SMM, July 7:

In the first half of 2026, geopolitical conflicts in the Middle East emerged as one of the decisive factors affecting electrolytic aluminum prices. Prior to the Middle East events, expectations of a US dollar rate-cut cycle were bullish for non-ferrous metal prices, and overseas electrolytic aluminum prices generally maintained a firm trend in January. However, high aluminum prices suppressed demand, compounded by the impact of the domestic Spring Festival holiday, leading to larger-than-expected domestic aluminum ingot inventory accumulation. In February, domestic and overseas aluminum prices fell in tandem. On February 28, the US-Israel coalition launched a military strike against Iran, officially marking the beginning of the Middle East geopolitical conflict's impact on aluminum prices.

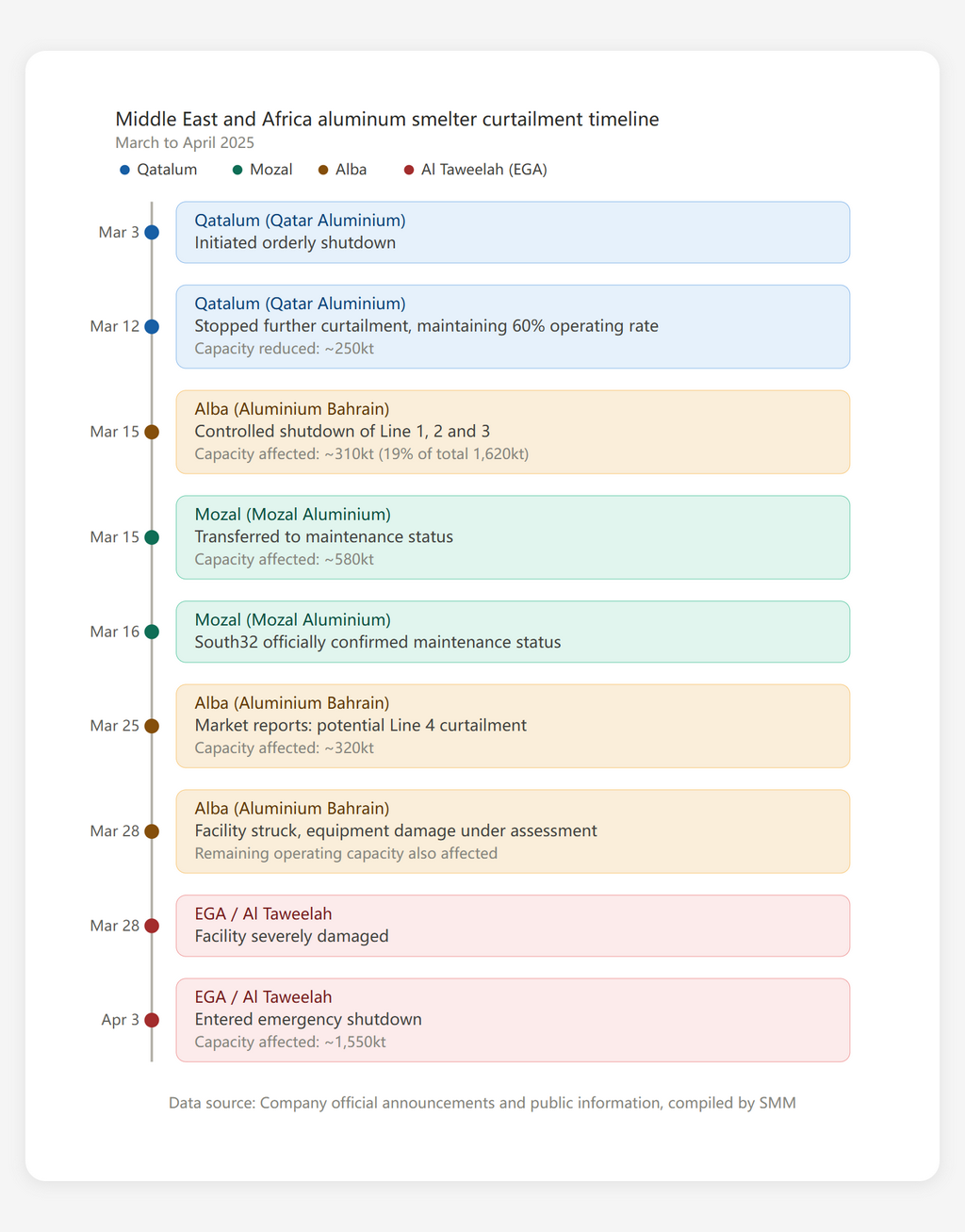

Middle East Geopolitical Conflict Triggers Production Cuts; Supply Gap Expectations Drive Up LME Aluminum Prices

Affected by the US-Iran conflict, some aluminum smelters in the Middle East experienced production cuts. Combined with the Mozambique aluminum smelter entering shutdown in March, the market expected overseas electrolytic aluminum fundamentals to face a significant supply gap. Boosted by this, overseas aluminum prices continued to climb, with the LME 3M aluminum price reaching a near three-year high of $3,787.5/tonne on June 2. The timeline of production cuts at Middle East and Mozambique aluminum smelters is as follows.

In addition, power and other infrastructure in Iran was damaged, making it difficult for local aluminum smelters to sustain production. However, with no official announcements yet, SMM has made its own production cut assessment. As of mid-April, SMM estimated that the total capacity affected by production cuts in the Middle East and Mozambique could reach approximately 3.5–4.0 million tonnes.

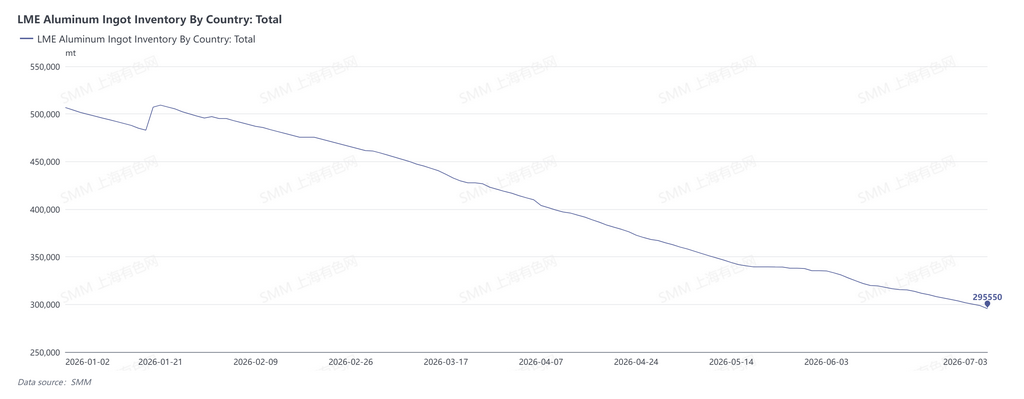

Under the impact of significant production cuts, overseas electrolytic aluminum fundamentals shifted to a deficit, with total LME aluminum ingot inventory and Japanese port aluminum ingot inventory continuing to decline. As of end-June 2026, LME global aluminum ingot inventory stood at 302,000 tonnes, down 207,000 tonnes from end-2025. As of end-May, Japanese major port electrolytic aluminum inventory was 239,000 tonnes, down 78,000 tonnes from end-2025.

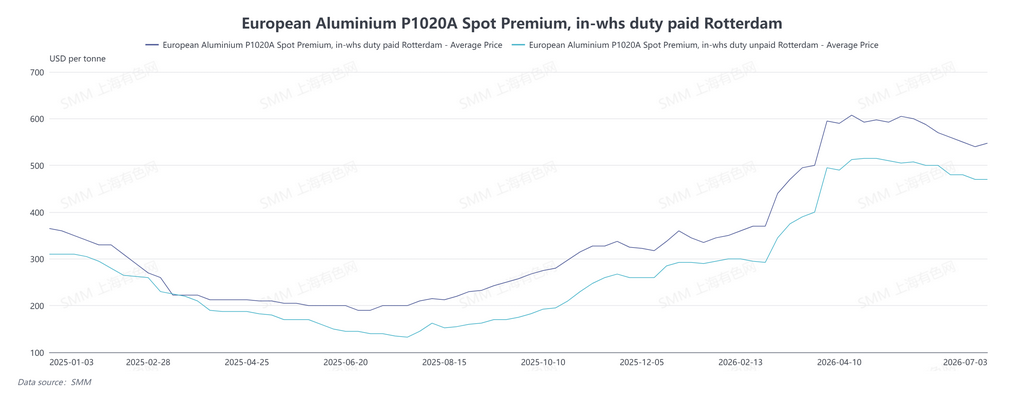

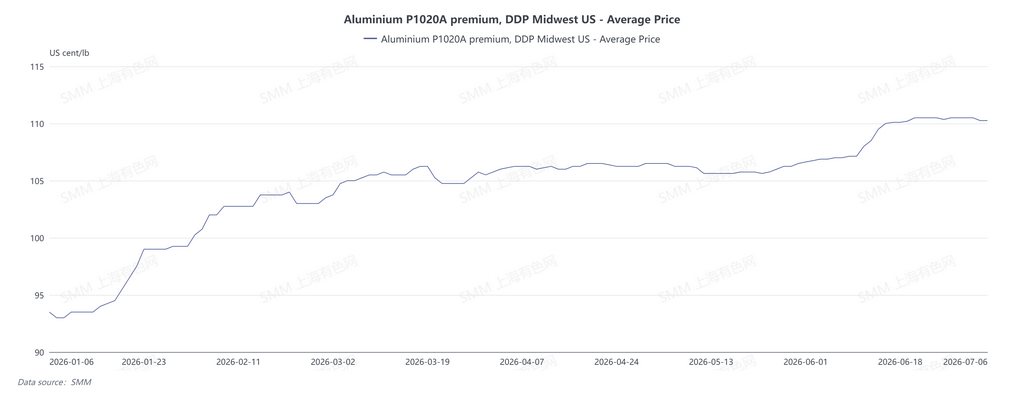

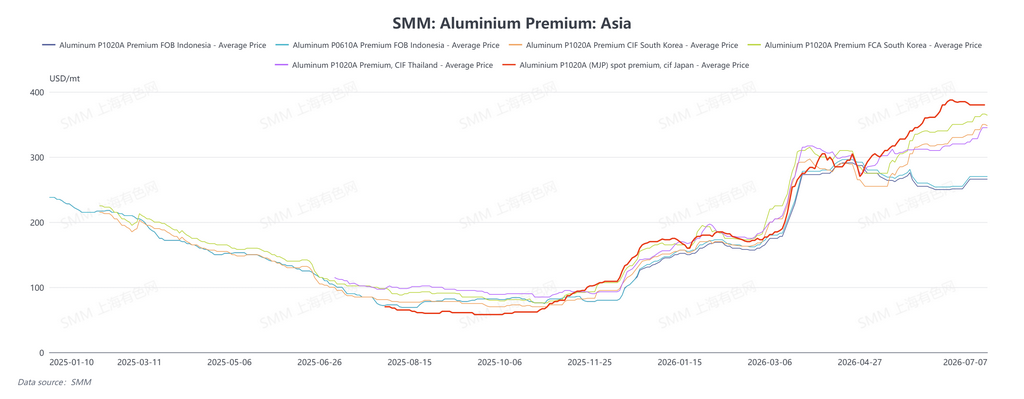

Amid expectations of supply tightening, ex-China aluminum premiums strengthened. As of end-June, SMM Japan MJP aluminum ingot spot premium recorded $380/mt, up 123.5% from the end of last year, and SMM Japan Q3 MJP aluminum ingot premium recorded $395/mt, up $309/mt from Q4 2025, a jump of 359.3%. SMM Europe P1020A aluminum ingot duty-paid price recorded $547.5/mt, up 62.2% from the end of last year, while SMM Europe P1020A aluminum ingot duty-unpaid price recorded $470/mt, up 64.9% YoY. SMM US Midwest DDP aluminum premium recorded 110.5¢/lb, equivalent to around $2,435/mt, up 18.2% from the start of the year, an absolute increase of approximately $374.7/mt.

Although supply tightened and aluminum ingot destocking took place, downstream purchasing enthusiasm was subdued by high prices, with actual transactions in Asia persistently at a discount to the Japan MJP aluminum ingot premium. Indonesia saw a concentration of new project startups; as new projects continued to ramp up production, supply increased, and since Q2, Indonesia aluminum ingot FOB prices showed a trend of pulling back slightly. As of end-June, SMM FOB Indonesia P0610A average price recorded $270/mt, up 92.9% from the end of last year, but down 8.8% from this year's high of $296/mt. SMM FOB Indonesia P1020A average price recorded $266/mt, up 97.0% YoY, but down 8.6% from this year's high of $291/mt.

Aluminum premiums in other regions maintained an overall uptrend. As of end-June, SMM CIF South Korea P1020A average price recorded $342/mt, up 132.7% from the end of last year; SMM FCA South Korea P1020A average price recorded $362/mt, up 119.4% YoY; and SMM CIF Thailand P1020A average price recorded $328/mt, up 120.9% YoY.

High Profits Accelerate Electrolytic Aluminum Restarts and New Project Commissioning

Under high aluminum prices, electrolytic aluminum companies enjoyed substantial profits. These high profits stimulated some idled capacity to accelerate restarts and also catalyzed more new electrolytic aluminum projects, accelerating their commissioning.

In the first half of the year, three electrolytic aluminum smelters resumed idled capacity to varying degrees, and two additional smelters announced plans to restart production in 2026. Details are as follows:

-

San Ciprián smelter in Spain safely completed restart on April 8, with total capacity of approximately 230,000 tonnes/year, representing an increase of approximately 150,000–200,000 tonnes/year compared to 2025 operating capacity.

-

Mount Holly in the United States began restart in April, with plans to reach full capacity by end-June, involving 50,000 tonnes/year of capacity.

-

Grundartangi smelter in Iceland began restart in April, expected to complete restart by end-July, involving 210,000 tonnes/year of capacity.

-

Magnitude 7 Metals planned to restart potline No. 1 cells at its New Madrid aluminum smelter in the United States, with plans to add 75,000 tonnes/year of primary aluminum capacity by end-2026.

-

Norsk Hydro indicated that the Slovalco smelter in Slovakia planned to restart partial primary aluminum production in Q4 2026, involving 75,000 tonnes/year of capacity.

Regarding new projects, according to SMM estimates, total planned commissioning capacity for overseas electrolytic aluminum in 2026 is approximately 2.3 million tonnes, of which approximately 700,000 tonnes have been commissioned, with the remaining 1.6 million tonnes expected to be commissioned in the second half of 2026. For details, please follow the "SMM Overseas Electrolytic Aluminum Project Monthly Review" series.

Overall, although the Middle East and Mozambique experienced large-scale production cuts in the first half of the year, the acceleration of restarts and new project commissioning partially offset the supply reduction. According to SMM estimates, total overseas electrolytic aluminum production in H1 2026 was 14.397 million tonnes, down 4.1% year-on-year, and total overseas demand was 13.612 million tonnes, down 3.1% year-on-year. Since overseas electrolytic aluminum had a net inflow of approximately 1.234 million tonnes into the domestic market in H1, the overseas electrolytic aluminum deficit in H1 is estimated at approximately 450,000 tonnes.

H2 Outlook: Middle East Restarts Combined with New Project Ramp-up Increase Supply, Putting Pressure on Aluminum Prices

In June–July, the Middle East geopolitical situation showed no clear signals of further deterioration, and news of restarts emerged from Middle East aluminum smelters that had undergone production cuts. On July 2, EGA announced that its Al Taweelah plant had made progress in restart efforts: anode removal work for all electrolytic cells had been completed; cell cleaning was approximately 90% complete; and over 20% of solidified aluminum blocks inside cells had been cleared. On May 26, the first electrolytic cell was successfully restarted; as of July 2, 89 cells were in operation (out of a total of 1,262 cells), equivalent to approximately 110,000 tonnes of capacity. In addition, Aluminum Bahrain and Qatalum were also expected to gradually begin restarts.

With Middle East restarts combined with continued ramp-up of new projects, the global electrolytic aluminum balance is expected to shift toward a surplus by Q4 2026.

![July Ex-China Alumina Supply Rebounds Significantly, Middle East Restart and Indonesian Policy Changes Draw Attention [SMM Analysis]](https://imgqn.smm.cn/usercenter/YPMhF20251217171654.jpg)