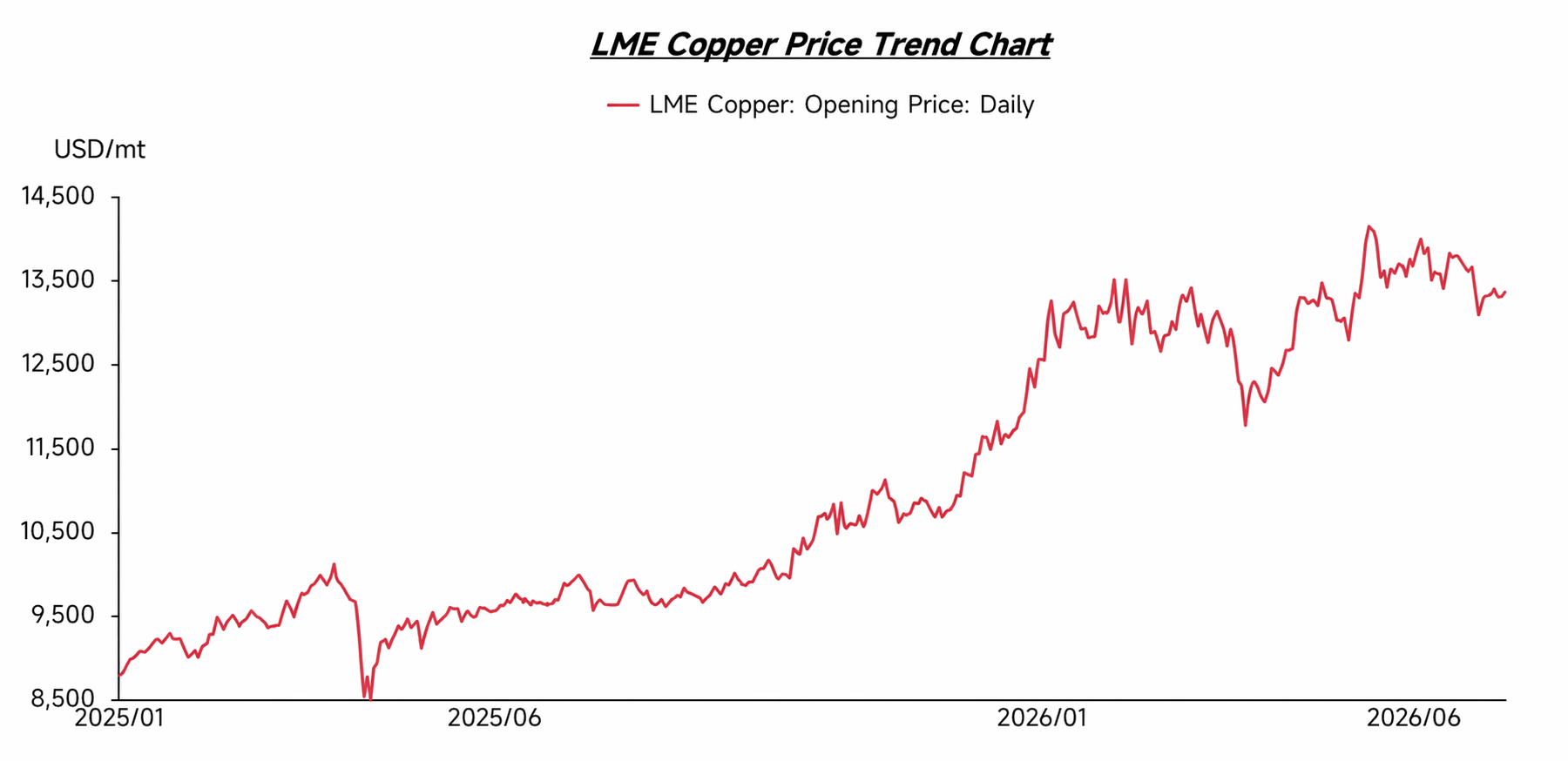

In Q1 2026, copper prices overall stayed high, consolidating around $13,000/mt. It was not until the end of Q1 that copper prices saw a temporary pullback, but they entered Q2 and then started an upward trend again, continuously hitting new historical highs. Behind this, on the one hand, tight copper ore supply provided support; on the other hand, the global copper resource siphon effect triggered by US tariff expectations further amplified market concerns over the supply side. At the same time, rapid growth in new copper-consuming sectors such as NEVs, new energy power, power grid construction, and data centers kept fueling market expectations for copper demand. Against the backdrop of supply growth struggling to match demand growth, copper prices received strong support.

The tight copper supply structure also further pushed enterprises to shift their focus from the ore side to supplementary sources beyond ore, among which copper scrap significantly gained importance. As copper prices kept surging, copper scrap prices also rose in tandem, while structural changes brought about by copper resource scarcity caused the pricing logic of the copper scrap market, previously dominated by consumption and price spreads, to begin shifting.

Supply Side

From the supply side perspective, the overseas copper scrap market was in a generally tight state at the time. Although high copper prices stimulated the willingness to collect and sell copper scrap to some extent, market inventory had been continuously depleted from Q4 2025 to Q1 2026, leaving overseas available cargoes still limited. According to feedback from some overseas scrap yards, the delivery lead time after placing orders had been noticeably extended, with some orders requiring a wait of 3–4 weeks before shipment could be arranged, reflecting that the supply tightness had not been effectively alleviated.

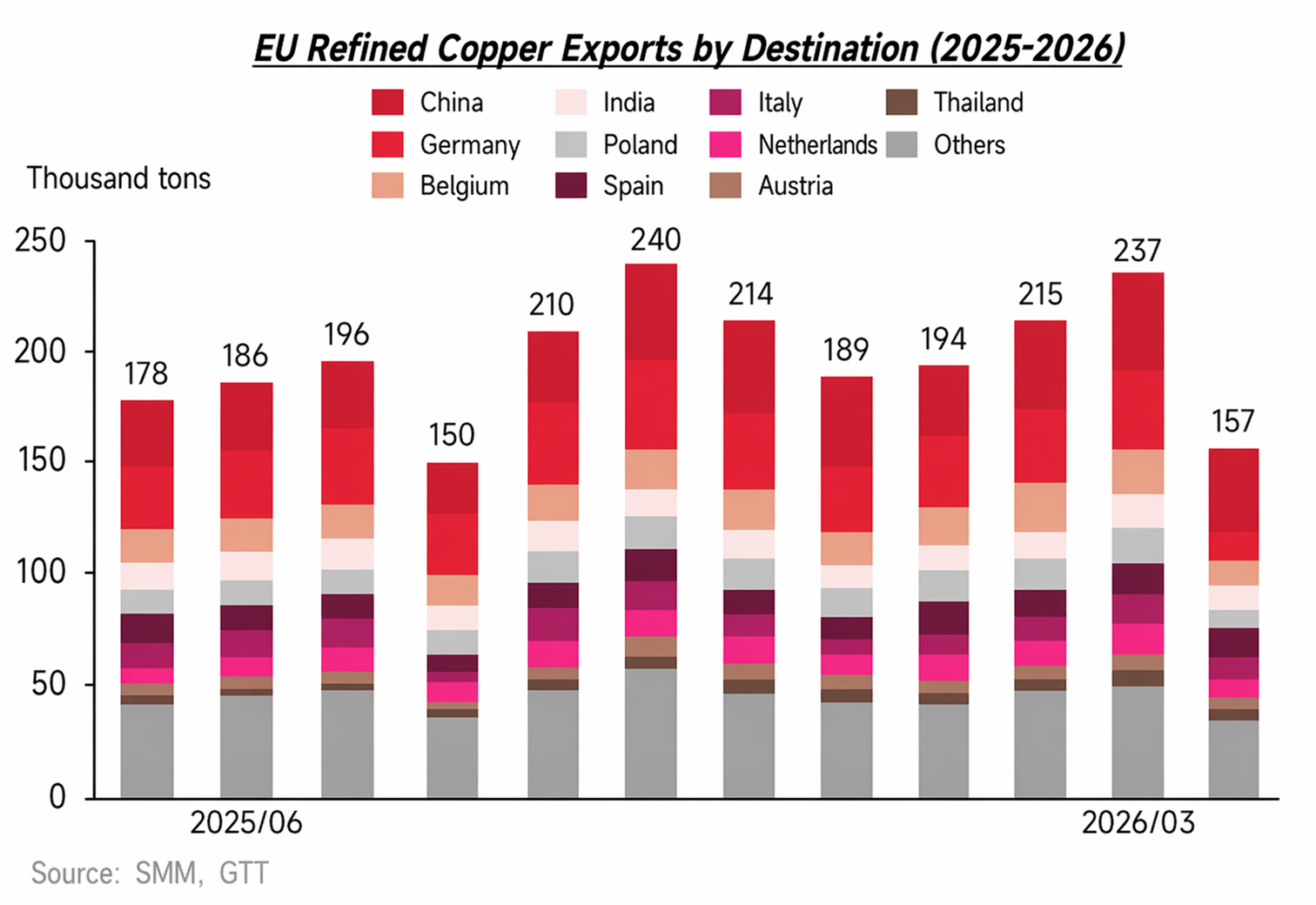

Meanwhile, traditional copper scrap exporting regions such as Europe and the US were actively promoting manufacturing reshoring, and local demand for scrap processing and smelting increased, further weakening the supply elasticity of traditional export markets. Under the combined impact of reduced exportable resources, stronger local absorption capacity, and intensified competition for high-quality scrap, the tight supply situation in overseas copper scrap markets continued.

Demand Side

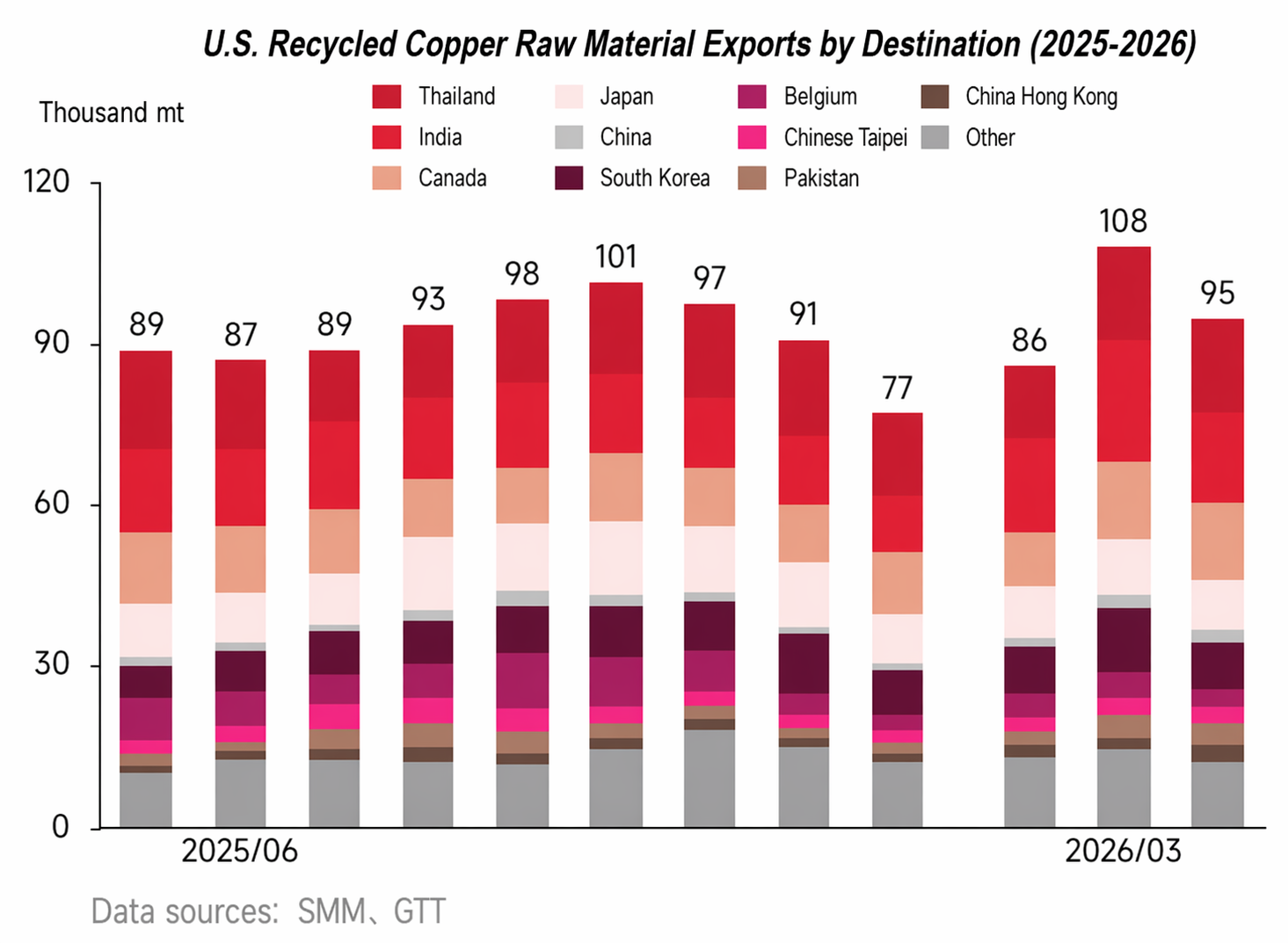

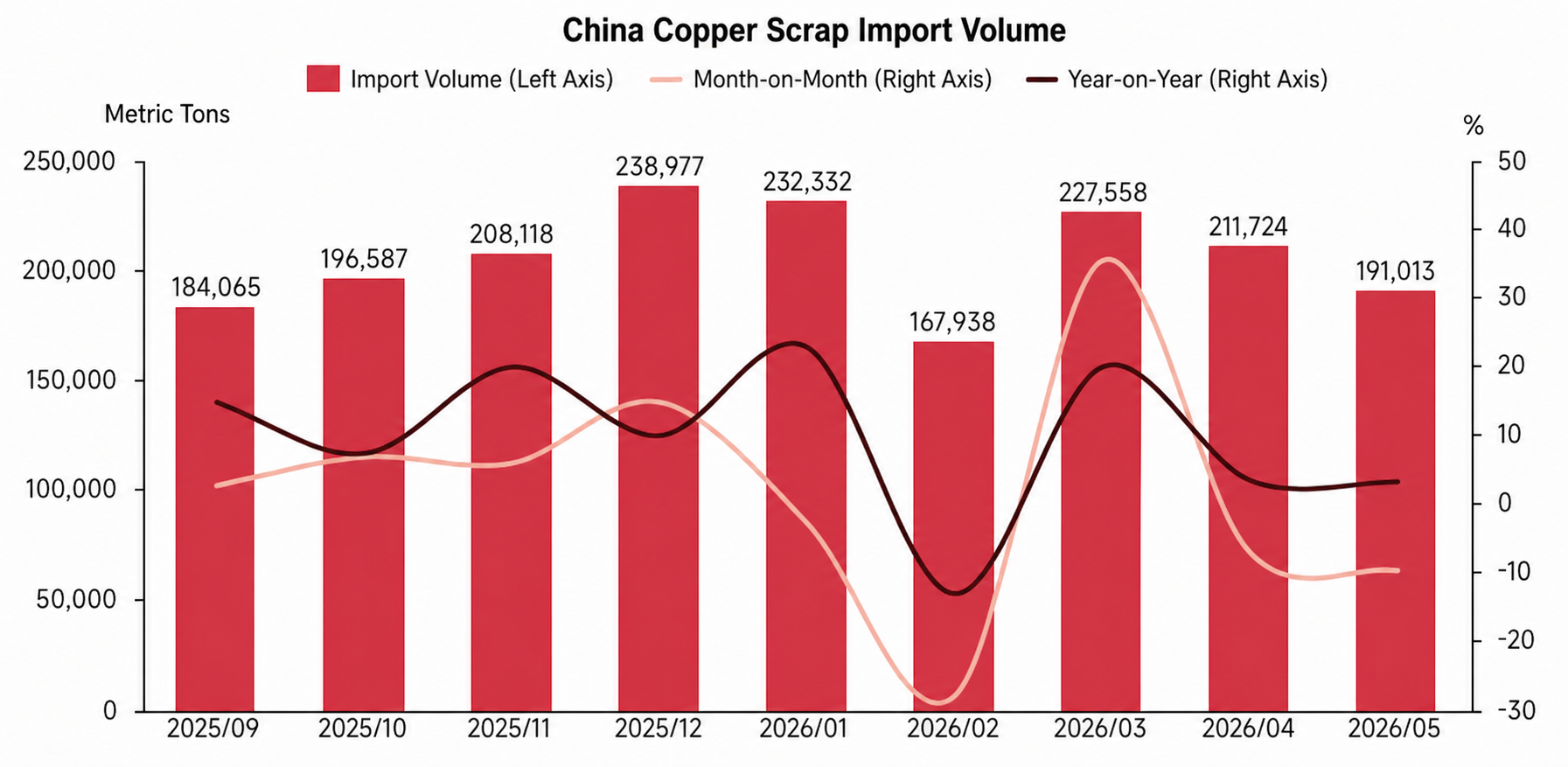

As the world’s largest copper scrap consumer market, China’s imports have long accounted for about one-third of global copper scrap trade. Since the beginning of 2026, impacted by domestic policies and tax compliance requirements, the circulation and use of untaxed copper scrap in the Chinese market have been restricted, which has also pushed domestic enterprises to continuously increase their procurement demand for imported taxed copper scrap. In H1 2026, China’s copper scrap imports overall stayed high. Except for February, which saw a temporary pullback due to the Chinese New Year holiday and high copper prices, imports in other months kept growing compared to the same period in 2025, reflecting that the rigid demand support from the Chinese market for overseas copper scrap remained strong.

Outside China, India, Southeast Asia, and some Middle Eastern regions are also strengthening their absorption capacity for medium- and low-grade copper scrap. After entering these regions, some low-grade scrap is re-processed through dismantling, crushing, sorting, or smelting, and then flows to local consumption or regional markets. From this perspective, the demand for copper scrap outside China is no longer solely determined by Chinese imports. Instead, a competitive landscape involving China, India, Southeast Asia, and local markets in exporting countries is gradually taking shape.

Meanwhile, amid expectations of tighter copper supply in the future, competition for copper scrap resources is intensifying globally. Smelters and related enterprises across the industry chain are actively expanding channels for copper scrap resources, and some countries are also strengthening the retention of their local recycled metal resources. Coupled with the reshoring of manufacturing in the US and Europe, which is driving a rebound in local secondary copper processing and smelting demand, the outflow capacity of copper scrap from traditional exporting regions outside China has been weakened. Driven by Chinese import demand, local demand outside China, and the trend of resource retention, global demand for copper scrap is on an overall upward trajectory.

Copper Scrap Prices

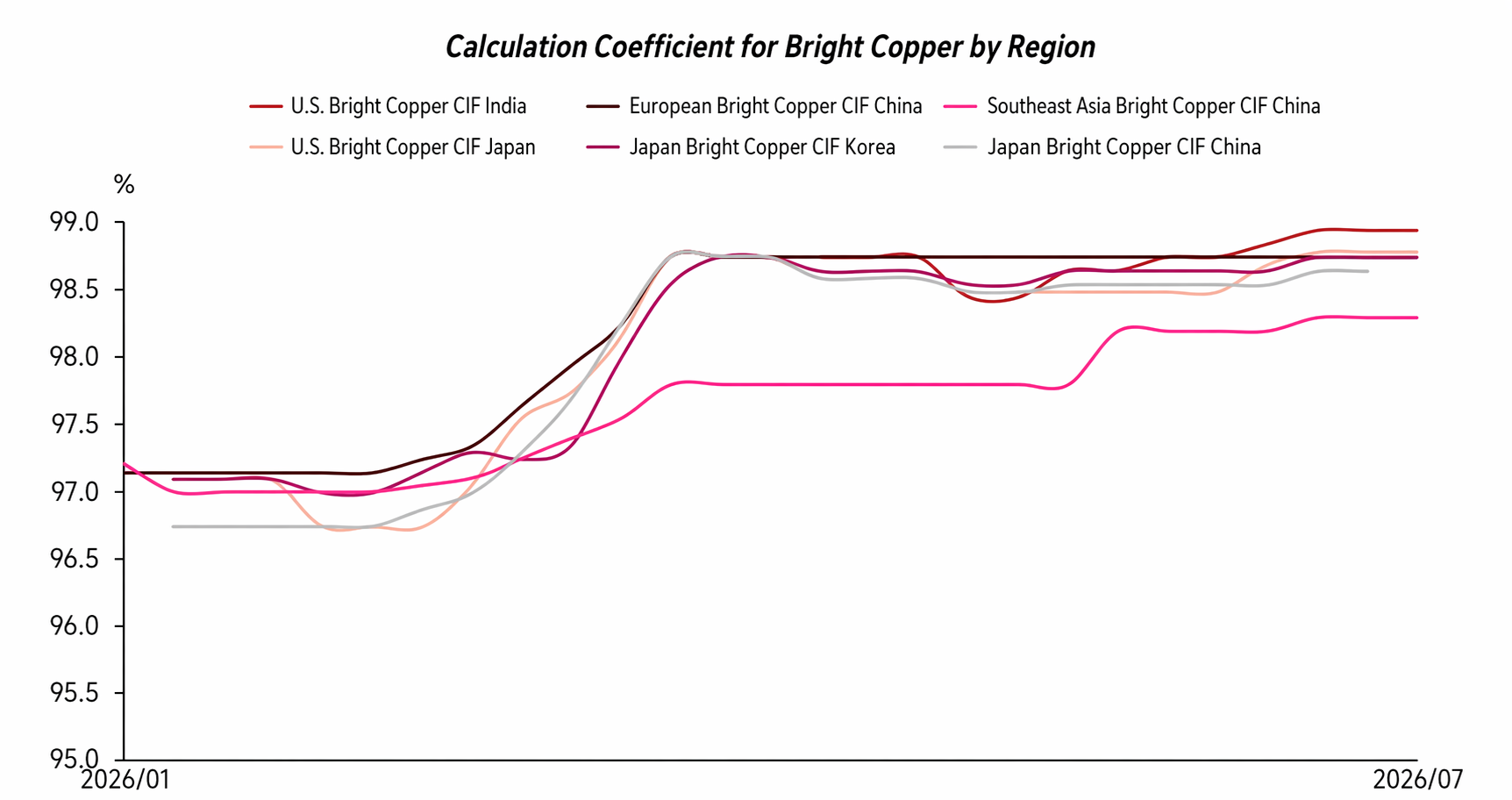

Against a backdrop of tight supply-demand balance and intensified regional competition, the payable indicator for copper scrap outside China shows an overall upward trend. Since the start of 2026, copper prices have continued to consolidate at highs, and the overall quotation for bare bright copper has also been at relatively high levels, with transaction ratios mostly around 97.5%–98%. After copper prices experienced a phased pullback in March, the payable indicator for copper scrap climbed further, and the quotation range for bare bright copper once rose to 98.5%–99%. However, after the pullback ended and copper prices re-entered an upward trajectory in Q2, even repeatedly hitting new record highs, the payable indicator for copper scrap did not see a notable pullback as in past pricing logic, but instead continued to stay high. This shift reflects that, supported by tight raw material supply and rigid procurement demand, the payable indicator for copper scrap outside China remains resilient even when copper prices are high, with limited downside room.

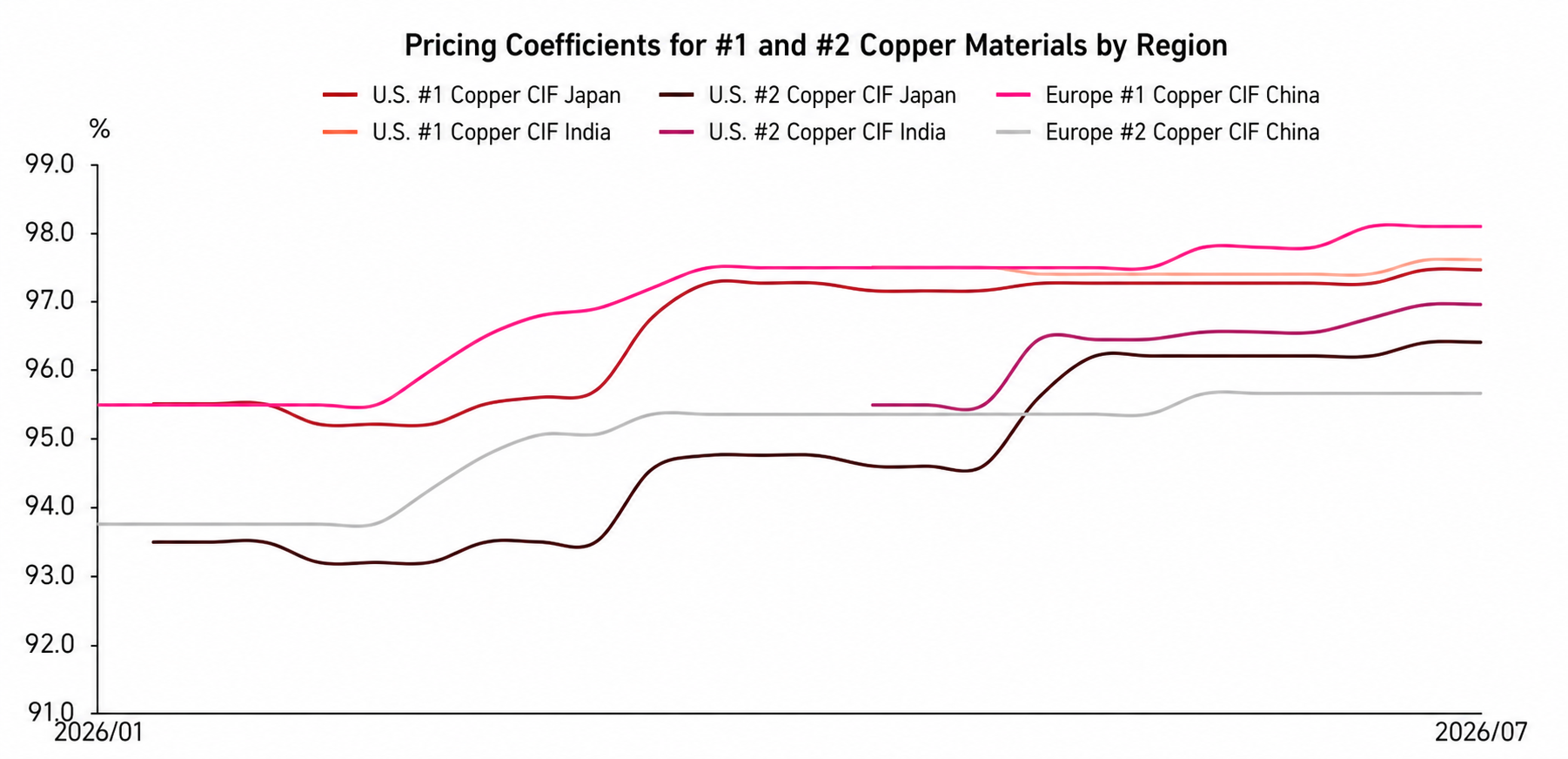

This trend is also evident in the prices of No.1 copper scrap and No.2 copper scrap. Since the start of 2026, the transaction ratio for No.1 copper scrap has kept rising, climbing from around 95.5%–96% at the beginning of the year to the current 97%–98% range. No.2 copper scrap prices have also risen markedly, and market quotations are becoming increasingly divergent. Affected by sustained high precious metal prices, smelters have become significantly more willing to accept higher prices for No.2 copper scrap with high gold and silver content, and quotations for some such cargoes can reach 97.5%–98.5%, even exceeding prices of some No.1 copper scrap.

From the perspective of supply structure, No. 2 copper semis with high gold and silver content mainly come from the Americas, so overall quotes for No. 2 copper semis from the Americas are notably higher than from other regions. In contrast, No. 2 copper semis from Japan, South Korea, and Southeast Asia generally have lower gold and silver content, leaving their price performance relatively under pressure, with transaction discounts mostly concentrated in the 95%–96% range. From this, it can be seen that the pricing logic of the copper scrap market has changed significantly, no longer simply following the past convention that “when copper prices rise, payable indicators pull back.” With tight raw material supply, intensifying resource competition, and widening structural differences among supply sources, copper scrap prices are increasingly influenced by multiple factors such as copper content, precious metal content, source region, smelting demand, and destination purchasing capacity, further highlighting the trend of price divergence.

Policy Side

Policy side, it has always been an important variable affecting copper scrap trade outside China. In recent years, as expectations of tight copper supply-demand have continued to intensify, countries have attached increasing importance to copper scrap as a strategic secondary resource, and major economies have continued to tighten oversight of scrap metal exports, imports, and local recycling.

Take the EU as an example. It is expected to formally implement new waste metal export regulatory requirements starting May 2027. At that time, copper scrap exports to non-OECD countries will need to meet two conditions simultaneously: the destination country must be on the EU's white list, and the destination processing plant must pass an independent third-party audit. This policy aims to raise the threshold for waste metal exports, restrict the outflow of insufficiently processed secondary metal resources, and encourage more copper scrap to remain in Europe for recycling and utilization. In the US, the copper industry has already advanced the proposal to include "copper/secondary copper in the 45X tax credit" to the Congressional legislative level, hoping to enhance the competitiveness of domestic manufacturing and secondary copper processing through tax incentives, thereby further improving the retention of domestic resources.

In addition, as the world's largest consumer market for copper scrap, changes in China's policy landscape also have a significant impact on the global copper scrap trade pattern. Currently, the Chinese market is actively promoting the standardized development of the secondary resources industry. For a long time, some enterprises purchasing domestic copper scrap have faced difficulties in tax accounting and compliance due to the lack of input invoices from upstream collectors. In recent years, China has been promoting the "reverse invoicing" mechanism, under which the buyer issues invoices to sellers that lack invoicing capabilities, in order to improve the input documentation system. However, due to operational difficulties in implementation, some enterprises have further increased their demand for imported copper scrap with tax documentation to meet requirements for tax-inclusive raw material production and compliant operations, providing strong support for copper scrap demand outside China.

In Southeast Asia, countries represented by Malaysia and Thailand have long served as transshipment and preliminary processing hubs for low-grade recycled metal raw materials. However, with heightened environmental awareness and growing demand for industrial upgrading, these countries have tightened inspection and supervision on the import of low-end recycled metal raw materials, with some categories even facing stricter restrictions or bans. Their policy aims to transform domestic industries toward higher value-added segments while reducing environmental pollution and social issues caused by non-compliant processing of low-end recycled metal raw materials. As a result, more low-grade copper scrap will likely need to undergo more thorough sorting, dismantling, and pre-processing before export or shift to new transshipment and processing regions. This will further raise compliance costs and circulation costs in global copper scrap trade.

Overall, future global copper scrap trade will no longer depend solely on price levels but be more influenced by policy compliance, environmental requirements, resource retention, and local processing capacity. For traders, being able to consistently supply high-quality, low-impurity cargoes with complete compliance documentation will be more competitive than relying solely on low prices.

H2 2026 Outlook

Looking ahead to H2 2026, first, available supply is unlikely to ease significantly. With previous inventories continuously depleted and limited release of new scrap outside China, coupled with rising local copper scrap processing demand and resource retention intentions in traditional export regions such as Europe and the US, overseas exportable supply is expected to be hard-pressed to show notable volume growth. Among these, mainstream categories such as bare bright copper, No.1 copper, and No.2 copper semis will remain tight.

Second, multi-regional competition on the demand side will continue to support copper scrap prices. China's import demand remains a key pillar for the overseas copper scrap market, while absorption capacity in India, Southeast Asia, Japan and South Korea, Europe, and the US is also strengthening. Global demand for copper scrap will feature multi-regional competition, and the scramble for resources will also keep copper scrap discounts from seeing a significant downward adjustment.

Against a backdrop of tight supply and intensifying resource competition, overseas copper scrap payable indicators are expected to stay high in H2. Downward support for discounts on bare bright copper and No.1 copper remains strong, while No.2 copper semis prices will continue to be influenced by differences in gold and silver content, origin regions, and smelting demand, sustaining pronounced divergence in quotes.

Moreover, high copper prices will continue to elevate trading risks. As copper prices fluctuate at highs, per-shipment cargo values will rise correspondingly, increasing traders' capital tie-ups, exposure to exchange rate fluctuations, and costs in logistics, warehousing, inspection, and compliance. Therefore, even if there is rigid demand support in the market, actual transactions may become more cautious, and buyers and sellers will pay increased attention to price lock-in, quality stability, and shipping cycles.

Overall, the copper scrap market outside China in H2 2026 is expected to maintain a tone of "tight supply, high discount rates, price divergence, and rising trade costs."

![Typhoon Disrupts Arrivals, China's Copper Social Inventory Sees Sharp Drawdown [SMM Weekly Data]](https://imgqn.smm.cn/usercenter/jlrsy20251217171711.jpg)

![With contract rollover imminent, end-users hold off purchases; suppliers hold prices firm and spot trades remain sluggish [SMM North China Copper Spot]](https://imgqn.smm.cn/usercenter/qcyEh20251217171709.jpg)

![Copper prices fell, but end-use demand was weak, and suppliers proactively cut prices to sell[SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/xKfXl20251217171711.jpg)